Square pegs in round holes

Share this article

Kiret Singh discusses the scope of the new anti-hybrid rules contained in TIOPA 2010 Part 6A

Key Points

What is the issue?

From 1 January 2017, anti-avoidance rules targeting certain arrangements and transactions which give rise to hybrid mismatch outcomes need to be carefully considered in the context of international group structures and cross-border transactions.

What does it mean to me?

The rules can apply to all entities subject to UK corporation tax (including UK permanent establishments of foreign entities) directly or indirectly party to arrangements that give rise to hybrid mismatch outcomes. There are limited transitional rules under the new regime therefore existing transactions and structures, as well as new transactions and structures, are within the scope of the rules.

What can I take away?

The rules are extremely complex and broad in their application. Perhaps most significantly, there are no ‘safe-harbours’ or exemptions for small and medium sized entities.

Overview

In response to the Final Report on Action 2 of the OECD Base Erosion and Profit Shifting (BEPS) project, the UK introduced domestic anti-avoidance legislation on hybrid mismatches effective from 1 January 2017. These rules, the first to be introduced in response to OECD’s Final Report on Action 2, can be found in Part 6A of TIOPA 2010 (the ‘new rules’) and supersede the previous anti-avoidance rules on tax arbitrage contained in Part 6 of TIOPA 2010 (the ‘old rules’). This article expands on certain concepts in relation to the new rules and considers certain structures and transactions that may fall within the scope of those rules.

The legislation in Part 6A of TIOPA 2010 broadly follows and implements the OECD’s recommendations in their Final Report on Action 2 of BEPS (‘Neutralising the effects of hybrid mismatch arrangements’). However, it is worth noting that there are certain material departures in the rules from the recommendations in the OECD’s Final Report.

Hybrid mismatches

The legislation principally aims to neutralise hybrid mismatch outcomes by altering either the tax treatment of deductions or receipts, depending on the circumstances. The new rules apply to arrangements that give rise to a ‘deduction/non-inclusion’ (‘D/NI’) mismatch or a double deduction (‘DD’) mismatch and all forms of payments and ‘quasi-payments’ (i.e. the rules are not limited to simple payments and transfer). The rules are considerably broader than the now superseded anti-arbitrage rules that previously applied mainly to cross-border financing arrangements.

Consistent with the OECD’s recommendations, the new rules, which can also apply to domestic arrangements, are designed to work whether or not the relevant countries party to a cross-border arrangement or structure have introduced rules based on OECD’s recommendations on Action 2. Consequently, the rules have been drafted in a way that gives them ‘extra-territorial’ effect requiring taxpayers to consider both the UK tax treatment and foreign tax treatment of transactions and linked arrangements that give rise to hybrid mismatch outcomes in determining if a tax deduction in the UK should be disallowed or if income would need to be brought within the charge to tax.

It is worth noting that the old rules only applied if HMRC issued a notice directing a company to make or amend its self-assessment whereas the new rules, like targeted anti-avoidance rules more generally, need to be considered by taxpayers under self-assessment. It is also worth noting that, unlike the old rules, there is no ‘commercial purpose’ test (i.e. the rules are not limited to arrangements designed to secure a tax advantage).

The rules are also not restricted to arrangements involving related parties and can apply more widely to ‘structured arrangements’ (or certain ‘over-arching’ arrangements in the case of imported mismatches) which are broadly arrangements which, it is reasonable to suppose, have been designed to secure a mismatch outcome.

Outline of legislation

Part 6A of TIOPA 2010 contains 14 chapters. Chapters 1, 2 and 14 contain certain key definitions and terms, Chapters 3 to 10 target specific types of hybrid mismatches that apply to D/NI and DD cases involving, amongst others, mismatches on payments or quasi-payments in connection with financial instruments, payments or quasi-payments on repos, stock lending arrangements and other hybrid transfers (this is likely to be more relevant to certain financial institutions and traders), payments or quasi-payments in relation to hybrid entities, certain internal transfers of money or money’s worth made or treated as made in relation to companies with permanent establishments, and certain mismatches concerning dual-resident companies. Chapter 11 counteracts ‘imported mismatches’.

