The rules on travel and subsistence: a long and winding road

Share this article

As our working patterns shift and more of us move to hybrid working, what impact will this have on claiming tax relief for travel and subsistence expenses?

Key Points

What is the issue?

While travel and subsistence is an area of compliance that seems straightforward on the face of it, it can actually be extremely complex for employers to understand and get right.

What does it mean for me?

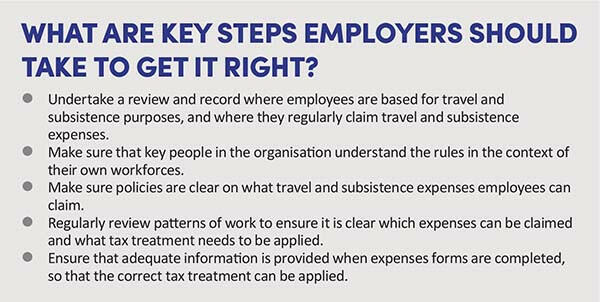

Key considerations include rules concerning permanent and temporary workplaces, ordinary commuting and working from home. Make sure your policies are clear on what travel and subsistence expenses employees can claim.

What can I take away?

With the move to widespread hybrid working, we expect to see HMRC increasing its focus on these types of travel and subsistence expenses.

The coronavirus pandemic has significantly changed the way we work. Homeworking has become the norm for many more employees who previously spent all or almost all of their time in offices. Millions of us are now working from home for two or three days each week and spending the rest of the working week in the office. Homeworking and hybrid working appear to be here to stay.

That all sounds familiar and straightforward but the nub of the problem is that, for travel and subsistence expenses, even though more employees work remotely and/or are much more mobile than they used to be, the current tax rules covering employee travel and subsistence have not changed substantively since April 1998.

It was widely hoped back in 2016, when the last review of the travel and subsistence rules took place, that some of the shortcomings in the rules might be addressed. But the fact they were not should come as no real surprise, as the 1998 amendment itself aimed to change rules that had dated back some 140 years.

While travel and subsistence is an area of compliance that seems straightforward on the face of it, it can actually be extremely complex for employers to understand and get right. It is no coincidence that HMRC has issued a guidance booklet with over 70 pages to help explain the rules, and that it focuses on travel and subsistence during its reviews of employer records.

In the past, HMRC has undertaken detailed reviews of situations where employees have a workplace at home but also another elsewhere (such as their employer’s headquarters) and the employer meets the cost of journeys between their home and the other workplace; or where the employer is paying travel and subsistence expenses for what they believe is a move covered under the ‘detached duty’ rules allowing for the amounts to be paid tax free. With the move to widespread hybrid working, we expect to see HMRC increasing its focus on these types of travel and subsistence expenses.

Within the current system, there are two main things to bear in mind relating to travel and subsistence.

The first (under the Income Tax (Earnings and Pensions) Act (ITEPA) 2003 s 337) is that tax relief is provided for ‘travel in the performance of the duties of the employment’. In other words, relief is given for travel that is an intrinsic part of an employee’s job and may include journeys between two workplaces. This rule is generally well understood by employers and often applied correctly in practice, but this could change going forward as more employees work from home and employers incorrectly conclude that their employees’ homes are workplaces for tax purposes.

However, it is in relation to the second rule (under ITEPA 2003 s 338) – which provides tax relief for necessary journeys to workplaces that employees must attend for work purposes, apart from those amounting to ‘ordinary commuting’ – that problems most often arise.

Key terms and considerations

The key terms and considerations needed to understand the rules are summarised below. Note that the rules for subsistence are similar to those for travel. If a business journey is allowable for tax purposes, the subsistence cost attributable to that journey generally is also allowable, unless there are issues around excessive expenditure, dual-purpose trips, and round sum or benchmark allowances.

Travel and subsistence expenses which attract tax relief and satisfy the exemption for paid or reimbursed expenses (ITEPA 2003 s 289A) do not need to be reported to HMRC.

