The scope of inheritance tax: a new residence-based system

Share this article

In the second of two articles on fundamental reforms to the taxation of non-UK domiciled individuals, we examine how long-term residence will replace the concept of domicile when determining inheritance tax.

Key Points

What is the issue?

From 6 April 2025, a new residence based system will be introduced for inheritance tax purposes.

What does it mean for me?

Under the new system, non-UK assets will be within the scope of inheritance tax if an individual qualifies as a long-term resident (defined as being UK resident for ten out of the previous 20 years). Individuals who leave the UK will remain within the scope of inheritance tax for a period ranging from three to 10 years after their departure. Trusts holding non-UK assets will also be subject to inheritance tax charges at relevant chargeable events if the settlor is a long-term resident (subject to certain transitional provisions for trusts settled prior to 30 October 2024).

What can I take away?

Individuals should review the impact of the changes on their affairs and consider a range of matters (including how assets are held, succession arrangements, timing of transactions, liquidity needs and mobility considerations) as part of a broader family succession plan.

From 6 April 2025, the concept of domicile as a connecting factor for inheritance tax purposes will be replaced with the concept of a long-term resident.

UK assets will always remain within the scope of inheritance tax, as under the current rules. The test of whether non-UK assets are within the scope of inheritance tax will be whether an individual qualifies as a ‘long-term resident’. An individual will be treated as a long-term resident once they have been resident in the UK for ten out of the 20 years prior to the taxyear in which a chargeable event (such as death) arises.

Whether an individual is considered a resident in a tax year will be determined using the same rules that apply for income tax and capital gains tax. The statutory residence test will be relevant from 6 April 2013 onwards. For tax years prior to 6 April 2013, the pre-statutory residence test rules will apply.

Once an individual has acquired the status of a long-term resident, their worldwide assets will effectively fall within the scope of inheritance tax from the 11th year of UK tax residence. This means that individuals who do not wish to acquire the status of a long-term resident will need to plan on the basis that they do not remain UK resident for longer than nine tax years in any 20 year period, as residence in any part of the tenth year will bring them within the scope of the long term residence rules.

As a result of these changes, non-UK domiciled individuals residing in the UK will become subject to inheritance tax on their worldwide assets sooner than under the current inheritance tax rules – ten years instead of 15 years.

The long-term residence test applies irrespective of an individual’s common law domicile. Therefore, there is encouraging news for UK domiciled individuals who have been, or will be, non-UK residents for ten years, as they may no longer be liable for inheritance tax on their non-UK assets.

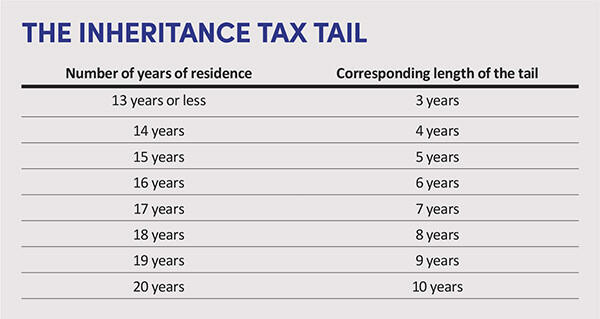

Inheritance tax tail

Once an individual who has become along-term resident leaves the UK, their worldwide assets will remain within the scope of inheritance tax for a number of years, commonly referred to as the ‘inheritance tax tail’. The length of this tail depends on the duration of the individual’s residence in the UK.

The minimum length of the tail is three years, which applies to individuals who have been UK residents for ten to 13 of the past 20 UK tax years. The length of the tail increases by one tax year for each additional year of residence, up to a maximum of ten years. See The inheritance tax tail.

There are special transitional rules for non-UK domiciled or deemed domiciled individuals who are not resident in the tax year 2025/26 and do not return to the UK. These individuals will be subject to the three-year tail (as currently applies), regardless of how many years they have been resident in the UK prior to 6 April 2025.

To benefit from these transitional rules, they must still demonstrate that they are not domiciled in the UKunder common law on 30 October 2024. Therefore, the concept ofdomicile will continue to be relevant for these purposes. Demonstrating a non-UK domicile can be an onerous task and in judgmental cases it is prudent for taxpayers to take advice ontheir position and to keep contemporaneous evidence.

Once an individual has lost their inheritance tax tail, assets owned by them personally and via trust structures will become excluded property for inheritance tax purposes. However, where assets are held via a trust, there can be an exit charge for inheritance tax purposes.

Inheritance tax regime for trusts

Under the current rules, non-UK situated property will be excluded from inheritance tax provided that the settlor was non-UK domiciled at the time the assets were transferred to the trust.

From 6 April 2025, the excluded property status of non-UK assets settled into trust will depend on whether the settlor is treated as long-term resident at a time when a chargeable inheritance tax event occurs. When the settlor is along-term resident, any assets they have settled will be within the scope of inheritance tax. This means that settled assets come in and out of inheritance tax charges based on the settlor’s long-term residence status in the UK at the time of a charge.

Where trust assets fall within the scope of inheritance tax, there are two separate charging regimes that need to be considered.

1. Relevant property regime

Under this regime, assets fall within the scope of inheritance tax charges of up to 6% on every ten-year anniversary of the trust creation and when capital distributions are made from the trust. The calculation of the charges will reflect the number of years that the non-UK property was excluded, resulting in lower charges during the early years of the operation of the new rules.