The imported mismatch rules most notably apply even when a UK entity is not directly involved in a hybrid mismatch arrangement but where such an arrangement exists elsewhere in the same over-arching ‘arrangement’. Chapter 12 contains provisions to amend adjustments made to counteract mismatches where new information becomes available and Chapter 13 contains, as is now common in all new UK legislation introduced, targeted anti-avoidance provisions.

The legislation contained in Chapters 3 to 10 outlined above set out the conditions that would need to be satisfied for there to be a hybrid mismatch caught within the rules and the adjustments which would need to be made for corporation tax purposes to neutralise the mismatch. Consistent with the OECD’s recommendation, the legislation proposes a ‘primary’ defence and a ‘secondary’ defence to ensure the hybrid mismatch outcome is neutralised.

Certain examples

The following examples consider the application of the new rules in Chapter 3 (the hybrid instruments rule) cases and a Chapter 5 (disregarded hybrid payer rule) case. These examples are not exhaustive and do not consider the scope of the rules in their entirety and only provide an overview of the application of the new rules in certain structures and arrangements. HMRC guidance in relation to the application of Part 6A of TIOPA 2010 is still in draft and further changes to the legislation are anticipated. The examples below only serve as a high-level guide on the application of the rules.

Hybrid instrument

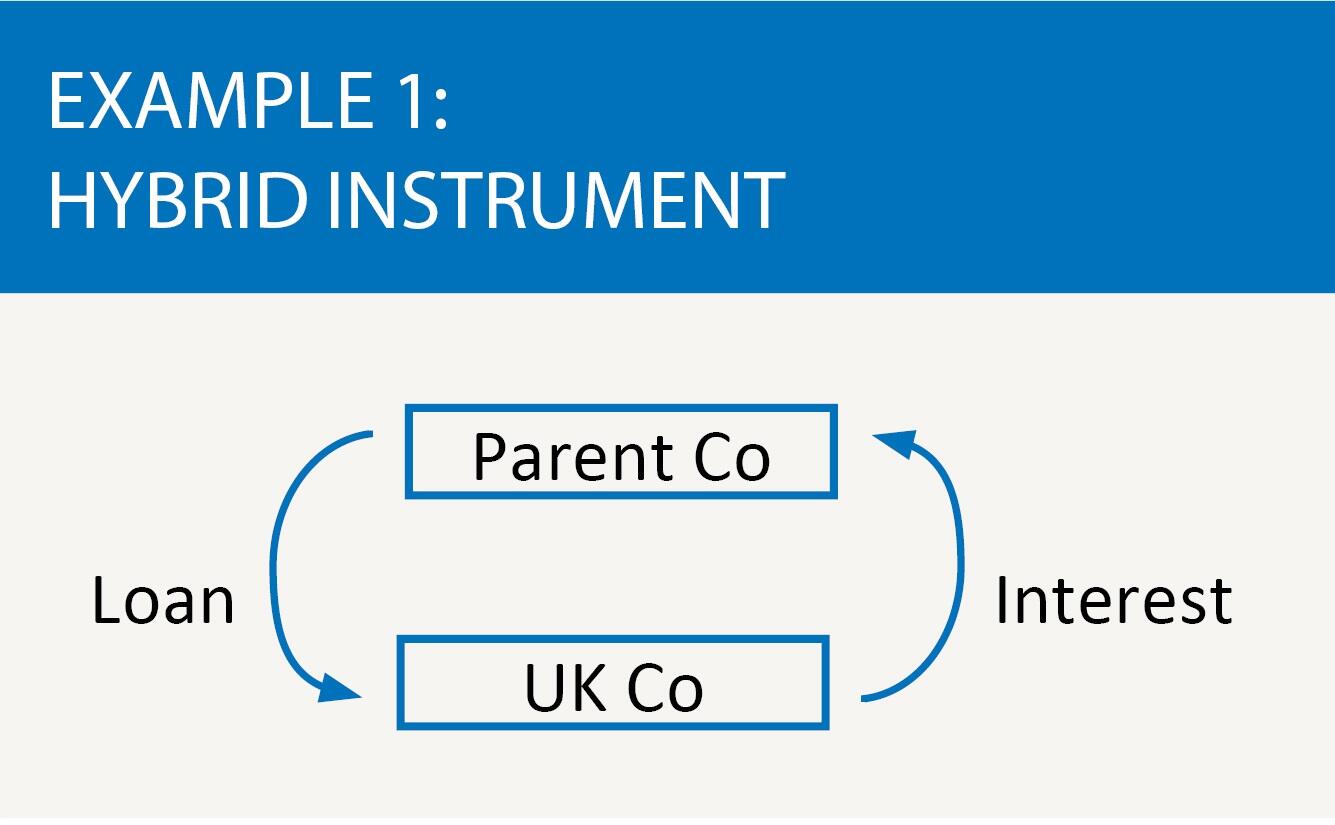

In example 1, let us assume that UK Co, a company incorporated in England and Wales and corporation tax resident in the UK only, is a wholly owned subsidiary of Parent Co which is incorporated and tax resident in Country X. ParentCo has provided UK Co with a shareholder loan which, let us assume, gives rise to tax deductible interest expenses in the UK and which is treated as a distribution and is exempt from tax under Country X’s participation exemption as Country X consider the shareholder loan to have the characteristics of equity.

The above structure would fall within the remit of Chapter 3 of Part 6A of TIOPA 2010 which counteract mismatches arising in respect of hybrid instruments as the shareholder loan in the above example would be considered to be a hybrid instrument. There are four conditions to be met before Chapter 3 can apply to the example above. If all four conditions are met, the mismatch above would be countered by denying a deduction claimed by UK Co.

There are a number of exceptions to the basic rule above and a detailed consideration of these would be outside the scope of this article. One key exception from a UK tax perspective is the treatment of certain regulatory capital securities for the purposes of the Taxation of Regulatory Capital Securities Regulations 2013 SI 2013/2029 issued for bona fide reasons to shore up regulatory capital which are not considered to be ‘financial instruments’ for the purposes of the rules.