Any travel expenses paid by the employer which do not attract tax relief, and which are not exempted by ITEPA 2003 s 289A, will (depending on the circumstances and subject to a PAYE Settlement Agreement being in place to cover such costs) either need to be:

- reported and dealt with at the tax year-end on forms P11D and P11D(b);

- reported and subjected to tax and Class 1 National Insurance Contributions (NIC) under PAYE at the time of payment; or

- reported and dealt with at the tax year-end on forms P11D for tax purposes and subjected to Class 1 NIC under PAYE at the time of payment.

HMRC penalties for non-compliance can be costly. For example, if incorrect P11Ds are filed negligently, a penalty of up to £3,000 per form can be levied by HMRC (although normally only in the most serious cases).

It could also mean that employers are liable for any tax and NIC that has been underpaid, potentially on a grossed-up basis, plus late payment interest. This can get expensive and large settlements have been seen on HMRC compliance reviews covering travel and subsistence expenses, particularly for large businesses. Settlements are often in relation to homeworkers having another permanent workplace and being paid for their travel expenses between their homes and those permanent workplaces; and travel from home to places which are not considered to be a temporary workplace.

1. Permanent workplace

A ‘permanent workplace’ is considered to be somewhere that an employee works regularly to perform their duties of employment. In many instances, it can be clear whether or not somewhere is an employee’s permanent workplace and, therefore, whether a journey to it can be deemed ordinary commuting. It is also possible for an employee to have more than one permanent workplace at the same time.

Travel to or from a permanent workplace and an employee’s home is generally treated as private rather than business travel, and so tax relief is not due on any related costs that are paid or reimbursed by an individual’s employer.

Necessary travel which takes place between one permanent workplace and another while an employee performs their duties of employment during the working day is treated as business travel and attracts tax relief.

2. Temporary workplace

A ‘temporary workplace’ is somewhere the employee attends to perform a task of limited duration or for a temporary purpose. So even if they attend it regularly, it may still not be classed as a permanent workplace.

There is, however, a special rule which treats a workplace that would otherwise be a temporary workplace as a permanent workplace, where an employee spends or is likely to spend more than 40% of their working time at that workplace over a period that lasts or is likely to last more than 24 months (known as the ‘24 month/40% rule’).

Bear in mind that the 24 month/40% rule treats locations that would otherwise be ‘temporary workplaces’ as ‘permanent workplaces’. If the workplace is not temporary in the first place (as it does not meet the definition laid out in the Employment Income Manual at EIM32075), the workplace would already be treated as a permanent workplace.

Travel to or from a temporary workplace and an employee’s home is generally treated as business rather than private travel; and so tax relief is due on any related costs that are paid or reimbursed by an individual’s employer, unless it is substantially the same journey in which case no deduction is allowable (ITEPA 2003 s 338(2)). This is not often considered by employers and very few expenses policies ever have this covered.

Such distinctions can be confusing – and as highlighted above, this is one of the areas of travel and subsistence on which HMRC focuses its attention. Employers often fail to consider the task involved or the purpose for working at a given location, which is what the legislation requires.

The employee’s attendance is not in question; the issue is whether the task itself will be undertaken for a limited duration or whether it is performed for a temporary purpose. The trouble is that many employers fail to look too deeply at the matter and simply consider the ‘24 month/40%’ rule, without first considering whether the workplace is capable of being a temporary workplace.

HMRC may ask for contracts, diaries and job descriptions in order to determine whether the locations visited meet the definition of a ‘temporary workplace’. Covid-19 has also presented a particular issue in that HMRC’s view is that the clock remained ticking even when government gave instructions to work from home where possible, so many employers are likely to find the 24 month period has expired during the last few years while employees have been working from their homes.

It should also be remembered that the word ‘task’ is not defined in the legislation. As a result, the normal dictionary definition applies. Here a ‘task’ is something specific; for example, a piece of work, rather than a group of things to do, which is the nature of a job more generally.

