Shifting sands

Share this article

Stephen Woodhouse and Charlotte Fleck consider the recent changes to Entrepreneurs’ Relief over the past year

Key Points

What is the issue?

Entrepreneurs’ Relief (ER) has become a focus for reform over the past year.

What does it mean to me?

Some have recommended that it be abolished on the basis that the availability of the relief does not sufficiently influence the decisions of entrepreneurs to establish new ventures while the costs of the relief (estimate at £2.7bn) could be better used in other areas.

What can I take away?

The relief has survived the threat of abolition – for now – but with significant changes. The changes reflect a mix of positive effects with a potentially substantial restriction of the relief which may not have been fully appreciated.

Entrepreneurs’ Relief (ER) has become a focus for reform over the past year. Some have recommended that it be abolished on the basis that the availability of the relief does not sufficiently influence the decisions of entrepreneurs to establish new ventures while the costs of the relief (estimate at £2.7bn) could be better used in other areas – see Resolution Foundation Report.

The relief has survived the threat of abolition – for now – but with significant changes.

Qualification Period

The qualification period during which the requirements for claiming relief has to be satisfied has increased from one year to two years.

This applies to disposals of shares after 6 April 2019 regardless of when those shares were required, which may verge on having retroactive effect for individuals who acquired shares more than one, but less than two years ago. Overall, the change might be expected to have a limited impact as most shareholdings which have benefitted from a significant increase in value might be expected to have been held for at least two years – and it’s understandable that a relief focussed on entrepreneurs requires more than 12 months’ ownership.

Also, this change will not affect claims for relief in respect of shares acquired through the exercise of EMI options as the qualification period does not apply to them.

Dilution protection

The provisions to protect ER in the event of a shareholder being diluted below the 5% personal company threshold (see below) were discussed in an earlier article (‘Breaking Barriers’, Tax Adviser, December 2018).

The effect of the changes is that, for dilutions occurring on or after 6 April 2019 which result in an individual’s shareholding falling below the 5%, an individual may effectively ‘crystallise’ their gain up to that point. The individual must elect for their shareholding to be treated as disposed of and reacquired immediately before the point of dilution (thus creating a chargeable gain to which ER may apply).

A second election may be made by the individual for that chargeable gain to be treated as accruing to them on a subsequent disposal of shares. This effectively prevents a ‘dry’ tax charge from arising on the notional disposal of the shares, with no proceeds of sale to cover the tax.

Personal Company Requirements

The third – and potentially most substantial – change relates to the requirement for the person claiming the relief (other than in respect of shares acquired through EMI options) to have a minimum 5% interest in the share capital of the Company.

This condition has, since the inception of ER, only required the shareholder to have a 5% interest in the nominal value of the Company’s share capital and its voting rights. This was clear from the legislation and recognised as such by HMRC.

The law has now been extended to encompass a requirement for the individual to be entitled to receive either:

- 5% of the dividends and assets available to ‘equity holders’ on a winding up of the business (Condition A); or

- 5% of the sale proceeds due to holders of ordinary shares on a notional disposal of the Company (Condition B).

Condition B was introduced at a late stage in order to simplify the determination of whether relief is available and in practice is likely to be the test relied on in most cases.

Impacts

The change which will have the most impact is likely to be the introduction of the 5% economic participation requirement.

This change will have potentially adverse effects on some employee shareholders in successful, high growth companies (in effect, introducing a penalty on success) while also increasing complexity and creating the risk of the structure of companies and financing arrangements being influenced more by tax than commercial considerations.

Impact on growth companies

The difficulty for growth companies results from the impact of the economic participation requirement linked to the effect of the dilution protection capping relief to the value of the shares at the time the dilution happens.

The problem with this is that the value of growing companies tends not to increase consistently over the life cycle of the Company. Rather, there will be value jumps as particular milestones are reached – including capital raising – with the result that capping the relief at the point when new funding is obtained may result in the biggest part of any overall gain not benefitting from the relief. Further, the scope to mitigate this is reduced by requiring an economic 5% participation.

