The savings conundrum

Share this article

Kelly Sizer explores some of the difficult choices faced by low-income savers

Key Points

What is the issue?

Tax and related state benefits consequences of choosing between savings schemes can be extremely complex.

What does it mean to me?

Tax advisers should not stray into regulated advice (unless they are so authorised), but if asked to comment on savings options from a tax incentive perspective, it is important to compare all available options.

What can I take away?

A new Help to Save scheme for claimants of working tax credit or universal credit is to be introduced by April 2018. But saving into a pension might produce a better overall return if employer contributions and tax relief are added, as well as the saver possibly being able to claim extra universal credit.

Two new government-incentivised savings schemes were promised in this year’s Budget – lifetime individual savings accounts (lifetime ISAs) and one dubbed ‘Help to Save’. Lifetime ISAs will be available from April 2017, Help to Save ‘no later than April 2018’.

In a tax context, you might be asked about the pros and cons of pension savings as against lifetime ISAs. Help to Save could also be considered for lower-income clients claiming either universal credit or working tax credit.

But how will a saver of limited means, unable to afford professional fees, understand the tax and related benefits consequences of the various options? These are the types of complex interactions with which the Low Incomes Tax Reform Group wrestles daily.

Incentivised savings options

Personal debt and lack of disposable income may prevent many low-income people saving. But, with automatic enrolment into workplace pensions, the issue is now inescapable for many unless they opt out of this savings plan.

Help to Save

Information on this scheme is sketchy, and awaits detailed consultation. But the government says Help to Save will allow qualifying individuals to deposit up to £50 a month for two years, with an option to extend for two more. The government will add a 50% bonus to the amount saved at the end of each two-year period, giving maximum savings of £2,400 with a £1,200 bonus.

Let us assume that both the government bonus and interest on the accounts will be exempted from income tax. Otherwise, for this group of savers a combination of the 0% starting rate band for savings and the personal savings allowance would probably render both the bonus and interest tax-free. But a specific exemption would be preferable to save doing the sums.

Eligibility criteria apply, as set out in Budget 2016 documents: ‘The scheme will be open to… adults in receipt of universal credit with minimum weekly household earnings equivalent to 16 hours at the national living wage, or those in receipt of working tax credit.’

It is not yet clear when the criteria will have to be met – whether only initially or throughout the savings period. We are told that funds will be accessible by the saver ‘to cover urgent costs and there will be no restrictions over how… funds are used’.

Lifetime ISA

The criteria of lifetime ISAs are different from Help to Saves. The scheme is not linked to income; it is available only to those under 40; and the ‘tax-relief’ or ‘bonus’ of 25% will cease at age 50.

Accessibility and use of the funds will be restricted: they have to be put towards the purchase of a first home if they are withdrawn before age 60. Access can be earlier, but with a clawback of tax relief and a 5% charge. Much more can be saved, however, than through Help to Save – up to £4,000 a year (plus £1,000 tax relief).

Pensions and automatic enrolment

Most ‘eligible jobholders’ – generally those from 22 to state pension age and earning more than £10,000 a year – will now or soon be automatically enrolled into a workplace pension.

They will benefit from a tax-free employer contribution. Their own contribution may be boosted by tax relief but this depends on how much they earn and whether their employer is operating a net pay arrangement or relief at source. Under the latter, tax relief of 20% is added to the worker’s pension fund even if they are a non-taxpayer. By contrast, under a net pay arrangement a non-taxpayer will not benefit from tax relief because contributions are deducted from gross earnings and paid to the scheme administrator.

When comparing savings options, a crucial factor in the ‘better off calculation’ is that pension contributions are deductible from earnings when calculating income for universal credit (UC) (other types of saving are not so deductible). UC’s ‘taper rate’ of 65p in the pound means that a £100 pension contribution could result in a £65 increase in the individual’s UC award.

Sifting through the options

So where should the low-income worker start when choosing between Help to Save, the lifetime ISA or pension contributions?

First, it would seem sensible to rule out a lifetime ISA for someone eligible for Help to Save unless they can afford more than the latter’s maximum £50 a month. The lifetime ISA’s lower rate of government top-up plus its restrictions and potential charges on withdrawal render it an unlikely choice for those on the lowest incomes.

This leaves us comparing Help to Save with pensions. A saver could put something into each but practicality probably dictates choosing one or the other when saving only a relatively small amount.