3. Ordinary commuting

For most employees, ‘ordinary commuting’ is the journey they make most days between their home and permanent workplace. Travel and subsistence expenses would normally be taxable here if the costs of ordinary commuting were paid for or reimbursed by their employer, or if travel facilities were provided.

But for some staff, the situation is more complicated. For example, if the journey to a temporary location is broadly the same as an employee’s ordinary commute to their permanent workplace, tax relief would be denied on the basis that the journey is normally treated as private travel.

This rule applies generally if the journey is in the same direction or on the same route, and amounts to less than 10 miles extra each way than the normal commute. This area is rarely explained in most employers’ travel and expenses policies but is again something that HMRC is increasingly focusing its energy on, particularly in major towns and cities.

4. Working from home

A key consideration when moving to a homeworking arrangement is whether the employer will meet the cost of the employee’s travel between their home and the office when they do travel into the office. This is of particular relevance to hybrid working arrangements.

The tax and NIC treatment of employees’ travel expenses can be complex and is particularly difficult to apply practically to modern working practices, such as hybrid working.

HMRC recently updated its guidance covering employees who work from home (EIM01471) to cover hybrid working. It now includes ‘Travel in the performance of the duties: travel to and from home where it is a place of work’ at EIM32370. The clear challenge with hybrid working is that when employees do travel into the office, often the statutory conditions in ITEPA 2003 s 337 will not be met for home to be a workplace for tax purposes, and under ITEPA 2003 s 338 the office will remain a permanent workplace.

Employers must therefore be clear when agreeing hybrid or homeworking arrangements which travel and subsistence expenses can be paid tax and NIC free and which cannot. EIM32174 covers ‘Travel for necessary attendance: employees who work at home: a hybrid working: example’.

In rare cases, ITEPA 2003 s 337 may apply, allowing for tax relief between the home (as a workplace) and another permanent workplace, as covered in EIM32370. The problem with applying ITEPA 2003 s 337 to hybrid working is that in many cases the location of the home isn’t dictated by the requirements of the job. HMRC notes: ‘For most people, the place where they live is a matter of personal choice. So the expense of travelling from home to any other place is a consequence of that personal choice, not an objective requirement of their job.’ The relief in ITEPA 2003 s 337 is therefore unlikely to apply to the majority of homeworking and hybrid working arrangements. It is worth noting that HMRC’s guidance says:

‘Most employers provide all the facilities necessary for work to be carried out at their business premises. So where employees work at home, they usually do so because it is convenient rather than because the nature of the job actually requires them to carry out the duties of their employment there. However, where it is an objective requirement of an employee’s duties to carry out substantive duties at the home address, then his or her home is a workplace for tax purposes.’

ITEPA 2003 s 338 then needs to be considered. This allows tax relief for travel expenses for the necessary attendance at any place in the performance of the duties of employment. To determine whether tax relief is due under s 338 for journeys between an employee’s home and their employer’s business premises, we need to consider whether the employee is travelling to a permanent or temporary workplace (see definitions above).

HMRC often quotes the case of Kirkwood v Evans [2002] EWHC 30 when looking at a ‘working from home’ situation. It concluded that although Mr Evans went to the Leeds office for only one day a week, it was a permanent and continuing part of his duties to do so. The judgment dealt with the situation briefly in a single paragraph, also stating that Mr Evans had conceded that the Leeds office was not his temporary workplace, even though the General Commissioners had concluded it was. The judge justified this view by saying: ‘This attendance was both regular and was not for the purpose of performing a task of limited duration or for some other temporary purpose.’

Perhaps Mr Evans was ill-advised to admit that Leeds was a permanent workplace. It could be argued that he undertook certain specific tasks each time he went there that were of limited duration; namely, delivering work he had performed since his last visit, taking new work with him, and downloading information from a database. On the other hand, HMRC seemed to argue that the word ‘task’ refers to doing these things each week on a continual basis.

There are, of course, also other special rules to consider on top of the above that cover areas relating to international trips, area-based and depot-based employees together with emergency call-outs.