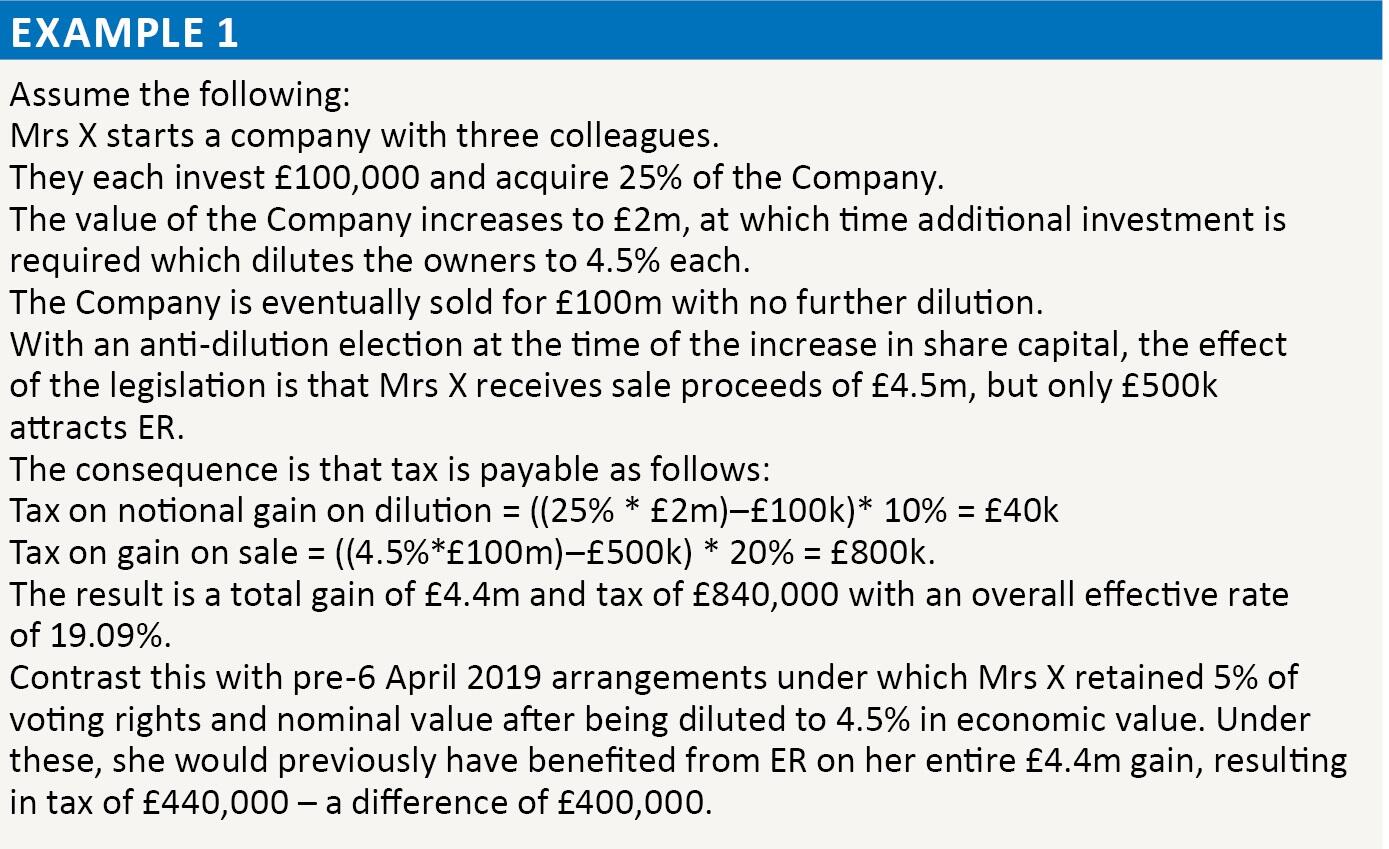

This is illustrated by example 1. With this potential impact on effective tax rates, it is to be expected that there will be a concentration on the applicability of the new legislation. This has a number of further impacts.

Condition A

The application of the 5% test is likely to be relatively straightforward with companies with a single class of ordinary share and it may be that Condition A may be met. However, if the first condition is to be relied on, particularly with multiple share classes, difficulties may arise.

For example, the test applies to the notional entitlement to distributions rather than actual distributions made. This will require the notional entitlement to be tested at all times throughout the two year qualification period taking account of the circumstances applying at each stage. This may be determined by factors which are external to share rights per se – e.g. the financial performance of the Company – which may make this difficult to assess.

Also, if there is more than one class of share with discretionary dividend entitlements determined by the Directors, it is arguable that this condition will never be fulfilled as, at any one time, the holders of neither class could demonstrate entitlement to share in dividends which could instead be allocated to the other class or classes.

Further, the test applies by reference to the definition of ‘equity holders’ calculated by reference to the corporate tax rules concerning group relief with the individuals claiming relief replacing the parent company in the calculations required. With any share structure other than a simple, single class, this is likely to result in complex calculations requiring specialist advice.

