Myths demystified

Share this article

Kiret Singh looks at the real issues faced when dealing with demergers

Key Points

What is the issue?

The concept of a demerger is simple. As businesses grow there may come a time where there is a need for business divisions to be restructured or streamlined.

What does it mean to me?

Demergers are still one of the most complicated areas of taxation and transaction structuring.

What can I take away?

Demergers require intimate tax knowledge and awareness of the Taxes Acts, sometimes covering all the main headings of taxation ranging from VAT through to Inheritance Tax.

Tax advisers have become increasingly familiar with statutory and non-statutory demerger types, the conditions which would need to be satisfied in order to exempt a distribution or to prevent a charge to income tax on a distribution from arising, securing capital gains tax and stamp tax neutrality and mitigating VAT costs on supplies made in the course of a demerger transaction.

However, the fact remains that demergers are still one of the most complicated areas of taxation and transaction structuring. Demergers require intimate tax knowledge and awareness of the Taxes Acts, sometimes covering all the main headings of taxation ranging from VAT through to Inheritance Tax. This article seeks to cover the common ‘myths’ associated with structuring a demerger transaction and addresses some of the author’s views on best practice.

What is a demerger?

The concept of a demerger is simple. As businesses grow there may come a time where there is a need for business divisions to be restructured and streamlined, where they may need to be carved-up and allocated to different shareholders with separate ownership structures, or, simply, where certain profit centres and divisions may need to be carved-out in anticipation of a sale (perhaps where they may no longer be considered to be the right ‘fit’ or where a suitable buyer is found that is best placed to take that business unit forward).

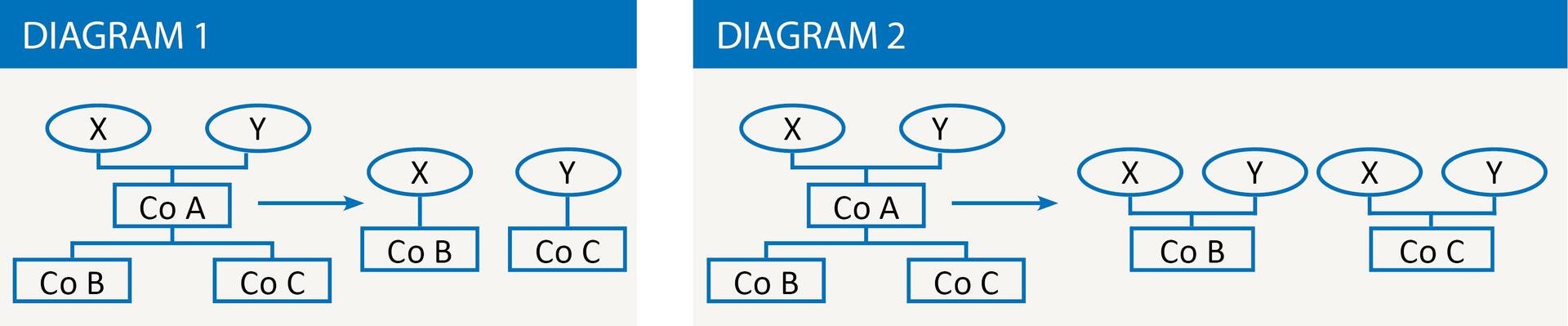

In tax terms, a ‘demerger’ can have a very broad meaning. It is most commonly associated with the split or partition of a company’s shareholding matched by a distribution of assets to different shareholder groupings. For this reason, demergers are often categorised into ‘partition’ demergers (see diagram 1) or ‘split’ demergers (see diagram 2).

Indeed, a ‘demerger’ could well be a split or partition of a partnership, a mixed partnership, or, in the context of investment funds and collective investment schemes, authorised unit trusts and Investment Trust Companies, for example. Although this article focuses on the demergers in the context of companies, the same underlying principles apply irrespective of the structure in question.

What are the main tax considerations?

The key to structuring a demerger from a tax perspective is securing tax neutrality. In other words, apart from professional fees and other associated costs, the aim should be to prevent, as far as possible, any transaction taxes or other tax charges crystallising on the transfer of shares and assets.