If the settlor of a trust has died before 6 April 2025, the excluded property status of non-UK assets will be determined based on the old test, which considers the settlor's domicile at the time the property was transferred to the trust. If the settlor of a trust dies on or after 6 April 2025, the excluded property status will not be available if the settlor was a long-term resident in the UK at the time of death.

From 6 April 2025, if a settlor ceases to be a long-term resident and non-UK relevant property held within a trust becomes excluded property, this will trigger an inheritance tax exit charge. The inheritance tax charges in this scenario will be capped at a maximum of 6%, reduced proportionally by the number of quarters to the next ten-year anniversary of the trust’s creation, while also reflecting the period during which the property qualified as excluded property.

The relevant property charges (including exit charges) apply not only to non-UK domiciled individuals who cease being UK tax resident from 6 April 2025 onwards, but also to those who left the UK before this date but remain within the scope of inheritance tax on non-UK assets for three years after their departure under the current inheritance tax rules.

2. Gift with reservation of benefits rules

Where the settlor is not excluded as a beneficiary of the trust, assets will be included in their estate for inheritance tax purposes and taxed at rates of up to 40%.

Under the transitional rules, non‑UK assets settled into a trust before 30 October 2024 will not be subject to the gift with reservations provisions. Therefore, there will be no 40% charge on the settlor’s death if they are a long-term resident. However, such trusts will still be within the scope of relevant property charges of up to 6%, as noted above. Accordingly, the grandfathering of trusts settled prior to 30 October 2024 is only partial and does not remove the exposure to inheritance tax under the relevant property regime.

Estate treaties

The government has indicated that there will be no changes to the operation of the estate tax treaties concluded by the UK. Consequently, the common law concept of domicile will continue to be relevant for determining whether an individual is considered domiciled for the purposes of these treaties and whether the UK has the right to impose inheritance tax on the individual’s estate. Notably, some estate tax treaties provide protections for settled property after a settlor becomes along-term resident in the UK.

Reform of agricultural property relief and business property relief

Many non-UK domiciled individuals own trading and farming businesses outside of the UK. As such individuals may fall within the scope of worldwide taxation for inheritance tax purposes from 6 April 2025, they need also to consider whether agricultural property relief and business property relief may be available.

In this regard, it is important to notethat the UK government has also announced reforms to agricultural property relief and business property relief, effective from 6 April 2026. The 100% relief for qualifying assets will be capped at £1 million of combined value in an individual’s estate. Any value above this threshold will receive only 50% relief, potentially resulting in an effective inheritance tax rate of 20% on excess personally held assets and 3% for business and agricultural assets held by trustees.

Key actions to consider prior to 6 April 2025

Succession matters are always high on taxpayers' agendas. The inheritance tax reform coming into effect from 6 April 2025 necessitates a reevaluation of traditional routes, such as trusts, commonly used by non-doms for asset protection and succession purposes. It is essential to consider alternative strategies in light of these changes.

As decisions on succession involve factors that extend beyond tax considerations – such as wealth protection, heir readiness and family dynamics – the primary challenge is to weigh all relevant factors and make a balanced decision within this limited timeframe.

Putting fundamentals in place

Individuals who fall within the scope of inheritance tax concerning non-UK assets need to review their worldwide will arrangements, considering factors such as the availability of spousal exemption. This process can be particularly complex for those with assets and family members spread across multiple locations.

Additionally, some individuals may consider obtaining life insurance to cover inheritance tax liabilities arising from both lifetime and death transfers of assets. As this is a regulated area, individuals will require specialist financial advice.

Lifetime gifting

Under general principles, lifetime gifts of assets do not attract inheritance tax if the donor survives for seven years following the gift. However, these rules are not applicable when the gift involves excluded property.

Some taxpayers may wish to consider whether it is timely to make lifetime gifts of excluded property to the next generation while the current rules are in place, prior to 6 April 2025.

Reviewing succession arrangements

Trusts have been historically used by non-UK domiciled individuals, given their asset protection, governance and succession impacts. However, given the extension of inheritance tax charges to trusts where the settlor is a long-term resident, as well as the removal of trust protections for income tax and capital gains tax (as outlined in the first article), the tax landscape for trust structures will significantly change from 6 April 2025.

Accordingly, some individuals may wish to revise their existing succession arrangements and consider alternatives to trusts, such as a family investment company or partnership. These alternatives come with their own distinct tax and legal frameworks and may be more suitable for certain taxpayers moving forward.

Where there are existing trusts, the trustees may need to consult with the settlor and/or beneficiaries regarding any changes.

Considering transitional provisions applicable to individuals leaving the UK

Individuals who decide to leave the UK and become non-UK tax resident from 6 April 2025 will be subject to transitional provisions relating to the reduced inheritance tax tail. As noted in the first article, such individuals will need to take care to comply with the statutory residence test. From an inheritance tax perspective, they need to review their common law domicile, as the transitional rules do not apply to individuals who are UK domiciled under common law on 30 October 2024. Furthermore, where such individuals are settlors of a trust, anexit charge may arise when they lose the inheritance tax tail.

Considering the impact of the estate treaties

Where individuals are domiciled outside of the UK for the purposes of the relevant treaties, protection from inheritance tax may be available even after they become long-term residents in the UK. As recent case law indicates, demonstrating non-UK domicile status may prove to be challenging for individuals who stayed inthe UK long term. A detailed review ofthe relevant estate treaty and its qualifying conditions would be required to confirm the position. Where relevant, a review of domicile position is also necessary (in the UK and/or the relevant treaty partner country).