Use of loan capital

The legislation increases the risk of the legislative requirements resulting in a distortion of the commercial structure of companies to ensure that relief is protected.

For example, companies may wish to seek loan financing rather than increase their share capital. This would be intended to result in the return payable on the loan capital being excluded from the calculation of the 5% calculation for all of profits available for distribution, assets available on a winding up and the proceeds of sale of the whole of the ordinary share capital of the Company.

This may lead to additional complications – e.g. with the accounting treatment and the prioritisation of participation in assets in the event of an insolvent liquidation – and potential risks with the anti-avoidance legislation and DOTAS rules considered below.

Condition B

For this reason, in many instances, reliance would be placed on Condition B relating to the share of sale proceeds.

The legislation tests the application of sale proceeds based on the market value at the date of sale – i.e. in effect, the share of those proceeds – but this must still be tested throughout the two year qualification period leading up to sale by reference to the circumstances applying at all times to a notional sale. That is, it is necessary to test whether, if the company had been sold at the beginning of the two year period for the value for which shares were sold at the end of that period, would the shareholder have received 5% of the proceeds?

Impact on Forfeiture Provisions

This creates a particular problem with forfeiture and vesting conditions for employee shares.

Let us assume that employee shares for a senior employee whereby that employee acquires 5% of the share capital immediately, but subject to forfeiture in accordance with a vesting schedule under which 20% of the shares vest each year, but with discretionary early vesting at the determination of the Board of Directors in the event of a sale prior to vesting.

With that structure, it would appear that the shares would only attract ER if there were no company sale until seven years after the shares were first acquired (due to there being no right to share in sale proceeds for unvested shares without the exercise of discretion), even if tax and national insurance contributions are paid on the full value without any reduction for the effect of forfeiture due to an election being made for them to be ignored under section 431 ITEPA. The corollary to that is that there would be no protection under the anti-dilution legislation if the dilution occurred within the five years following the acquisition.

Favouring option plans

These rules do not apply to shares acquired through the exercise of EMI options. Consequently, the senior member of management in the previous paragraph would not face the seven year wait and loss of relief on an early exit if they had instead been granted EMI options with an equivalent five year vesting schedule.

This is an important point for advisers to consider when designing and implementing share plans. It also produces a result which might be seen as acting against the intent of the ER rules. ER was introduced to ‘incentivise and reward entrepreneurs who, with significant initiative and risk, play a key role in building and growing a company’. It might be thought that with these objectives, the rules should favour individuals who invest and put their money at risk rather than option holders who take no such risk.

Tax avoidance

The legislation provides that the effect of ‘any avoidance arrangements’ is to be ignored. This covers arrangements if ‘the main purpose of, or one of the main purposes of, the arrangement is to secure that …’ broadly, ER is available.

This is a sweeping provision and would seem to limit substantially any planning to secure that the relief applies. For instance, if, as suggested earlier, new investment is structured in the form of loan capital, it could be argued that the loan capital is used with a main purpose of securing the relief, in which case its effect would be ignored and the relief lost.

DOTAS

A further constraint on the development of planning to secure ER would be the possible application of the Disclosure of Tax Avoidance Schemes legislation (or DOTAS). In particular, the use of ‘financial products’ falling within Hallmark 9 of the DOTAS legislation will lead to a requirement to notify HMRC and obtain a DOTAS number if, broadly, there is a tax advantage and either the arrangement involves a contrived term which would not have been entered into but for the tax advantage or one or more abnormal steps without which the tax advantage could not be obtained.

Summary

The effect of the reforms on ER should be considered in combination.

While acting to preserve the relief in the face of recommendations to abolish it, the amendments are likely to result in a more substantial restriction on the value of the relief than was first appreciated.

The changes reflect a mix of positive effects with a potentially substantial restriction of the relief which may not have been fully appreciated.

In particular, the combined effect of the economic participation requirement with the operation of the dilution protection capping relief to the value of the shares at the time the dilution happens creates challenges for successful companies. As values jump as particular milestones are reached – including capital raising – capping the relief at the point when new funding is obtained may result in the biggest part of any overall gain not benefiting from the relief.

Further, the scope to mitigate this is reduced by requiring an economic 5% participation with stringent anti-avoidance rules.

The result is likely to be a substantial reduction in the estimated £2.7bn annual cost of ER and challenges for advisers to ensure that their clients obtain the value of the relief which they would expect.