To this end, one of the most important angles to a corporate demerger is preventing, principally where there are UK-resident shareholders, a charge to income tax on a distribution (in accordance with the definition of a ‘distribution’ in Part 23 of CTA 2010). The tax consequences here can be material and significant if a charge to income tax cannot be avoided (as it stands, a charge of up to 38.1% can arise on the value of the assets to be demerged or otherwise carved-out). This is why a lot of emphasis is placed on so-called ‘statutory’ demergers which exempt this charge to income tax where various conditions are met (also set out in Part 23 of CTA 2010). Non-statutory demergers, on the other hand, seek to simulate the same outcome through other means that seek to ‘switch-off’ income tax rules and force capital gains tax treatment (e.g. through putting a company into members voluntary liquidation or by rebasing to create new consideration through a capital reduction).

Employment-related securities is often an after-thought when structuring a demerger. Once again, the tax consequences of overlooking certain key employment-tax considerations can be very costly, as this could give rise to income tax charges of up to 45% on any value or benefit derived by or conferred on employees, broadly. The overall tax cost could be higher if the shares in question are ‘readily convertible assets’ (a detailed discussion of what is and isn’t a ‘readily convertible asset’ in this context is outside the scope of this article).

Capital gains tax considerations are equally important. At stake, the distributing or transferor company could be subject to corporate tax on chargeable gains at rates of up to 19% presently (and ignoring other reliefs such as indexation allowances and/or the substantial shareholdings exemption, both of which have been subject to change in rules introduced last year) and up to 20% for the individual shareholders that are subject to the demerger transaction.

Finally, stamp tax (or stamp duty reserve tax, as may be the case) and Stamp Duty Land Tax (or the Scottish equivalent, LBTT, as may be relevant) will also require consideration (including its application to investment funds or unit trusts (under principles established in Save & Prosper Securities Limited). The general rule of thumb is that stamp taxes are unavoidable in corporate ‘partition’ demergers (as existing reliefs do not cater for these), however, every effort would be required to prevent stamp liabilities for ‘split’ demergers where there is, in substance, no change of ownership.

Preventing any unexpected surprises or liabilities

The following points set out certain considerations typically encountered in the course of a demerger and what can be done to mitigate risks arising in the course of advising clients on such transactions.

Importance of HMRC clearance

HMRC clearance letters are very important and obtaining relevant clearances is a fundamental workstream in a demerger transaction. Clearances can cover a number of provisions in the Taxes Acts which specifically provide for a clearance mechanism (e.g. clearance to confirm exempt distribution treatment under Part 23 of CTA 2010, clearances for reconstruction provisions within Part 8 of CTA 2009, scheme of reconstruction reliefs in TCGA 1992 and so on, so called ‘statutory’ clearances), clearances on certain areas of doubt on the application of tax law and where there is little or no guidance provided by HMRC (or ‘non-statutory clearances’) and specific stamp tax adjudications required from HMRC (e.g. under section 75 or section 77 of Finance Act 1986).

Whilst clearances are fundamentally key in structuring transactions, it is the author’s view that various workstreams should precede the making of a clearance application to HMRC and following the agreement of terms (with the appropriate addressees that will be placing reliance on the advice given) such as i) conducting a planning meeting, ii) drawing up a proforma balance sheet, iii) carrying out due-diligence on any precedent transactions or reconstructions and iv) preparing either an options paper, a tax report or memorandum, (or both), exploring the options available to meet set objectives and providing a recommendation as to the most suitable way forward.

This is extremely important not just in ensuring the client is fully educated and appraised of the proposed structure of the transaction, but also to manage risk, ensuring all material tax considerations have been sufficiently rehearsed, identifying any potential risk areas and ensuring all parties to the transaction (e.g. the directors, shareholders, lawyers, advisers, etc.) are aware of the key deliverables and timelines.

Scope of HMRC clearance

Statutory and non-statutory clearances provided by HMRC are typically qualified (sometimes quite heavily) such that HMRC keep to scope and reserve their right to revisit the transactions or arrangements in question. Specifically, for most statutory clearance applications (e.g. share exchange reliefs, scheme of reconstruction reliefs, transactions in securities clearances), HMRC only provide clearance confirming that they do not consider the transactions or arrangements in question to have a tax avoidance purpose. For example, in the context of clearances under section 139(5) of TCGA 1992, HMRC do not confirm whether all the requisite conditions of that section have been met (and thus no tax charge should arise on the distributing or transferring company in a demerger). Their clearance only extends to the bona fides of the transactions and/or arrangements in question and, this, too, is based on the information provided by the taxpayer and/or their advisers in the clearance applications (working on the assumption that every material detail or consideration has been disclosed to HMRC in the clearance application).

