Seemingly simple

Share this article

A reminder and update on seemingly simple intangible fixed assets

Key Points

What is the issue?

Intangibles generally follow the accounting treatment but tweaks round the edges in recent and coming years have muddied the water.

What does it mean to me?

The ‘new’ intangibles regime is not only relevant to technology and media companies, but also any company in a business combination.

What can I take away?

A reminder of key aspects of the intangible fixed assets regime, transitional provision, beneficial claims and elections and an awareness of changes on the horizon.

Scope of the regime

Assets within the ‘new’ intangible fixed assets (IFAs) regime are those treated as intangible assets for accounting purposes. Both FRS 102 and IAS 38 define an intangible asset as an identifiable non-monetary asset without physical substance. However, only assets created or acquired on or after 1 April 2002 are ‘new’. For most assets, identifying the date of creation or acquisition is simple. In the case of goodwill, it is created before 1 April 2002 if the relevant business was carried on by a company or a related party before that date. Otherwise, it is created on or after 1 April 2002 and within the scope of the regime.

Exclusions from the regime apply in one of three ways: total (e.g. assets held for non-commercial purposes and shares), only as respect royalties (e.g. sound recordings) or in another specific manner (e.g. no debits on goodwill acquired on or after 8 July 2015 apart from realisation debits which will always be treated as non-trading IFA debits – see below for more).

Basic rules: where tax cost and NBV equal accounts cost and NBV

Debits and credits

As with general trading income rules, the starting point is the GAAP-compliant accounts drawn up by the company. Debits and credits released to the company’s GAAP-compliant profit and loss account are generally allowable or taxable respectively.

Taxable credits include receipts from royalties, revaluations gains and gains on a bargain purchase credited to the profit and loss account.

Allowable debits usually take the form of amortisation or impairment charges of capitalised expenditure.

Realisation

A sale, disposal or any other kind of transaction in an IFA that results in it ceasing to be recognised on the company’s balance sheet is referred to as a realisation. There are three possible calculations of the realisation.

If debits have previously been allowed for tax purposes then the realisation debit or credit is equal to any proceeds received less the tax-written down value at the date of derecognition. Provided the historic tax debits have equalled the accounting debits, no tax adjustment to the profit on disposal will be required.

If debits have not been allowed in respect of the asset, e.g. goodwill acquired on or after 8 July 2015, the tax gain/loss is equal to proceeds less cost. If the asset has been amortised in the accounts, this will require an adjustment to profits to reduce the accounting gain by the amount of amortisation previously posted through the accounts but not allowed for tax purposes.

For assets not recognised on the balance sheet, for example internally-generated goodwill sold in a trade and asset transfer, a credit equal to the proceeds attributable to the asset is taxed.

Trade vs non-trade and losses

Debits and credits, including those on a realisation, in respect of trade IFAs are taxed or deducted from the relevant trade profits results. Any losses arising from these are therefore within the trading loss rules following any other adjustments.

Non-trading credits and debits (which will always include losses on disposal of goodwill which was acquired on or after 8 July 2015) are netted. If the result is a gain, it is charged to corporation tax. If the result is a loss, it can be set in whole or part against the company’s total income, by claim, within the usual two year period. It can also be the subject of a current year group relief claim. If and to the extent it is not the subject of such claims, it is carried forward and treated as non-trading loss on IFAs for the next period.

Prior to 1 April 2017, the loss was instead carried forward as a non-trading debit on IFAs and was therefore effectively used first against non-trading credits in subsequent periods. From 1 April 2017 onwards, the loss retains its flexibility year-on-year. Such a loss carried forward can now be the subject of a group relief claim for carried-forward losses under the new CTA 2010 Part 5A.

Variations to basic rules

The effect of the basic rule to follow the accounts treatment is that, generally, the tax cost and accounts cost, and by extension the tax written down value and net book value, of an asset will be equal. However, the tax values can differ from the accounting values due to the application of a number of provisions. The most common are the straight-line writing down election, roll-over relief claims and the transfer pricing rules. These complicate the calculation of profits chargeable to corporation tax and may have deferred tax implications when provisioning.

4% writing down election

Instead of allowing debits as the assets are amortised or impaired in the accounts, an election can be made to write down an asset for tax purposes at a fixed rate of 4% per annum of the cost. The choice is made irrevocably from the initial recognition of the asset and on an asset-by-asset basis. There is no requirement for the asset to be written down in the accounts of the entity. The election must be made within two years of the end of the chargeable accounting period in which the asset is initially recognised.

