Spot the difference

Share this article

Kathie Haunton and Sarah Goodman provide guidance in determining which supplier costs can be included in an R&D claim

Key Points

What is the issue?

In practice, R&D claimants often find it difficult to understand how their relationships with third parties fit within the R&D tax regimes. Distinguishing between R&D services provided by externally provided workers (‘EPWs’) and subcontracted R&D activities is particularly important for large company claimants making Research and Development Expenditure Credit (‘RDEC’) claims, where subcontracted R&D can only be claimed in limited circumstances.

What does it mean for me?

Understanding the distinction between the relevant qualifying cost categories will enable companies to consider the nature of their relationship with third party suppliers and other group companies, to ensure that these are appropriately documented and qualifying costs are included in the company’s R&D claim.

What can I take away?

You will need to work out how to identify the fact pattern of arrangements, and the indicators HMRC might expect to see, so that a robust R&D claim is submitted and eligible costs correctly identified.

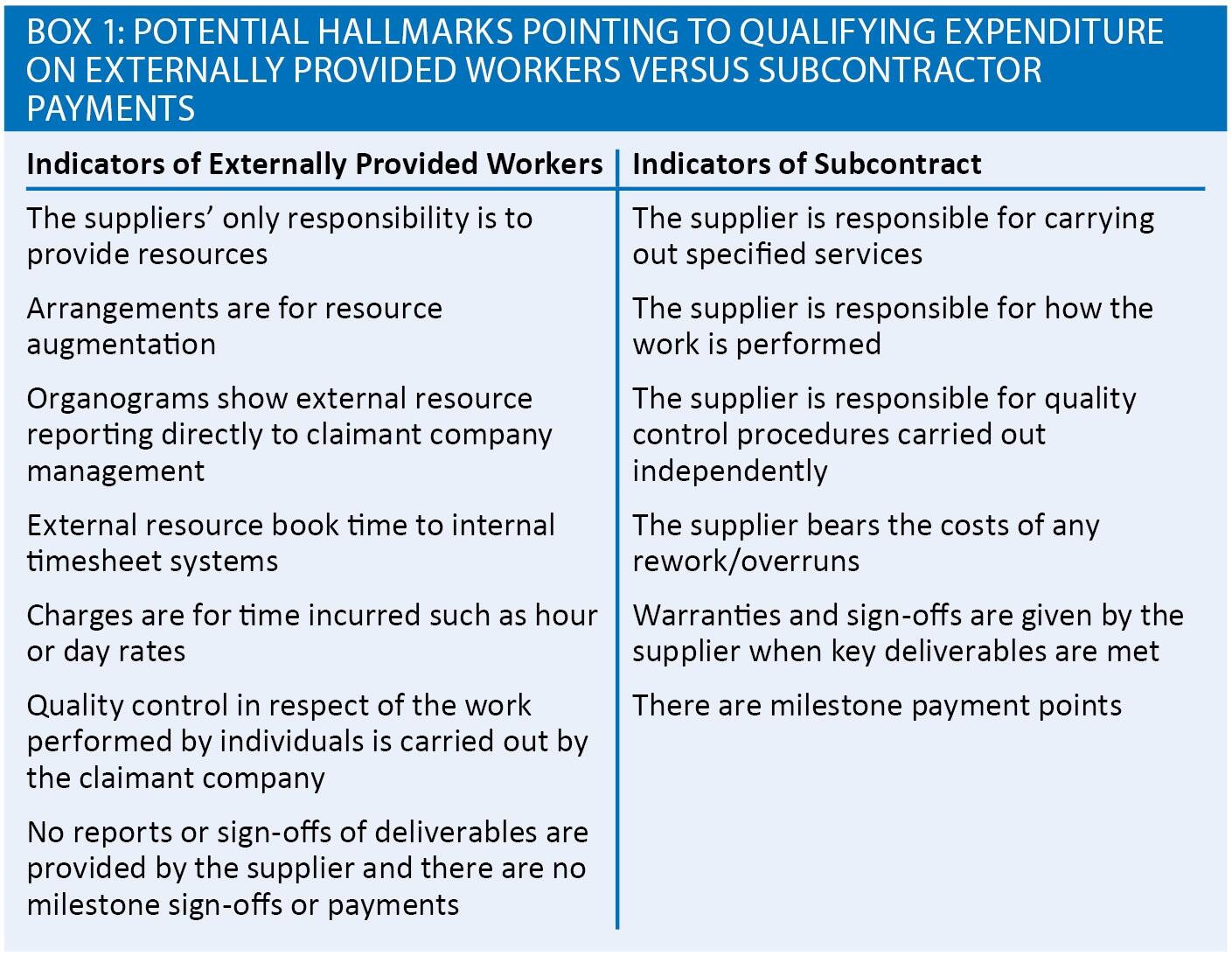

R&D tax relief continues to provide valuable cash incentives to UK businesses; over 240,000 R&D claims have been made since the R&D tax relief schemes were first introduced and £21.4 billion has been claimed in tax relief (HMRC Research and Development Tax Credit Statistics – September 2018). Although many areas of the R&D regime are now well understood, the nature of arrangements with third party suppliers and other group companies can often be difficult to determine. This means that expenditure that could potentially qualify can either be overlooked or non-qualifying costs incorrectly included in R&D claims. See box 1.

