Tax threshold freezes: the impact of fiscal drag

Share this article

Frozen tax thresholds until 2031 will steadily raise tax bills, making proactive remuneration and income planning increasingly important for employees and employers.

Key Points

What is the issue?

Freezing income tax thresholds until 2031 increases tax liabilities through fiscal drag, despite no headline rise in tax rates.

What does it mean to me?

Employees and employers will face higher effective tax and NIC costs as wage growth pushes more income into higher tax bands.

What can I take away?

Careful remuneration planning – including pensions, salary sacrifice and non-cash benefits – can help to mitigate the impact of frozen thresholds.

Since the Budget, there has been much debate over whether Rachel Reeves and the Labour government have breached their manifesto pledge not to raise income tax. Whatever the political arguments, the practical position for taxpayers is clear: income tax thresholds are frozen until 2031. In this article, we will look at what that freeze means in practice for both employees and employers.

Income tax rates and thresholds have been devolved to Scotland; this article does not consider the position for Scottish taxpayers. Income tax rates but not thresholds have been devolved in a limited way to Wales but so far the Senedd has followed the UK-wide rates.

We look at which elements of income tax have been frozen, how this is likely to affect tax liabilities over the coming years, and what steps taxpayers and businesses may be able to take to help to mitigate the impact of these changes.

What did Budget 2025 do?

Chancellor Rachel Reeves confirmed an extension of existing freezes so that personal tax thresholds remain fixed in cash terms until 6 April 2031. This freeze was first announced in March 2021, meaning that by the end of the period there will have been nearly a decade without any change to the income tax bands and the personal allowance.

While taxpayers will not see an explicit change in income tax rates, extending the freeze to 2031 will intensify the effect of fiscal drag on earnings. As wages rise, a greater proportion of income is taxed and more income is pulled into higher tax bands. This may contribute to wage inflation, but for employers it also means higher costs.

The main employer National Insurance contribution (NIC) rate rose to 15% in April 2025 and the secondary threshold (the point at which employer NIC becomes payable) fell to £5,000. Together, these measures already significantly increase the marginal cost of employees’ salaries.

It is important to note that some employees will also be affected by changes to pension salary sacrifice, which has long been an efficient way of making pension contributions. From April 2029, NIC relief on employee pension contributions made through salary sacrifice will be capped at £2,000 per person per year. Amounts sacrificed above £2,000 will attract both employer and employee NIC, although income tax relief remains unchanged.

While there was no change to income tax rates on earned income, the Budget introduced higher bands for savings and property income.

From April 2027, savings and property income will be taxed at rates 2% higher than currently:

- Basic rate: 22%

- Higher rate: 42%

- Additional rate: 47%.

In practice, this mirors the pre‑Budget suggestion of applying National Insurance to property income but does so more straightforwardly and with less administrative complexity.

Dividends are also affected. From April 2026, the Budget introduces a 2% increase in dividend tax rates for the basic and higher bands. The basic rate will rise from 8.75% to 10.75%, and the higher rate from 33.75% to 35.75%. The additional rate band will remain unchanged at 39.35%.

From 6 April 2027, the ordering rules will also change, so that the personal allowance and other reliefs must first be set against non-investment income (employment, trading income and pensions). Savings, dividends and property income will then be taxed afterwards using their own band.

This effectively treats investment income as the ‘top slice’, pushing it more frequently into higher or additional rate bands.

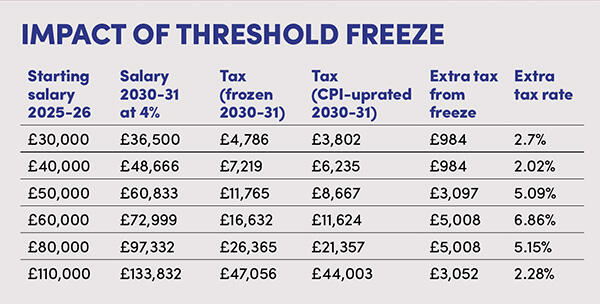

What does this mean in practice?

The table above models the effect of the threshold freeze and fiscal drag through to 2031. It assumes that pay grows by 4% a year and compares the tax payable based on frozen thresholds with the tax payable if thresholds had been uprated in line with the Consumer Price Index (CPI).

ICAEW’s analysis of Office for Budgetary Responsibility (OBR) figures indicates that by 2030-31 the personal allowance would be around £4,920 higher and the higher rate threshold around £20,120 higher than the frozen values. The additional rate threshold is assumed to remain unchanged, in order to focus on the key bands where fiscal drag is most keenly felt.

