Stacking the odds

Share this article

Paul Sutton examines how corporate governance flaws exacerbate transfer pricing risks

Key Points

What is the issue?

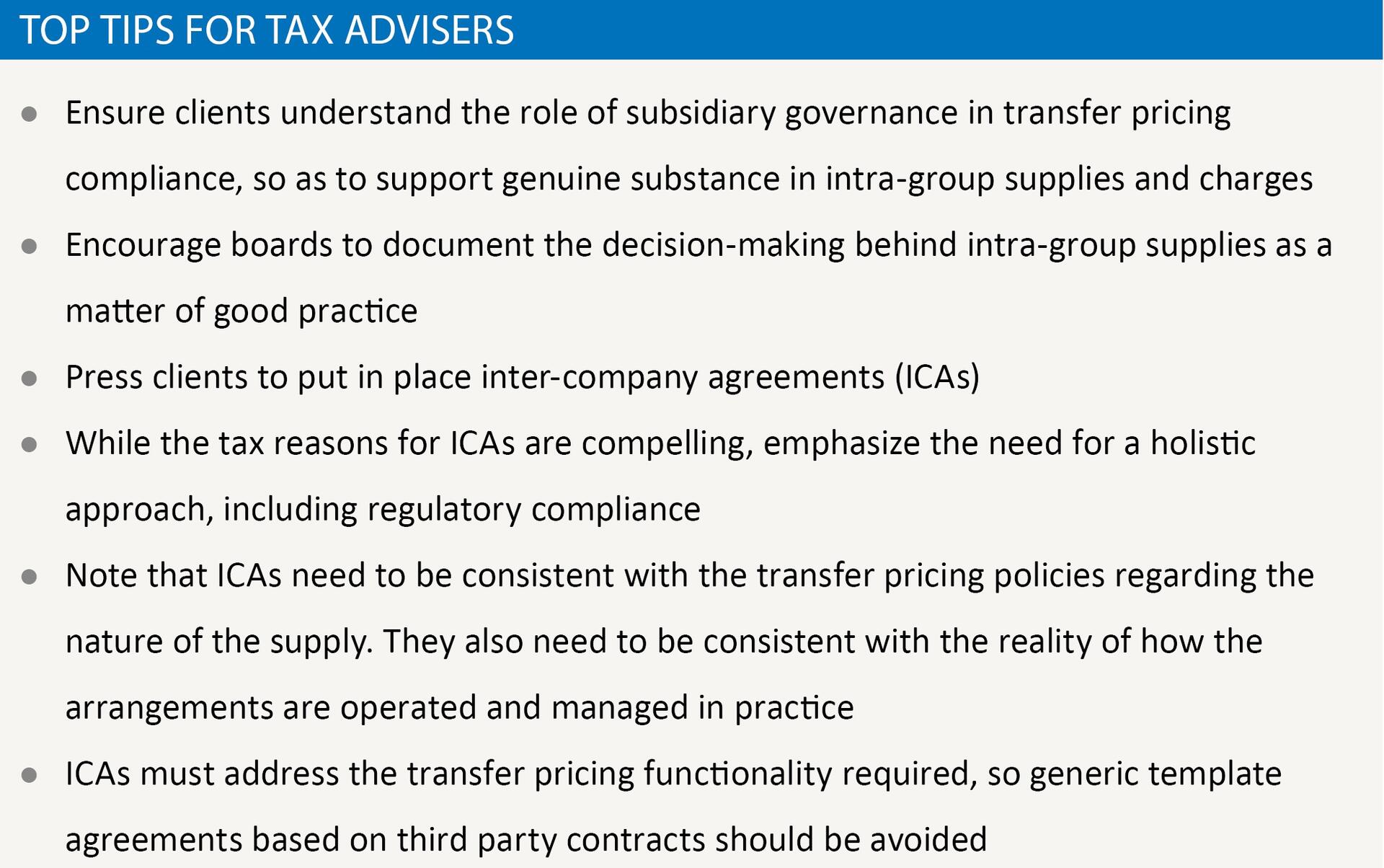

From a legal perspective, a multinational group is a collection of legal entities, each controlled by its own board or governing body. The decisions that subsidiary boards make, and how they are arrived at, are still largely opaque.

