Spring Budget 2023: some important messages for business and individuals

Share this article

On 15 March, chancellor Jeremy Hunt presented his first Budget. While more orthodox than the previous Budget, it contains some important messages for business and individuals.

After the tax rises from the 2022 changes, the Spring Budget reduces tax by about £13 billion in 2023-24 and each of the two years’ after. The major slice – some £8-10 billion annually – goes on full expensing for plant and machinery over the next three years.

Commentators have pointed out that the forecasts from the Office of Budget Responsibility show there is no margin for error in complying with the current fiscal rules – which no doubt has affected Budget decisions. The forecasts expect that national account taxes will amount to £922 billion in 2022-23 and £950 billion in 2023-24. Two thirds of that comes from income tax, national insurance and VAT.

Perhaps the most important Budget headline is the increased investment in childcare. None of the £4-5 billion annual cost from 2025-26 comes in the form of tax relief – although it places even more focus on the huge penalty from increasing earnings over £100,000. Some estimates suggest that earnings would need to increase by 30% just to cover the withdrawal of childcare and the personal allowance above £100,000.

There is a lot of detail in the Budget documents and there’s more to come. The government will bring forward a further set of tax administration and maintenance announcements later in the spring. None of those announcements will require legislation in Spring Finance Bill 2023 or have an impact on the government’s finances at this stage.

Fuel duty

Extending the 5p fuel duty cut for a further year costs a whopping £4.8 billion next year and £2.5 billion annually thereafter. Fuel duty is one of those taxes which is spread very broadly – so it costs a very large amount to deliver comparatively low amounts to individuals with petrol or diesel cars (about £100 to the average motorist in both the current year and next year). In 2021, it is estimated that 45% of households had access to one car or van, with a further 33% having two or more vehicles (see bit.ly/4075v2X). 22% of households did not have a car or van. A large saving also goes to road hauliers, of course.

The OBR estimates that the cumulative cost of freezing fuel duty rates between 2010-11 and 2023-24 relative to increasing them in line with RPI inflation has risen to around £80 billion, after factoring in the expected reduced demand for fuel due to higher duty rates. Many have questioned why our forecasts continue to assume that fuel duty will increase annually with inflation, given that record.

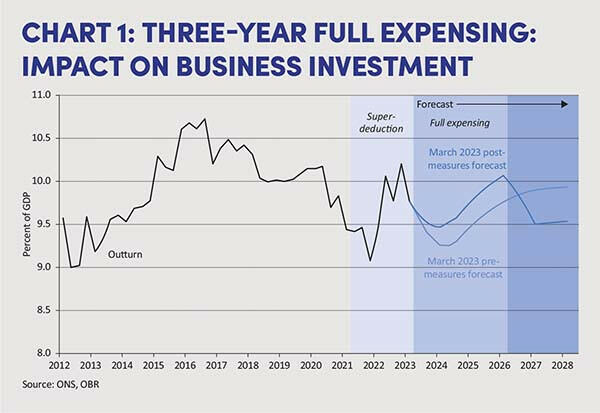

Investing in plant and machinery

In 2021, the government introduced the 130% super-deduction to encourage companies to invest. This ends on 31 March 2023. The government is now introducing full expensing – a 100% first year allowance, from 1 April 2023 until 31 March 2026. This means that companies across the UK will be able to write off the full cost of qualifying main rate plant and machinery investment in the year of investment. Companies investing in special rate (including long life) assets will also benefit from a 50% first year allowance during this period. These new reliefs apply only to new equipment and exclude leasing. They also apply only to companies and not to individuals and partnerships. The Treasury says that moving to full expensing means the UK’s plant and machinery allowances will be joint first in the OECD in Net Present Value terms, instead of dropping to 33rd.

Professor Michael Devereux from the Oxford Centre for Business Taxation (see bit.ly/3ngPetn) estimates that the effect of this change will increase UK investment even more than the OBR allowed in its forecast (see page 63 at bit.ly/3TCdQsQ). Inevitably, though, not making the reliefs permanent loses some of the benefit – although the government said it hopes to continue with full expensing provided the public finances allow. The Labour opposition has also said it supports full expensing. See the chart below.

The government has also decided to improve its original plans for tax relief on research and developments costs. There will be a special relief of £27 for every £100 of R&D investment for loss-making small and medium sized companies engaged in intensive R&D sectors – costing about £500 million annually from 2025-26. This gives back some of the relief removed in the Autumn Budget – but does mean that we now have three R&D schemes instead of the previous two.