Based on the modelling, several key points stand out:

- The freeze raises the total tax most for households pushed across the higher-rate threshold – the ‘cliff’ where 40% tax begins.

- At higher incomes, the difference narrows, largely due to the personal allowance taper (which removes the allowance altogether by £125,140) and the fixed additional rate threshold.

While this analysis focuses only on income tax, the freeze is likely to have more of a bite when combined with higher employer NIC, the changes to dividend, saving and property rates, and the high income child benefit charge.

Mitigating the impact

To combat the effects of the freeze, employers will increasingly be looking for ways to reward employees in the most efficient way – without inadvertently dragging them into higher rate tax bands.

With employer NIC at 15% and the secondary threshold down to £5,000, pure cash awards have a steeper marginal cost. As a result, employers are likely to focus more heavily on ways they can reward employees in a tax-efficient manner.

We have outlined some of the options below. Converting a portion of annual pay increases into employer pension contributions, electric vehicle leasing or universal benefits is likely to become more common. These options are particularly valuable for those in the £50,000 to £60,000 range, who are amongst the hardest hit by fiscal drag.

Pension optimisation

Pension contributions remain a powerful tool for structuring employment packages efficiently.

The cap on NIC relief for employee salary sacrifice does not take effect until April 2029. Until then, maximising pension contributions through salary sacrifice can still deliver full NIC and income tax saving.

Even after April 2029, salary sacrifice will remain attractive. Income tax relief continues to apply, though NIC relief is only available on the first £2,000 of contributions every year for both employees and employers. As income tax relief will continue to apply, for employees in the ‘taper zone’ of £100,000 to £125,140 well-sized pension contributions can restore the personal allowance and significantly reduce the effective marginal tax rate. A similar approach applies for those affected by the high income child benefit charge.

Crucially, ordinary employer pension contributions remain fully exempt from NIC after April 2029. This is likely to impact how remuneration packages are structured going forward. That being said, while pension contributions are a fantastic way to save for the future, they do not address people’s immediate cost-of-living pressures.

Electric vehicles via salary sacrifice

The tax-efficient provision of company cars can materially reduce the pressure of household costs.

The benefit-in-kind rates for company cars are still at a very low rate. The rate on pure electric vehicles is 3% in 2025-26, rising gradually to 9% by 2029-30. Even with higher employer NIC, electric vehicles salary sacrifice arrangements typically leave employees materially better off than comparable personal leases, while also helping employers to meet net-zero and ESG targets.

The Budget’s per-mile levy from 2028 is modest in the early years and does not fundamentally alter the salary sacrifice mechanics.

Universal, tax-efficient non-cash benefits

While the range of tax-free benefits that can be given to employees has been restricted over recent years, several options remain. Some of these benefits can also support employers’ desires to increase office attendance.

For example, where a canteen or meal facility is made available to all employees at a location and provided on a reasonable scale, the benefit is exempt from income tax and NIC. Care must be taken to ensure that the benefit is not delivered through salary sacrifice, which would disapply the exemption.

This can be a simple way to boost the total reward without triggering a tax liability. It can also help to create a pleasant working environment at a time when many employers are pushing to attract employees back to the office.

Cycle-to-work schemes and other cycle provision made generally available to staff, and used mainly for qualifying journeys, remains beneficial. E-bikes are included. Despite pre-Budget speculation about caps, the scheme continues unchanged and is an efficient, cost‑effective way to support health and sustainable commuting while protecting net pay.

Employer-provided mobile phones also remain exempt from income tax and NIC, provided that they are supplied without transferring ownership, the contract is in the employer’s name, and the exemption is limited to one phone or SIM per employee. The exemption covers the handset, line rental and private calls. While tax-efficient, some employees may be less keen on this if they feel it increases expectations of accessibility outside work hours.

Managing expectations and minimising surprise

The most corrosive element of fiscal drag is surprise: the sudden realisation that a modest pay rise has pushed someone into higher-rate tax or intensified the personal allowance tapering.

Employers should be particularly mindful of employers clustered around the £50,270 threshold and those in the £100,000 to £125,140 range, where the impacts of tax cliff edges are most keenly felt. Clear communication with these employees about the structure of their remuneration packages will be crucual.

Employers may also want to consider providing access to financial planning support for their employees, helping them to understand and navigate the impact of these changes and with ongoing planning.

© Getty images