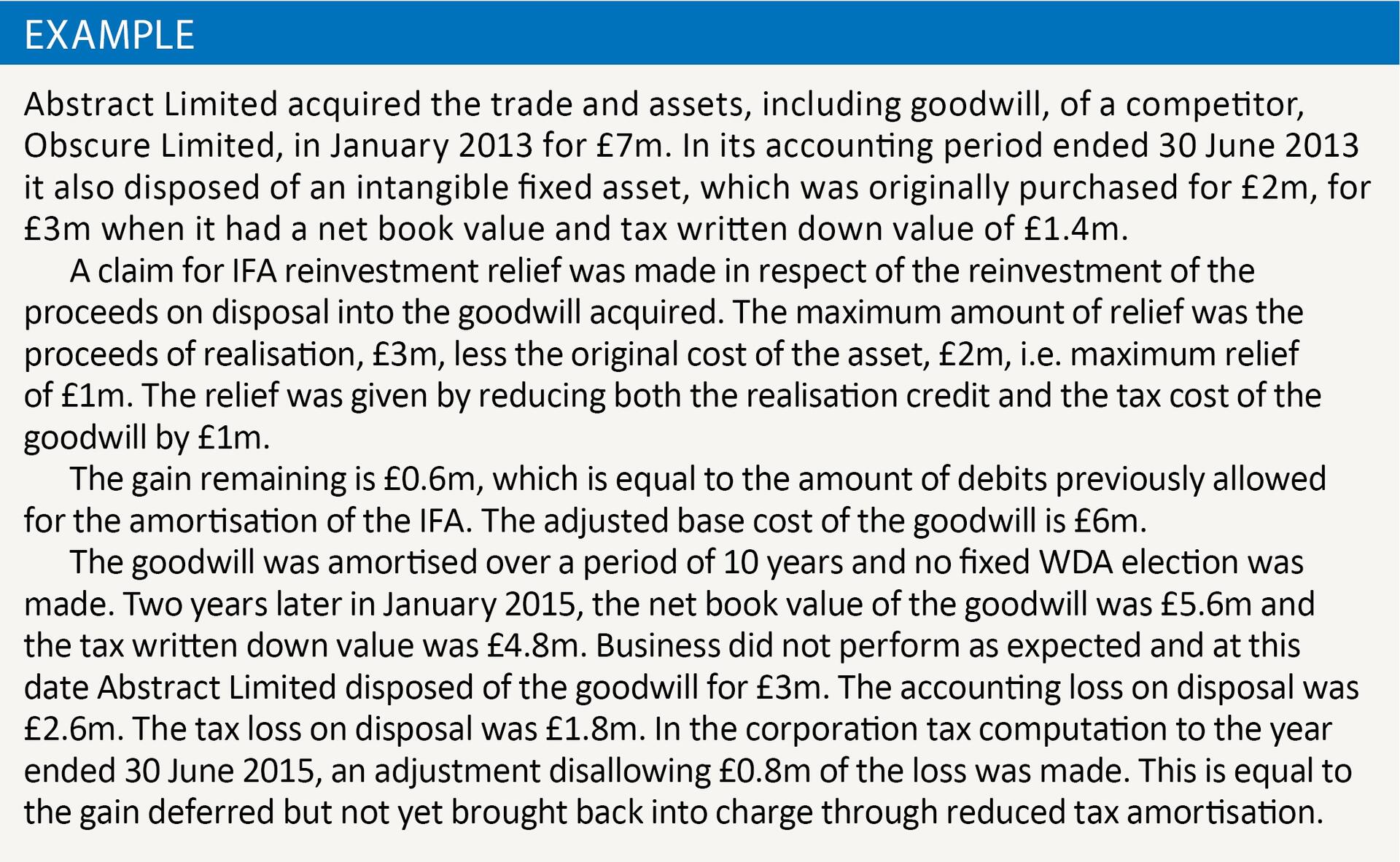

Roll-over relief

The IFA regime includes a claim for a deferral relief on realisation credits which closely mirrors the replacement of business assets relief in TCGA 1992 s 152 et seq. The old IFA must have been within the IFA regime, i.e. not wholly excluded, and the proceeds on sale must exceed the original cost. Claims can also be made where the old asset is an IFA created or acquired before 1 April 2002.