Finally, the audio-visual tax reliefs will be reformed into expenditure credits with a higher rate of relief than under the current system. The expenditure threshold for high-end TV will remain at £1 million per hour. The government will also extend the temporary higher rates of theatre, orchestra, and museums and galleries tax reliefs for two further years from April 2023 – although we may wonder why these are not grants.

Individuals and small business

The Spring Budget announces a consultation to expand the ‘cash basis’ – and a systematic review of HMRC guidance and key forms for small businesses, to help make the tax system easier for them to understand. The cash basis is currently used by about 1.2 million self-employed individuals and the consultation looks at removing some of the current restrictions. It focuses on four proposals, but welcomes other ideas:

- increasing the turnover thresholds for businesses to use the cash basis;

- setting the cash basis as the default, with an opt-out for accruals;

- increasing the £500 limit on interest deductions in the cash basis; and

- relaxing restrictions on using relief for losses made in the cash basis.

The current restrictions mean that about 200,000 businesses cannot currently use the cash basis.

The Budget also includes a discussion document on modernising HMRC’s income tax services so taxpayers can manage their own tax affairs online, reducing the need to contact HMRC. This includes the introduction of a Single Customer Account so taxpayers can interact with all their tax information in one place.

The adjusted time frame (and phasing) for Making Tax Digital for Income Tax brings a high cost, compared to numbers originally in the forecast. The changes are now expected to reduce the yield by at least £500 million annually from 2026-27, rising gently over time.

Pension saving

Reversing pension policy introduced over the last decade is an interesting move – and it carries a £1 billion annual cost. The government’s objective is to increase pension saving by wealthier taxpayers, remove the disincentive for some NHS consultants to work additionally and at the same time make additional funds available to invest in the economy. Removing the lifetime allowance charge from April 2023 and then abolishing the lifetime allowance completely is estimated to cost around £800 million annually. In 2020-21, about 9,000 individuals faced lifetime allowance charges amounting to some £400 million.

Increasing the annual allowance to £60,000 from April 2023 and allowing Pension Input Amount aggregation between open and closed public service pension schemes costs around £270 million annually. This is intended to allow members to offset any negative real growth for annual allowance purposes in legacy public service pension schemes against the annual allowance. In 2020-21, about 58,000 individuals faced annual charges, estimated at around £300 million.

Increasing the money purchase annual allowance (MPAA) to £10,000 from April 2023 is estimated to cost £35‑40 million annually. The original £4,000 limit was introduced in response to ‘round tripping’ – where funds were withdrawn from a pension only to be reinvested with a second burst of tax relief. The minimum tapered annual allowance will also be increased from £4,000 to £10,000, and the adjusted income threshold for the taper will be increased from £240,000 to £260,000.

The tax-free lump sum will now be limited to £268,275 – 25% of the previous lifetime allowance limit of £1,073,100 and frozen thereafter. This is likely to be the start of a long-term freeze of the tax-free amount.

Finally, lump sums currently taxed for some individuals at 55% above the lifetime allowance will be taxed at an individual’s marginal rate of income tax. These changes will take effect from 6 April 2023.

Pension scheme administrators will need to continue to operate lifetime allowance checks when paying benefits (for example, assessing whether an individual has available lifetime allowance) and to issue benefit crystallisation event statements (see bit.ly/3yXHorx).

Members who applied for before 15 March 2023 and hold a valid enhanced protection or any valid fixed protections will be able to accrue new pension benefits, join new arrangements or transfer without losing this protection. They will also keep their entitlement to a higher tax-free lump sum.

Fraud, tax avoidance and tax debt

The government will double the maximum sentences for the most egregious cases of tax fraud from seven to 14 years, and will consult shortly on the introduction of a new criminal offence for promoters of tax avoidance who fail to comply with a legal notice from HMRC to stop promoting a tax avoidance scheme.

The government is also investing a further £47.2 million to improve HMRC’s capability to collect tax debts, including supporting those who are temporarily unable to pay. This recognises that tax debt ballooned during the pandemic and significant effort will now be needed to recover as much as possible.

And finally… crypto cash gamble

Amusingly, it is thought that amending the Self Assessment tax forms will bring in £10 million annually from crypto-asset gains from 2025-26. The OBR classed this as ‘highly uncertain’; the surprise is why any number at all was put in.