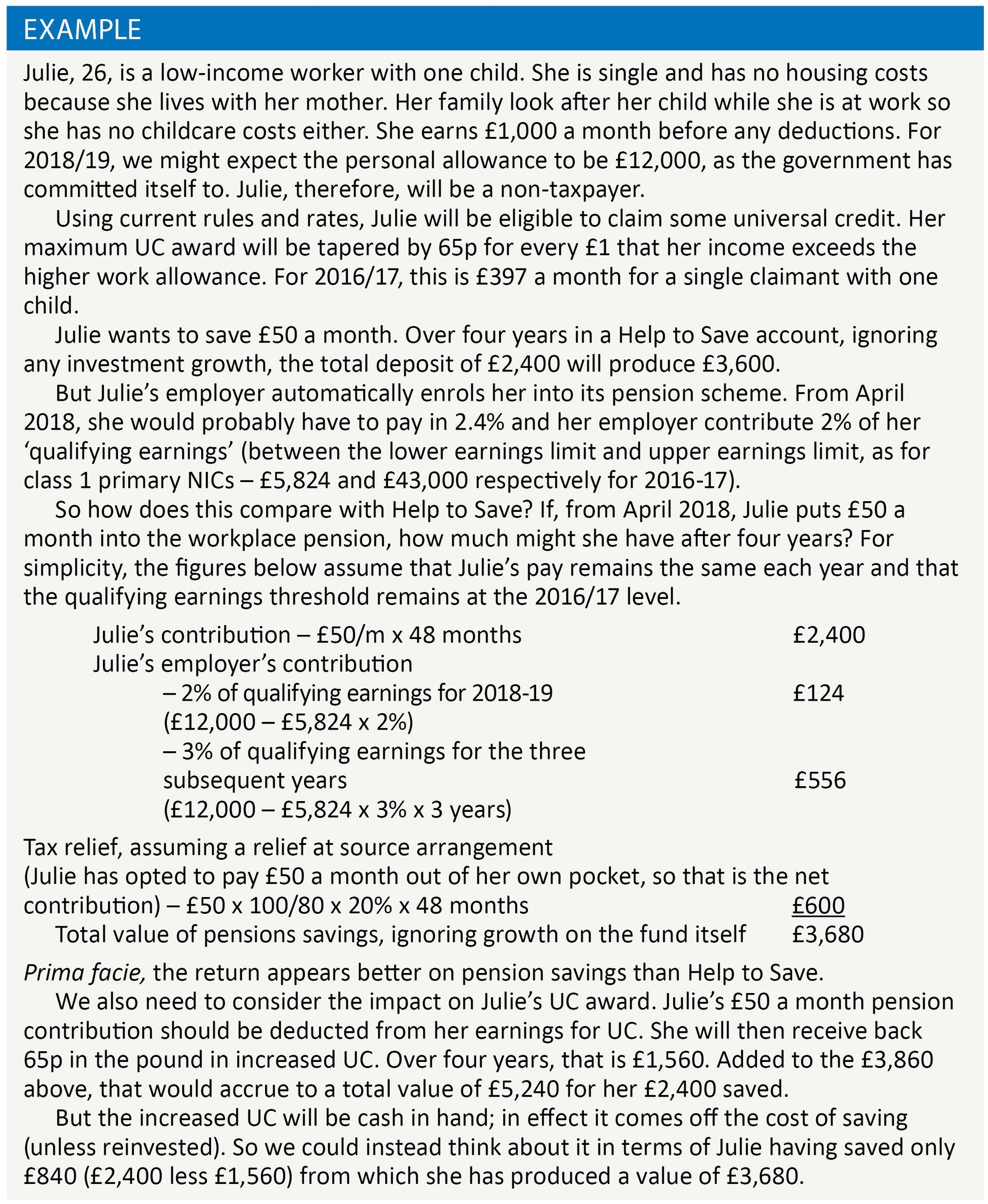

Given the lag between the announcement of Help to Save and its introduction, in order to work through an example we will have to fast forward to April 2018 (see the example).

One might think that double benefit could be had by saving the maximum into the Help to Save scheme, then putting the funds into a pension. Since the use of Help to Save funds are unrestricted, that would appear possible. But a one-off pension contribution by transferring Help to Save funds as a lump sum might not be as beneficial for UC, given that this is calculated monthly. If the pension contribution were to reduce that particular month’s income below the standard allowance at which UC begins to be tapered away, there would be no positive impact on the UC award. This might therefore negate the £1,200 bonus achieved through Help to Save.