Nil tax jurisdictions

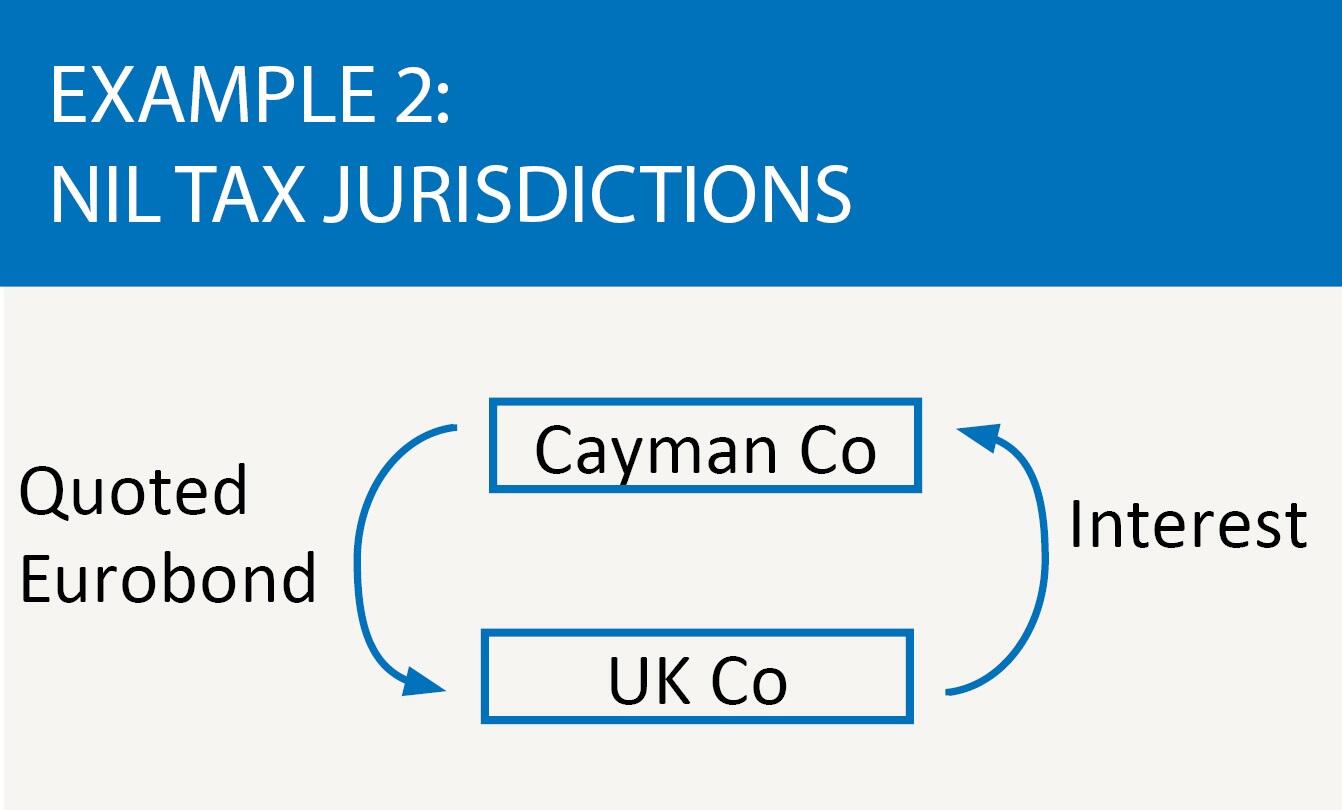

An extension to the example would be a situation where a company in a nil tax jurisdiction, such as Cayman Co, which is a company incorporated in and tax resident only in the Cayman Islands, subscribes for loan notes in UK Co on arm’s length terms which are listed on a recognised stock exchange, as shown in example 2. Notwithstanding the UK anti-avoidance rules which apply in relation to interest deductions more generally, assuming the interest expense in the case above would give rise to a tax deduction in the UK, as the corresponding income would not be subject to tax in the Cayman, there would prima facie be a D/NI case. The OECD’s Final Report states that such cases should not fall within the remit of the hybrid financial instruments rule (i.e. as implemented in Chapter 3 of Part 6 of TIOPA 2010). However, there is some uncertainty based on HMRC’s guidance whether the same would be true from a UK tax perspective).

The recommendations of the OECD and the HMRC guidance on the new rules are, however, consistent in their application in cases where a foreign creditor in a loan relationship with a UK debtor is subject to a territorial tax regime and is not subject to taxation on income with a foreign situs. Therefore, in the above example, if Cayman Co were to be a company incorporated and tax resident in Hong Kong, for example, there should be no mismatch caught by the rules on hybrid financial instruments.