We consider below the factors that help to determine whether arrangements with suppliers are likely to be EPW or subcontract in nature, an important concept for companies claiming relief under the RDEC regime. Although costs associated with the supply of EPWs can be included in an RDEC claim, subcontracted R&D costs can only be claimed in a limited range of circumstances. Getting this distinction wrong can mean leaving money on the table if EPW costs are missed. If subcontract costs are incorrectly claimed as EPWs, there is also the risk of repayments and penalties.

The distinction is also relevant for companies claiming Patent Box relief under the new nexus regime. Here, arrangements that reflect an EPW relationship are considered ‘good spend’ to the R&D fraction. In contrast, expenditure on subcontracted R&D to connected persons negatively impacts the R&D fraction and therefore the proportion of profits benefitting from the relief.

Relevant definitions

The conditions for an individual to be an EPW are set out in the legislation at CTA 2009 s 1128 and, in essence, demonstrate that the individual will operate as if they were staff of the claimant company, but on a temporary basis. A staff provider payment exists where the claimant company makes a payment to a group company or an unconnected third party, for the services of individuals.

A person is an externally provided worker in relation to the claimant company if the following conditions are satisfied:

- he/she is an individual;

- he/she is not a director/employee of the claimant company;

- he/she personally provides or is under an obligation to personally provide services to the company;

- he/she is subject to (or to the right of) the supervision, direction or control of the company as to the manner in which those services are provided;

- his/her services are supplied to the company by or through a staff provider (whether or not he/she is a director or employee of the staff provider or of any other person);

- the worker provides, or is under an obligation to provide, those services personally to the company under the terms of a contract between the worker and a person other than the company (the ‘staff controller’); and

- the provision of those services does not constitute the carrying on of activities contracted out by the company.

Most of the above requirements are factual and relatively straightforward. In fact, HMRC guidance (CIRD84100) take the operation of ‘PAYE’ by the staff provider in relation to the worker as indicative that most conditions are met. Unfortunately, not all arrangements are as simple to evaluate and the issues generally arise when considering the more subjective conditions (d and g) , particularly given there is no clear definition of ‘activities contracted out’ or of ‘subcontracted’ activities within the R&D legislation and only limited guidance in CIRD84250.

Practicalities

There are a range of situations where R&D claimants will engage with group companies or external suppliers and HMRC will expect the claimant company to have reviewed the contracts, invoices, group recharges and specific fact patterns when determining whether to claim costs as EPW or subcontract.

The starting point is a review of the contract with the supplier. In reviewing contracts for indications of a subcontract relationship, claimants should look for any definitive commentary on output based arrangements, a high degree of autonomy enjoyed by the supplier in undertaking the work, strict division of responsibility and fixed milestones for payment and delivery. Conversely, for an EPW relationship, it is more likely that the contract references specific numbers of staff and their associated qualifications, the ability for the claimant to closely monitor and supervise work the individuals perform, and the risk and cost of any rework sitting with the claimant company.

It is often the case, however, that the wording of the contract does not clearly or accurately reflect the reality of the working arrangement. Many suppliers will have a template for their contracts or Master Service Agreements, neither of which are likely to have been drafted with the R&D rules in mind. If the supplier is another group company, any contract or inter-company agreement is likely to be even more limited on detail. It is therefore also important to understand the actual nature of the working relationship in practice and the fact pattern of the day-to-day arrangements.

In reviewing the RDEC filing position, conversations should take place with the relevant technical staff to appropriately document what the legislation requires compared to the terms of the contract, how the services are actually delivered and how the delivery of those services supports or overrules the conclusion drawn from the contract. The types of questions and evidence HMRC may consider include:

- where does day-to-day control for the project reside and who has control over the resources used to deliver the project?

- is there flexibility for the claimant to change the requirements of the project as the development work progresses and what degree of autonomy is enjoyed by the persons engaged?

- who will bear the economic risk of irrecoverable additional project costs if services provided do not meet the quality requirements?

- who owns the intellectual property resulting from the R&D activities?

HMRC will expect evidence such as completed timesheets, the daily allocation of tasks and other examples of day-to-day management such as working on first name terms, the ability to request a change of staff and the potential involvement in performance reviews in order to accept costs as EPWs. The level of documentation and support prepared should however be commensurate with the value to be derived from the claim.

The distinction between EPW and subcontract costs is not always relevant for SMEs unless there is a requirement to claim part of the costs under the RDEC, but for those companies that expect to move to large company claims in the near future, considering the way agreements are structured may be important to their later claims.