HMRC are known to challenge the validity of a statutory clearance application where it is not clear whether the transactions or arrangements in question fall squarely within the remit of the relief or exemption sought (which provides for the statutory clearance mechanism), however, this should not be construed as HMRC agreeing that the the relevant relief or exemption is in point. The one exception to this is where HMRC’s clearance, by virtue of the statutory provision that provides for the making of a clearance, extends to simply confirming whether or not they consider the transactions or arrangements to have an avoidance purpose and confirms whether the requisite conditions for relief or exemption have been met (e.g. in the case of section 1092 of CTA 2010 providing advance confirmation that a distribution would be exempt).

For the reasons above, HMRC clearances, whilst critical, are not themselves conclusive on the tax analysis underpinning a demerger transaction. The principal obligation remains with the tax adviser or tax lawyer to ensure that their opinions are robust and complete (including the underlying analysis supporting conclusions reached).

Accounting matters

Determining the accounting treatment of a demerger transaction is pivotal in ensuring no unexpected tax consequences arise as a result of the transactions proposed. This can range from establishing the correct treatment of asset transfers and acquisitions, ensuring appropriate disclosure is made in the financial statements of the entities involved in the transaction, identifying all debit and credit items which may impact the statement of comprehsive income of the relevant companies, and identifying any transactions which could be unlawful or illegal from a corporate law perspective.

These considerations are best tackled by including the auditors or the internal finance team (or their advisers) of the companies subject to the demerger in the project or deal team and reviewing the balance sheet and the tax computations of the relevant companies subject to the transaction at the beginning. Special care should be given to transitional adjustments, any items brought forward in the tax computations which may be released or brought within the charge to tax as a result of the demerger transaction, and the management of deferred tax assets and liabilities, to name a few material considerations. Drawing up proforma balance sheets for all relevant entities within scope pre-transaction and illustrating each step to implement the proposed transaction can help prevent unexpected outcomes.

Drafting legal documentation

Linked to the first point above on planning a transaction is ensuring that an appropriate team is identified and mobilised for the purposes of implementing a demerger. Although tax forms a key part in the various workstreams, associated with implementing a demerger, it is the author’s view that the drafting of all legal documentation should strictly be carried out by qualified solicitors.

For this reason, whilst it may be acceptable, subject to appropriate skill, experience and resource available, for tax advisers to consider drafting minutes and resolutions, often, in a demerger transaction, there are various other documents required which require drafting (e.g. asset purchase agreements, novation or assignment deeds, etc.) which should be drafted by lawyers. Indeed where there are property transfers and where property conveyancing is required, this should be handled by suitably experienced and qualified lawyers. This involves additional cost and, for this reason, where tax advisers are putting forward demerger proposals in front of their clients, all expected costs involved should be made clear to the client from the beginning.

Employment tax risks

As noted above, the impact of a demerger on share awards held by employees, including options and long-term incentive plans, is often an area that is overlooked when considering the impact of a demerger transaction.

The terms of any share awards will need to be reviewed to determine whether they specify what happens to the award on a demerger. However, the terms may not expressly deal with a demerger and in those circumstances it will be necessary to consider how the demerger is being structured and whether the employee is part of the demerged business and whether any other provisions of the award will apply. For example, will the employee become a leaver because they are part of the demerged business and/or is a new holding company being introduced?

Where employees already hold shares, they will be able to participate in the demerger with other shareholders, although the impact of the demerger on any performance conditions or hurdles applying to the shares will need to be considered. In addition to the tax consideration of non-employee shareholders, it will also be necessary to consider whether any income tax liabilities may arise under Part 7 ITEPA 2003, for example where the shares are restricted securities.

Where employees do not currently hold shares, for example options of LTIP awards, a key impact of the demerger is that those awards can lose value unless action is taken. Where shareholders receive distributions as part of the demerger, the shares will reduce in value and employees holding awards over shares will now hold awards over shares which have reduced in value whilst not being entitled to the distribution as they are not shareholders. In some cases it may be possible to rely on variation of share capital provisions in the terms of the awards but this may not always be possible, particularly for tax advantaged awards.