US Check the Box election

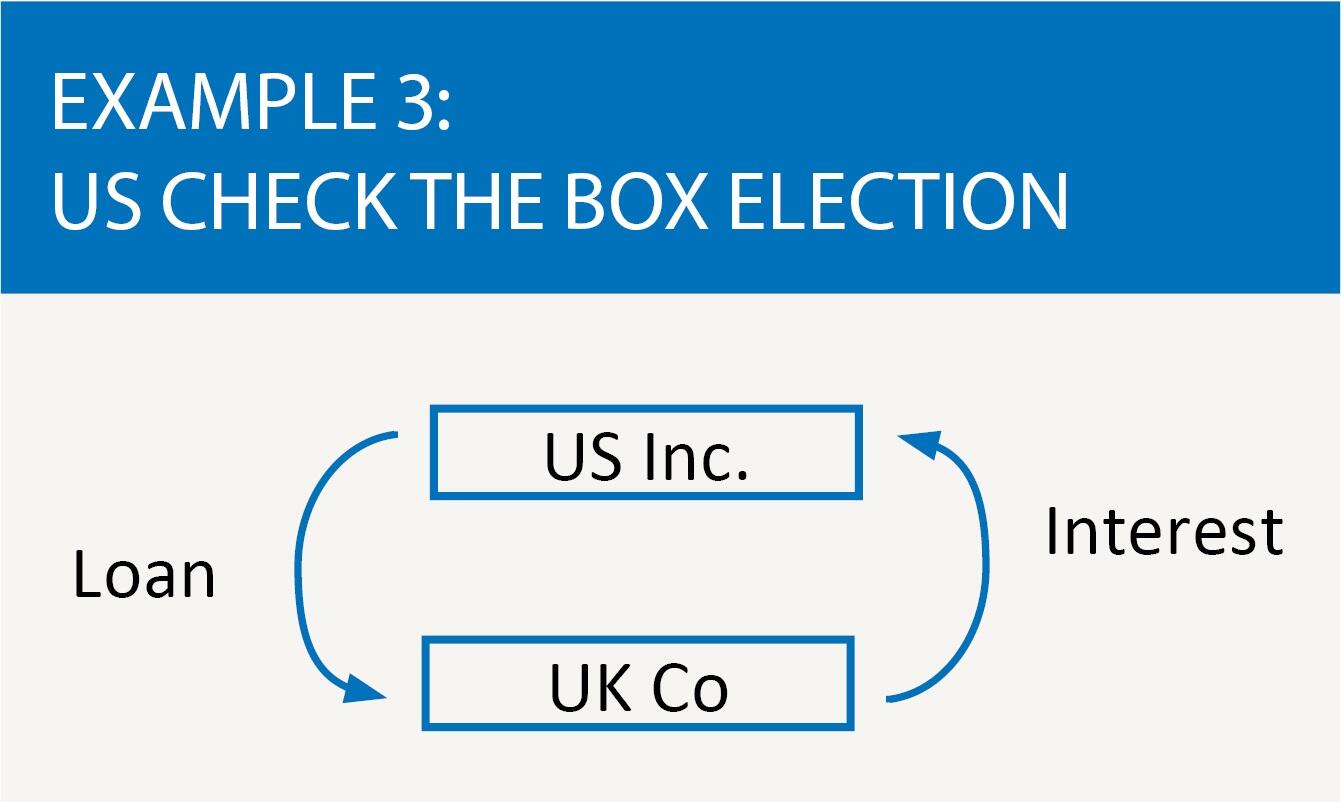

In example 3, let us assume that a US parent company provides a loan to its wholly owned UK subsidiary at interest (let us assume that the loan is a plain, vanilla debt) and the interest expense, again, notwithstanding other anti-avoidance rules and the new anti-hybrid rules, would be deductible from a UK corporation tax perspective. Let us also assume that UK Co has been treated as a ‘disregarded’ entity for US federal tax purposes through the making of an entity classification election (also commonly referred to as a ‘check-the-box’ election). As such, UK Co for UK tax purposes would be considered to be a separate tax person whereas UKCo would broadly be considered to be the same entity as US Inc for US federal tax purposes with the result being that interest income from UK Co would not be subject to US federal income tax giving rise to a D/NI outcome.

In example 3, UK Co would be considered to be a ‘hybrid entity’ and specifically a ‘hybrid payer’ and the conditions within Chapter 5 of Part 6A of TIOPA 2010 would need to be considered. There are five conditions which would need to be satisfied before Chapter 6 applies. Most financing structures that have sought to take advantage of the arbitrage above are very likely to be caught by Chapter 5 of Part 6A of TIOPA 2010 and advisers would need to consider the impact of deductions in the UK being denied or restricted.

The above examples consider, at a high-level, the application of the rules based on existing legislation and HMRC guidance. HMRC’s guidance (all 390 pages) provide a number of examples of the scope of the new rules and it is not possible, within the confines of this article, to consider the application of the rules in the remaining chapters within the legislation. There are also certain notable departures and variations from the recommendations and the examples contained in OECD’s Final Report on Action 2 (most notably the treatment of debits and credits on the release of a connected company loan otherwise than on a distressed basis).