Reinvestment can be made into one or more IFAs capitalised in the accounts of the company which are within the IFA regime after the expenditure is incurred. The reinvestment must be made in the period running from 12 months preceding the realisation to three years after the realisation. There is no further list of specific IFAs which are qualifying assets – anything chargeable within the regime is acceptable.

If the expenditure incurred on new assets is equal to or greater than the proceeds of realisation, the maximum relief is the proceeds of realisation less the original cost of the old asset, i.e. absolute cash profit.

If the expenditure incurred on new assets is less than the proceeds of realisation, relief is capped at the amount by which the total expenditure on new assets exceeds the original cost of the old asset.

For both calculations, the original cost is taken to be the indexed cost for an old asset that is an IFA created or acquired before 1 April 2002.

In either case, the old asset must be realised for proceeds in excess of the original expenditure incurred on the old asset. This means book profits that arise because the proceeds of sale exceed amortised cost (but are less than original cost) are not eligible for roll-over relief.

The relief must be claimed within four years of the end of the chargeable accounting period in which the old asset is realised or the other assets are acquired, whichever is later. Provisional claims are allowed.

The effect of the roll-over relief claim is to reduce the tax costs, and subsequent tax written-down values, of new assets acquired, impacting on calculations of profits chargeable to corporation tax and possibly creating timing differences and a deferred tax liability thereon.

Groups and related parties

The group provisions for IFAs are also similar to TCGA 1992 provisions. A group includes a principal company and its 75% subsidiaries and their 75% subsidiaries and so on, as long as they are effective 51% subsidiaries of the principal company. Companies can only be members of one group.

Transfers between two companies that are members of the same group are tax neutral, meaning that:

- The transfer is neither a realisation nor an acquisition,

- The transferee inherits the original cost and historic credits and debits brought into account of the asset from the transferor (important for any future roll-over relief claims on subsequent realisations), and

- The transferee is treated as having always owned the asset.

Roll-over relief on IFAs can apply on a group basis. One company can dispose of the old asset and another company acquire other assets. There is also an indirect roll-over relief where a company becomes part of a group as a result of another company acquiring a controlling interest in it. In that case, if the company invested in holds IFAs, this can be treated as an investment in other assets for roll-over relief purposes.

In both of these extensions to roll-over relief, the claim must be made jointly by both companies involved.

One key difference between IFAs and chargeable assets is the treatment of degrouping charges. The principle is the same: a company (transferee) leaves a group and at some point in the six years prior to it leaving the group there has been a tax neutral intra-group transfer of an IFA to it. The charge arises if the company leaves still holding the asset.

The transferee is deemed to have made a market value disposal of the IFA immediately after the intra-group transfer and immediately reacquired it for the same value. The resultant credit or debit is brought into account immediately before the transferee ceases to be a member of the group.

The crucial difference is that, where the company leaves the group as a result of a sale of its shares, TCGA 1992 s 179 degrouping charges are added to the disposal proceeds on the sale of shares, and the degrouping charge is therefore usually exempt under the substantial-shareholding exemption. No such provision applies to exempt IFA degrouping charges which are charged as trade or non-trade IFA credits as described above.

The degrouping charge can be treated as the realisation of an old asset for roll-over relief purposes. In addition, a joint election can be made between the transferee company and another UK resident company in the group it is leaving to transfer the whole or part of a degrouping charge to the company remaining in the group. Such a reallocated charge can, in turn, be treated as a realisation by the remaining company of an old asset for roll-over relief purposes.

Goodwill and customer-related intangibles: changes on the horizon

As described above, no debits are allowed on goodwill acquired on or after 8 July 2015 except for debits on realisation, which are always treated as non-trade. This rule applies to goodwill, customer or marketing lists, customer relationships, unregistered trademarks and licences or other rights in relation to any of the above assets. The effect of this together with the 1 April 2002 watershed has created three possible treatments of goodwill.

The Office for Tax Simplification has questioned whether this is really necessary or whether simplifications could be made without a material impact on HMRC’s receipts.

The government announced at the Autumn Budget 2017 that it will consult on the current IFA regime in 2018 although the precise scope is not yet clear. Further changes can be expected in the form of alterations to the OECD’s transfer pricing guideline in response to BEPS action point 8 – hard-to-value intangibles.