For these reasons, the impact of the demerger on share awards should be considered early in the process to determine the impact on employee share awards.

Stamp adjudications

Stamp adjudication applications should not be an after-thought and should be submitted on a timely basis. Preparing an application for stamp tax adjudication can take a significant amount of time and effort and should be given sufficient attention from the beginning.

One key area which must be given detailed consideration is the application of section 77 of Finance Act 1986 (which is relevant where there is an insertion of a New HoldCo in a group structure as part of a demerger; typically required in a ‘section 110’ liquidations demerger where there is no desire to liquidate an existing trading company or in a capital reductions demerger to create ‘new consideration’). This relief, also referred to as ‘new holding company’ relief, is far more restrictive than it is often perceived to be and HMRC are known to reject applications to claim this relief even in trivial circumstances (e.g. where ‘subscriber’ shares issued on incorporation have not been reflected in consideration shares issued to provide for ‘mirroring’ shareholdings pre and post insertion of a New HoldCo). HMRC also take a very literal view on what constitutes ‘shares’ and ‘share capital’ and say in their manuals that the conditions of section 77 are ‘stringent and [will be] strictly enforced’.

Equal care and attention would be required to ensure that there are no ‘disqualifying arrangements’ which could block a claim under section 77 of Finance Act 1986 and that the share exchange is not being done as part of arrangements to effect a subsequent change of ‘control’ (under the recently introduced anti-avoidance rules contained in section 77A of Finance Act 1986, which, although aimed at pre-takeover arrangements involving a foreign New HoldCo, can also inadvertently apply to demerger transactions).

Section 75 of Finance Act 1986 can be equally important (depending on the structure of the transaction and the form of the demerger) and should be given the same level of weight and attention.

Transferring businesses

Schedule 5AA of TCGA 1992 setting out the requisite conditions which would need to be met to qualify as a ‘scheme of reconstruction’ is a critical part of the Taxes Acts when considering a demerger transaction. One of the conditions (the continuity of business requirement; paragraph 4 of Schedule 5AA) is that the ‘effect of the restructuring is that…the business or substantially the whole of the business carried on’ by the original company or original companies must be carried on by a successor company or two or more successor companies.

The meaning of ‘business’ for these purposes specifically includes the holding of shares in a controlled subsidiary (see para 4(3)). However, one would have to refer to case law to establish what constitutes a ‘business’ more widely. Once again, this is an area that deserves more attention and care in a demerger transaction. Particular care is required where transfers in the course of a demerger are made in relation to assets which do not themselves constitute a ‘business’ (e.g. high-value ‘stand-alone’ assets and intellectual property, investments that are not internally or externally managed, etc.).

Linked to this is whether the conditions for Transfer of a Going Concern (TOGC) treatment for VAT purposes applies to the proposed steps in the transaction structure or whether there are any supplies made which could attract VAT (potentially irrecoverable, depending on the VAT recovery status of the relevant entities involved).

House-keeping and elections

Finally, it is important to complete transactions with a ‘bible’ of documents that include the making of all relevant elections (e.g. section 431, ITEPA 2003 elections, etc.), submissions of all relevant notifications and forms to HMRC and the compilation of final signed opinions, clearance letters and other material documentation.

For statutory ‘exempt’ demergers, a return must be made to HMRC within 30 days of making an exempt distribution (again, an often overlooked requirement). The return must be made to an officer of HMRC giving details of the distribution and the reason why it is exempt. This return must be made even if HMRC have provided confirmation that a distribution is exempt. Still on statutory demergers, care would also be required to ensure that clients understand how a ‘chargeable payment’ might arise and in ensuring that this can be avoided, as far as possible (for as long as five years from the date of the exempt distribution).

What has changed?

Tax advisers will be familiar with the re-write of the degrouping charge rules in Finance Act 2011 and how this has impacted demerger transactions (indeed, there are a number of de-grouping related pitfalls that can be considered in the context of a demerger transaction covering de-grouping on shares and other assets, intangible assets under the TCGA 1992 and the Part 8, CTA 2009 regimes and SDLT de-grouping charges which warrants an article in its own right). Some will also be aware of the ongoing consultation concerning reforms to the de-grouping rules for Pt 8 intangibles.

The re-write of the SSE rules introduced in FA 2017 will also have a significant impact on demergers and will increase the popularity of ‘direct’ statutory demergers.