Many low-income workers have more than one job. Let’s say Julie above earned £6,000 a year in each of two jobs, making her a ‘non-eligible jobholder’. She could opt in to her employers’ pension schemes and benefit from an employer contribution on each, but she will not be automatically enrolled. This is because she is earning above the lower earnings limit (£5,824 for 2016/17) but below the earnings trigger of £10,000 for automatic enrolment (gauged on each job, assuming they are unconnected).

Since employers need make only minimum contributions on qualifying earnings – above the LEL – this would wipe out most of the £680 employer contribution in the calculations for Julie above.

Moreover, if she were earning beneath the LEL, Julie would be an ‘entitled worker’ – that is, able to join employers’ pension schemes but not qualify for an employer contribution

The self-employed

The self-employed would not benefit as much from pension savings for the obvious reason that there is no employer contribution – not only that, but they would need to take extreme care in assessing the UC position when making pension contributions due to the minimum income floor (MIF) for ‘gainfully self-employed’ claimants.

If the MIF is applied and the individual’s income from self-employment falls below the set level (in general, this is 35 hours x national living wage less notional tax and NICs), they are deemed to have earnings equal to the MIF in the UC calculation. Unlike tax and NICs, pension contributions are not deductible when calculating the MIF. So if a claimant’s income is already near or below that minimum, the pension contribution may have little or no positive effect on their award.

A further UC consideration

Unlike tax credits, entitlement to which is assessed on income alone (ignoring capital), UC is based on a much wider test of claimants’ means. Claimants with more than £16,000 in ‘capital’ (unless it is disregarded) will not qualify. Claimants with ‘capital’ of £6,000 to £16,000 are deemed to receive ‘tariff income’ from it and their award is reduced.

For claimants below state pension age, untouched pension savings are disregarded in the capital assessment under Universal Credit Regulations 2013 Sch 10 para 10.

So, unless the regulations are amended such that Help to Save funds are similarly disregarded, this is another point in favour of pension savings.

Are we any clearer?

Pension saving would appear the ‘winner’, especially if some of the amount is returned by way of increased UC. Another point in favour of automatic enrolment is the deduction of contributions directly from wages. It is psychologically much harder to save out of your net pay than to have never had the money. This could be one reason why pension savings rates are so poor among the self-employed and why there are calls to extend some form of automatic enrolment to them.

But it would be unwise to conclude generally that pensions are preferable to Help to Save. No doubt some may still prefer the more accessible Help to Save scheme, albeit subject to seeing whether further strings are attached after the consultation.

Take Julie in our example. Flexible access to savings might be crucial if her circumstances change – let’s say her family is no longer able to take care of her child while she works. Although she might be able to claim extra UC to help with those costs, this is paid monthly and there could be a delay between the claim and payment. She will also need to supplement the cost herself since UC childcare payments cover only 85% of the cost and are subject to an overall cap.

Consider also the tax position on withdrawal – apparently, Help to Save will be tax-free to access, as against potentially only 25% of a pension fund being tax-free.

There are many other factors to take into account such as age, access to the funds and the longer-term prospects of financial security. With pensions flexibility, savers at least only have to consider the age restriction on accessing their savings given that the pot itself is now accessible in full, even though 75% of it could be subject to tax.

Many may consider saving small amounts into a pension a rather fruitless exercise if they are unlikely to amass much of a retirement nest egg. Indeed, if savings were to exceed future capital or income limits for assessment of entitlement to state benefits, the up-front tax and UC advantages of their saving might quickly be eroded by restriction of future claims.

Unfortunately, it would take an extremely sophisticated calculator to help savers decide on the best route for them. It would have to take account of current and future tax position, likely benefits entitlement, personal circumstances, interest on current debts and many other factors. We could – and will – call for better guidance to the public on how to make these decisions, but is that the answer?

One improvement may be to have a single form of tax-incentivised saving. There will always be personal factors and future unknowns that are impossible to quantify. But at least simpler savings options would eliminate one unknown and give people a better chance of making the best decisions for them.

Further information

Members’ thoughts on this topic are welcome – email [email protected].

LITRG’s guidance for advisers grappling with tax-related benefits issues, including tax credits and their transition to universal credit, can be found at www.revenuebenefits.org.uk.