Investment funds

It is also worth noting that the rules will need to be carefully considered by investment funds and their managers. Special exemptions apply to certain ‘relevant investment funds’ (broadly UK OEICs, authorised unit trusts and ‘offshore funds’ meeting the genuine diversity of ownership condition), however, other private funds, including debt funds and private equity funds, may be considered to be hybrid or reverse hybrid entities (for example, an English limited partnership which is considered to be tax transparent in the UK but may be considered to be a separate person in other jurisdictions) and could fall within the scope of the rules or could have dealings with underlying UK investee companies where payments and/or distributions made by those companies could fall within the scope of the rules (either on account of the entities being related parties or members of a control group or there being ‘structured’ arrangements).

Similar considerations are likely to apply in relation to securitisation companies in structured finance transactions which often issue asset-backed instruments and/or loans that could be treated as ‘hybrid’ instruments (such as profit participation notes issued by a company tax resident in Ireland falling within the meaning of Section 110 of the Irish Taxes Consolidation Act 1997). Even where investors in such entities and the entities themselves do not have any link with the UK, dealings between the those entities with UK counterparties in relation to debt instruments, for example, could be caught under the new rules (e.g. in in relation to the rules in Chapter 11 on imported mismatches).

Next steps

Companies should review their business structures as soon as possible to establish if they may potentially be caught and determine whether any rectification or remedial measures may be put in place to mitigate the application of the rules.