A stop to looping

Share this article

Satvi Vepa considers the rules introduced to counter VAT offshore looping

Key Points

What is the issue?

Following the case of Hastings Insurance Services Limited v HMRC [2018] UKFTT 27 (TC) (see below), the Government announced in July last year that secondary legislation would be introduced to tackle VAT avoidance relating to a particular off-shore looping arrangement used almost exclusively in the insurance sector.

What does it mean to me?

The VAT (Input Tax) (Specified Supplies) (Amendment) Order 2018 (the ‘Amendment Order’) was drafted for this purpose came into effect for supplies made on or after 1st March 2019.

What can I take away?

Insurance intermediaries that provide intermediary services to non-EU insurance companies in respect of insurance ultimately provided to a UK customer base will no longer be able to recover input VAT attributable to their supply of services to the non-EU insurance company.

Following the case of Hastings Insurance Services Limited v HMRC [2018] UKFTT 27 (TC) (see below), the Government announced in July last year that secondary legislation would be introduced to tackle VAT avoidance relating to a particular off-shore looping arrangement used almost exclusively in the insurance sector. The VAT (Input Tax) (Specified Supplies) (Amendment) Order 2018 (the ‘Amendment Order’) was drafted for this purpose. It was laid before Parliament on 11 December 2018 and came into effect for supplies made on or after 1 March 2019.

Legal background

UK VAT is chargeable on any supply of goods or services made in the UK where the supply is a taxable supply made by a taxable person in the course or furtherance of any business carried on by that person. A taxable supply is a supply of goods or services made in the UK other than an exempt supply. Exempt supplies are set out in Schedule 9 of the VAT Act 1994 (‘VATA’). This includes supplies of insurance services within group 2 of Schedule 9.

A taxable person has the right to recover input tax attributable to 1) taxable supplies, 2) supplies made outside of the UK that would be taxable supplies if made within the UK and 3) such other supplies outside the UK and exempt supplies as the Treasury may order. Unless an order exists to the contrary, where a supply is exempt the taxable person cannot recover any input tax relating to that exempt supply. Therefore an insurance intermediary making exempt supplies only will generally not be able to recover its input VAT (e.g. on overheads and outsourced services).

The VAT (Input Tax) (Specified Supplies) Order 1999 (the ‘Order’), which relates to exempt supplies of services under Group 2 of Schedule 9, is such an order. Broadly, the Order states that where the supply of services are supplied to a person who belongs outside the EU, input tax recovery is allowed if the supply would have been exempt if made in the UK. HMRC consider that a number of insurance companies utilise these rules to ensure recovery of input VAT which would other wise be irrecoverable – by looping services through a non-EU company.

Hastings v HMRC

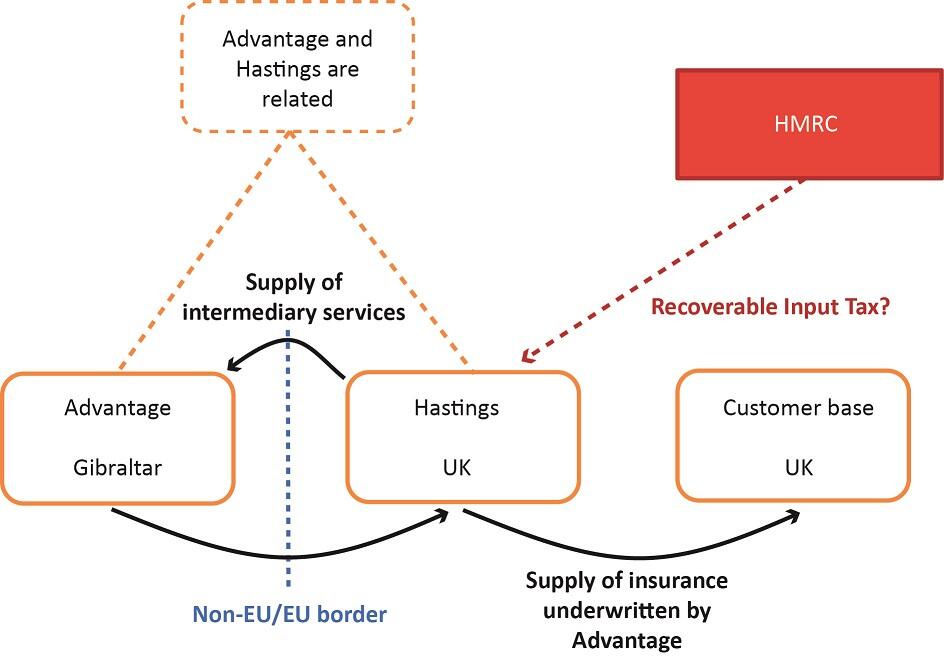

The Hastings case was HMRC’s (failed) attempt at challenging such arrangements in the Courts. As illustrated, Hastings is an insurance company in the UK which provides services to Advantage, a company based in Gibraltar (outside of the EU for VAT purposes) which underwrites insurance for a UK customer base using Hastings as its intermediary. Hastings and Advantage have at different periods been connected or related under GAAP, but are separate businesses with their own management, commercial aims and risk taking. The question was whether Hastings could recover or obtain credit for input VAT attributable to the supplies it made to Advantage. If the place of those supplies was within the UK, Hastings would not be entitled to recover the input VAT as the supply of its service to Advantage was exempt from VAT. However, if the place of supply was outside of the EU then Hastings would be entitled to recover the input VAT under the Order. See figure 1.