What does it mean to me?

Part of the problem is that board meetings usually just record the outcome of decisions, rather than the discussions and deliberations behind those decisions. This has ramifications for transfer pricing compliance, which looks at how individual group entities exercise actual control over risks.

What can I take away?

With proper planning, and the appropriate processes in place, it should be possible to produce contemporaneous documentation that produces clear audit trails that evidence how decisions are made regarding intra-group supplies. These processes, when supported by legally robust ICAs, provide the best possible protection against challenges to transfer pricing arrangements.

How well-run boards make decisions has changed dramatically over the last decade. High profile corporate collapses, such as Enron and WorldCom, instigated a widespread review of best corporate governance practice, resulting in many boards adopting reforms to promote greater transparency. Multinational enterprises now routinely disclose directors’ salaries and committee members on their websites, and many boards go much further.

Visible structural changes such as these, necessary though they were, did not go to the heart of how boards make decisions and how corporate groups function. From a legal perspective, a multinational group is a collection of legal entities, each controlled by its own board or governing body. The decisions that subsidiary boards make, and how they are arrived at, are still largely opaque. This is particularly true of the deliberations which underpin those decisions, which are seldom, if ever, recorded in detail. Part of the problem is that board meetings usually just record the outcome of decisions, rather than the discussions and deliberations behind those decisions. This has ramifications for transfer pricing compliance, which looks at how individual group entities exercise actual control over risks. It means that conventional governance processes are unlikely to provide much protection if decisions are later questioned by tax authorities. From the point of view of international tax authorities, the discussions which gives rise to decisions about intra-group supplies are critical in determining whether those supplies are compliant from a transfer pricing perspective.

The risks are considerable and growing. From 2011/12 to 2016/17, HMRC secured £5.9 billion of additional tax by challenging the transfer pricing arrangements of multinationals. Intra-group supplies are of course subject to challenge by every tax authority in which businesses operate, so HMRC’s increased activity in this area is just the tip of the iceberg. Imminent tax reform in the U.S., which will reduce corporation tax rates from 35% to 21% will likely mean that U.S. corporates face more scrutiny of their transfer pricing policies from foreign tax authorities. This is because the payment of intercompany charges and royalties to the U.S. will look more like ‘tax planning’. To complicate matters, the level of detail required in documenting transfers varies considerably, so that what is adequate in one jurisdiction may not provide adequate protection in another. The Russian tax authority, for example, is particularly rigorous in insisting that arrangements are supported by copious documentation of the kind unlikely to be supported by the corporate governance processes of many boards.

External tax advisers are usually at a significant disadvantage in this respect in that their influence over clients is often limited, particularly when it comes to boardroom processes. As the need to evidence the decision making behind intra-group supplies becomes more pressing, tax advisers have a growing responsibility to ensure that boards document decisions in sufficient detail. Convincing boards to spend more time on an activity whose value may never be apparent is not always an easy task (if a transfer pricing challenge is averted due to in-depth documenting of decisions, the cost of that challenge, had it succeeded, cannot be quantified). Nevertheless, as tax authorities step up their scrutiny of transfer pricing arrangements the logic of investing more resources in prevention becomes more compelling.

The growing need for businesses to be able to evidence contemporaneous documentation (e.g. dated board minutes) of transfer pricing arrangements, including the deliberations that gave rise to those decisions, while necessary, is not a sufficient condition for transfer pricing compliance. Tax advisers should also press boards to have inter-company agreements (ICAs) in place. ICAs can be seem as the legal manifestation of those board deliberations on intra-group supplies.

ICAs are legal agreements between related parties. They define the legal terms on which services, products and financial support are provided within a group. ICAs can cover a wide range of issues, including head and back office services, revenue and cost sharing, intellectual property licences, and so on.

