Record review

Share this article

Jane Mellor considers the updated 2017 CPD requirements for CIOT and ATT members, and reports on the review of 2018 records

Key Points

What is the issue?

From 1 January 2017, the CPD requirements for CIOT and ATT members and ADIT affiliates changed. The first review of records under the new regulations has just been completed, so it is an ideal opportunity to feed back to members on themes identified during the review.

What does it mean for me?

The CIOT and ATT will be continuing the annual programme of reviewing records. All members coming within the scope of the regulations should be prepared to provide their records on a timely basis if requested.

What can I take away?

This article reminds members of the requirements under the regulations and also sets out tips on how to ensure appropriate CPD is undertaken and recorded.

Updated continuing professional development (CPD) regulations and guidance notes (bit.ly/2P220Iv) came into force on 1 January 2017. As a reminder, the regulations apply to members who:

- 1.2.1: provide tax compliance services, advice, consultancy or guidance in tax including, without limitation, those in private practice, the public sector, commerce, industry or not for profit sector;

- 1.2.2: do not fall in para 1 above but who use the designation CTA, CTA (Fellow), ATII, FTII, Chartered Tax Adviser, ATT, Taxation Technician, ATT (Fellow), Taxation Technician (Fellow), ADIT affiliate or International Tax Affiliate of the Chartered Institute of Taxation.

There was therefore a major change in terms of the members who came within the scope of the CPD regulations, as those not working in a tax related role but holding themselves out to the public as a CTA, ATT or ADIT affiliate have been required to consider the extent, if any, of their CPD need.

The CPD requirement for those coming within the scope of the regulations is: ‘Members are required to perform such CPD as is appropriate to their duties.’ CPD requirements must be met over the calendar year and the first records reviewed since the change have been those for the year to 31 December 2018.

A previous article (‘A new approach’, Tax Adviser, December 2016) set out the changes and the reasons why the CIOT and ATT decided to move away from the previous hours based approach.

What is the CIOT/ATT process for reviewing CPD records?

In early summer 2019, the CIOT and ATT wrote to a selection of members requesting their CPD records and they were initially given six weeks to email those records to us.

Once records had been received, a review was then undertaken by the Professional Standards team. Where appropriate, anonymised records were also considered by the team of tax professionals who volunteer to take part in the CPD working party.

Where the records were satisfactory, an acknowledgement email was sent confirming that nothing further was required from the member. In some cases, follow up emails or telephone calls were undertaken to obtain further information from the member or to provide guidance on how records could be improved going forward.

Note that members are required to reply to correspondence from the CIOT and ATT. Therefore, even where members consider that they do not come within the requirements of the regulations, they must respond and advise us why they do not think they are within the scope of the requirements. Members not replying to correspondence are referred to the Taxation Disciplinary Board (TDB) for disciplinary action, and this is a referral which is distinct from any referral for not meeting the CPD requirements.

What were the findings?

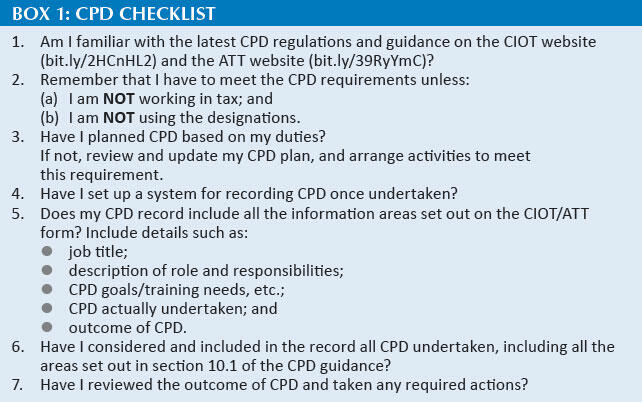

The working party were pleased to see that in general members had a good understanding of CPD requirements and good records in support of what they had done to meet those requirements. Good practice points and certain themes arising from the review are set out below and a checklist is supplied at the end of the article for members to use when considering their own CPD.

Familiarity with the requirements

As you would expect, members working in tax were familiar with the requirement to undertake CPD. Many of the records provided made it clear that members had kept up to date with the latest regulations and guidance and were aware of the 2017 changes. Members had set out what their role was, the particular areas they needed to focus on, and the CPD planned and undertaken to meet this requirement. Whilst it is acceptable to record hours of CPD undertaken based on the previous regulations, it is important that records make it clear how the CPD that is planned and undertaken is appropriate to the member’s duties.

Members working in areas other than tax should consider carefully whether

The CIOT/ATT CPD record form is not mandatory but it provides a guide as to the information which the CIOT and ATT would find helpful to see during a review.

they are now within the scope of the regulations because they use the designations (with the exception of honorary members). Not all members appeared to be fully aware of the change in the regulations. Members could confirm that CPD had been undertaken but their records were not always maintained in a structured way, which meant it was harder for the member to demonstrate they had planned their CPD and complied with the regulations.

Those members not working in tax and not holding themselves out as members through use of the designations should be able to clearly articulate their reason for not undertaking and recording CPD if their records are requested. When completing their annual membership return, they will be asked the question: ‘Have you completed your continuing professional development in accordance with CIOT/ATT regulations?’ Members who do not work in tax and do not use their designations should answer ‘yes’ when asked if they meet the requirements of the regulations.

Recording

Having planned and undertaken CPD, it is important that it is recorded. Members should be aware that:

- The CIOT/ATT CPD record form is not mandatory but where used it provides a guide as to the information which the CIOT and ATT would find helpful to see during a review. It provides a structured approach which helps to identify whether requirements have been met.

- Where members retain records in other formats (excel, timesheet records, etc.), these are acceptable for submission; however, it is good practice to ensure that records include broadly the same information as would be provided on the CIOT/ATT record form. When sending these records, members need to supply details of their job title and a brief description of their role to assist with the review.

- Good records seen during the review included the whole range of different types of CPD undertaken. Some members understated what they had done by only providing a list of the structured courses or webinars attended. The wide range of activities which counts as CPD is set out in the CPD guidance but some members omitted to include details such as reading technical journals, coaching and mentoring within their firm, technical research and attendance at branch events.

- Records do need to be submitted and it is never sufficient for members to respond to a request by stating that they meet the requirements of Ideally, the record will include a consideration of the outcome of CPD undertaken so the plan and CPD activities can be updated if required.

Voluntary work

Members selected for review included those who are undertaking voluntary and pro bono work, often using their tax skills. It was helpful to receive records showing that members had undertaken CPD of relevance to these roles, as well as in relation to paid roles.

What next?

Members should continue to look out for further guidance in relation to CPD on the CIOT and ATT websites, including a brief film setting out points in relation to compliance with CPD requirements.

The CIOT and ATT will be contacting members in Spring 2020 to request records for the year to 31 December 2019. Members selected should ensure that they promptly provide complete records for the year. In the meantime, members may want to review their own CPD requirements and the records being maintained using the checklist in Box 1.