Place of supply rules

The UK place of supply rules for services state that where the recipient is a ‘relevant business person’ the place of supply is treated as being where that relevant business person belongs. Where the relevant business person belongs is determined in accordance with VATA s 9, as follows:

- if the person has a business establishment (‘BE’), or some other fixed establishment (‘FE’), in a country and none in any other country, that country;

- if the person has a BE, or some other FE, in more than one country, the country in which the establishment which is most directly concerned with the supply is;

- otherwise, the country in which the person’s usual place of residence or permanent address is.

The test is sequential and case law has consistently held that this is the case unless it gives an irrational result.

In order to determine where Advantage belonged, it was important to understand where it had its BE and FE (if any). These terms are not defined in UK legislation (definitions provided in Council Implementing Regulation 2011(282/2011/EU) may be relied on) but HMRC does provide some guidance on these terms in VAT Notice 741A. Although the guidance doesn’t give much more information than the EU definitions, HMRC does set out a number of examples of FEs.

Arguments: common ownership

It was agreed by all parties that Advantage had a BE in Gibraltar. However, HMRC argued that Hastings made supplies to the UK customer base on Advantage’s behalf and as Hastings’ human and technical resources were available to Advantage via on-going contractual arrangements, Advantage also had an FE in the UK.

It is clear when looking at HMRC’s VAT Notice, that this argument demonstrates a marked change in HMRC’s view on the importance of common ownership in creating an FE; most of the examples contained in the VAT Notice point to some element of common ownership – owning a property, a subsidiary or a branch. Clearly Hastings did not fall within any of these examples. Hastings was not a subsidiary of Advantage acting in Advantage’s name; it provided services to a panel of underwriters and not solely to Advantage, and importantly Hastings operated a separate autonomous business to Advantage. HMRC’s argument above also confusingly places significant emphasis on contractual relationships between underwriters and intermediaries. If common ownership was not necessary for an FE contractual links could be enough to establish an FE – potentially significantly widening the test.

Arguments: consumption

HMRC also argued that all that was needed for an FE to exist was for Hastings’ human and technical resources to provide Advantage with a framework comprising all that was necessary for the ‘customer facing’ side of the UK business – revealing HMRC’s actual mind-set that UK tax should be applied where there are sales to UK consumers. Seemingly, where this isn’t the case, HMRC consider UK tax is being avoided. HMRC contended that although the place of supply rules are usually to be applied in sequential order, doing so in this case would potentially lead to distortion of competition and therefore if Advantage was operating through an FE in the UK, that FE should take precedence over its BE in Gibraltar. It has always been thought that the FE rule would override the BE rule in exceptional cases only. However, HMRC relied on cases, such as the DFDS case C-260/95 to argue that the FE rule should override the BE rule because:

- VAT must be applied in a manner as far as possible in harmony with the actual economic situation and be charged at the place of consumption; and

- otherwise there could be a distortion of competition, i.e. a company with a non-EU BE could avoid establishment in the UK in order to gain a tax advantage.

These arguments are broad and cast doubt over the extent to which businesses can rely on the primacy of the BE rule. In fact, perhaps HMRC will soon want to see that the FE rule overrides the BE rule as long as an FE can be found in the same jurisdiction as the consumer!

Judgement

Luckily, the FTT concluded in Hastings that ‘it is clearly not envisaged that the resources of an entity comprise a FE of another legal (albeit related) entity as a result of the provision of service under commercially agreed contractual arrangements where, in fact, each entity operates a separate business with its own commercial imperatives and financial risk taking’. The fact that the two businesses were mutually dependant on each other did not detract from that. Hastings was not an FE of Advantage, Hastings was supplying to Advantage at its BE in Gibraltar and so Hastings’ UK input tax relating to those supplies was recoverable from HMRC.

The Amended Order

Unsurprisingly, the benefits of the FTT ruling for the insurance sector are now lost. HMRC chose to avoid a costly appeal to the UTT and instead the Government enacted the Amended Order to counter such arrangements. Insurance intermediaries that provide intermediary services to non-EU insurance companies in respect of insurance ultimately provided to a UK customer base will no longer be able to recover input VAT attributable to their supply of services to the non-EU insurance company. However, the order should still apply if the insured belongs outside the UK.

The Amended Order achieves this by restricting application of the Order for insurance companies to circumstances where the insured belongs outside of the United Kingdom – completely side stepping (replacing?) the place of supply rules and going straight to what HMRC were probably always trying to achieve and what is clearly becoming the norm in the tax world: consumer-based taxation.