It has long been accepted that ICAs are a fundamental part of transfer pricing compliance and with the implementation of the OECD’s BEPS guidance by an increasing number of countries each year, this importance is only increasing for multinational enterprises and financial institutions. The OECD had this to say on the matter in 2010: ‘Contractual arrangements are the starting point for determining which party to a transaction bears the risk associated with it. Accordingly, it would be a good practice for associated enterprises to document in writing their decisions to allocate or transfer significant risks before the transactions with respect to which the risks to be borne or transferred occur…’

Previously, external advisers have often struggled to convince boards of the necessity of ICAs. Businesses frequently took the view that the relationship between corporate entities in a group is unlikely to come under scrutiny and so neglected to invest in clear, legally robust ICAs. Now, the landscape is very different. The question is no longer whether a group should implement intercompany agreements, but how they should manage the process of creating and maintaining those agreements. Failing to ensure that legally binding intercompany agreements are in place is akin to giving tax authorities access to the group’s bank accounts so they can withdraw what they consider fair.

While the tax reasons for properly drafted ICAs are compelling enough, there are important non-tax drivers, too. ICAs can be an important tool for regulatory compliance (where one or more members of the group are regulated entities, for example in the financial services and insurance sectors); ring-fencing assets and liabilities from risk; improving the corporate governance of companies throughout the group; reducing personal liability risks for directors; supporting the external and internal audit of group entities and ensuring that intellectual property rights can be enforced and monetised appropriately.

The consequences of not having ICAs can be serious. Fundamentally, groups which do not have appropriate, signed ICAs in place are on the back foot in discussions with local tax authorities about their transfer pricing compliance. This is because they are unable to present a clear statement as to what intra-group supplies are being made (and for what price), how relevant assets are held, and how risks are allocated between group companies. In certain jurisdictions, corporates are routinely subject to fines and penalties, simply for failing to produce signed ICAs when requested. Other problems include expenses potentially being disallowed, post year-end ‘true up’ type adjustments being subject to challenge and local tax authorities attempting to re-characterise a transaction as something other than that claimed by the taxpayer.

It is important to achieve the governance and transfer pricing benefits of having robust legal documentation for intra group supplies. In relation to any given intra group supply, the relevant ICAs obviously need to be consistent with the group’s transfer pricing policies regarding the nature of the supply, the terms of supply (including the allocation of risk) and the pricing of the supply. They also need to be consistent with the reality of how the arrangements are operated and managed in practice. Complicated change control or reporting provisions which have been imported from an arms’ length commercial contract will do nothing to enhance a group’s transfer pricing position if they are not followed in practice.

The terms of the ICAs must be consistent with the legal and beneficial ownership of any relevant assets and the commercial reality of intra group transactions. For example, an intra-group agreement where a company purports to grant a license over intellectual property which it does not actually own, could create confusion and misleading accounting entries, rather than promoting the group’s transfer pricing and other commercial objectives.

The legal agreements should reflect an arrangement which the directors of each participating company can properly approve as promoting the interests of that particular company. This means that some proposed arrangements can be problematic – such as arrangements which would involve a particular entity incurring ongoing losses; being exposed to liabilities or cashflow demands which it does not have the financial resources to meet (such as indemnities for product liability, or an obligation to repay loans on demand); or ‘giving away’ assets or value, especially if it is to a parent undertaking.

Finally, the ICAs must be capable of being legally binding, which means that the key terms of the arrangement must have ‘legal certainty’. This principally applies to the description of what is being supplied and the price of the supply, so that those provisions must be objectively ascertainable from the terms of the agreement. We see a lot of agreements where there is no price stated or the price is set by some vague reference to comparable turnover or net profits of the subsidiary. This approach can raise issues from the point of view of legal certainty and from a transfer pricing compliance perspective. Other common mistakes include agreements being too complicated; not matching ownership and flow of IP; not adequately reflecting group structures; failing to guard against inappropriate termination provisions; and overlooking the importance of making provisions for allocation of cost between multiple service recipients.

With proper planning, and the appropriate processes in place, it should be possible to produce contemporaneous documentation that produces clear audit trails that evidence how decisions are made regarding intra-group supplies. These processes, when supported by legally robust ICAs, provide the best possible protection against challenges to transfer pricing arrangements.