Is there a place for multiple trusts?

Share this article

In the second of our articles on multiple trusts, we ask whether it will be worthwhile to establish a number of different trusts in the future.

Key Points

Key Points

What is the issue?

In the future, it is worth considering whether having a number of settlements will be advantageous.

What does it mean for me?

Dividing an asset between trusts may still be worthwhile on valuation grounds if, for example, a majority shareholding is split so that each trust holds a minority interest valued accordingly on the ten year anniversary. >

What can I take away?

The use of multiple trusts may still have valuation advantages even after the changes in Finance (No 2) Act 2015, particularly in the case of business property.

In the January 2022 issue of Tax Adviser, we examined the changes that had been made to trusts from 18 November 2015 in Finance (No.2) Act 2015. Following those amendments, when calculating the rate of tax charged under the relevant property regime, the value of non-relevant property in the same or a related settlement is now excluded.

In the future, it is worth considering whether having a number of settlements will be advantageous.

Advantages of multiple trusts

There is no point in trying to circumvent same day additions and obtain multiple nil rate bands for multiple trusts. However, dividing an asset between trusts may still be worthwhile on valuation grounds. If, for example, a majority shareholding is split between, say, five trusts from the outset, each trust holds a minority interest valued accordingly on the ten year anniversary. The sum of the whole is likely to be greater than the individual parts.

There are no provisions to aggregate values where the same settlor has set up and funded different trusts from the outset. There is nothing similar to the related property valuation provisions in Inheritance Tax Act 1984 s 161. However, if say four identical trusts are used for one company shareholding purely to minimise values at a ten year anniversary, consider carefully whether a DOTAS report needs to be made.

There may well be other non-tax reasons to use multiple trusts; for example, if different branches of the same family have different long term objectives. Sometimes a settlor prefers to have separate trusts for each child and their respective families, despite the additional administrative costs and even if there are no obvious valuation advantages.

If the settled property is likely to increase substantially in value after it is settled, it is better to split the property among a number of different settlements from the start. This is because the property in each settlement will only be aggregated with historic values settled into the other trusts. Note that a decision has to be made from the outset if multiple trusts are desired. It is not possible to set up one trust and then sub-divide it into 10 separate trusts later, as s 81 will treat the property as remaining comprised in one trust for the purposes of the relevant property regime.

A further decision is whether to settle property into different settlements by transfers all made on the same day, so that aggregation is of property comprised in related settlements or in same-day additions. Alternatively, a series of transfers could be made on different days, so that the settlements comprising the property transferred later in the sequence have to be aggregated with the settlor’s chargeable transfers made earlier in the sequence.

Same-day additions and property initially in a related settlement are included at their value when settled taken by themselves, but not taking into account any business or agricultural relief. Previous chargeable transfers of the settlor do take into account any business or agricultural relief, but absent such relief, the values of those transfers will add up to a ‘loss to the transferor’ value, which reflects the value of the asset being fragmented taken as a single asset. So generally it is preferable to use trusts set up on the same day for property investment companies, but successive trusts for companies qualifying for business property relief.

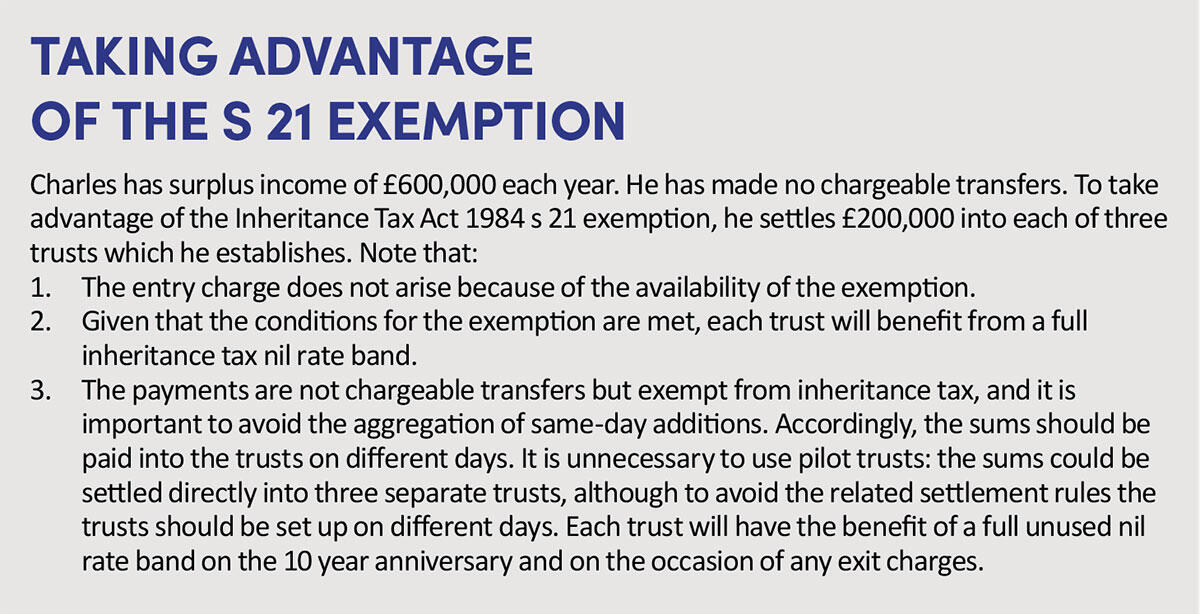

Normal expenditure out of income

Avoid related settlements where normal expenditure out of income exemption is in point. This exemption is available for gifts out of the income of the taxpayer, provided that such gifts are ‘normal’ (i.e. are part of a pattern of payments) and do not have the effect of reducing his standard of living (see Inheritance Tax Act 1984 s 21 and Bennett v IRC [1995] STC 54).

Excluded property

Where a settlor is not domiciled in the UK and is settling property situated outside the UK but the trust may in future hold UK situated property (e.g. a UK house), there may be long term advantages in having a number of different settlements, particularly if the settlor has made no chargeable transfers in the preceding seven years. As long as the settled property remains excluded property, it does not make any difference whether it is comprised in one settlement or several. However, if any of the property becomes relevant property – for example, the trustees buy UK land – then if the settled property has been divided among a number of settlements, each settlement will have its own nil rate band in the event of a periodic or exit charge.

Replacement property

Settling property qualifying for business property relief into multiple trusts is sensible if there is any risk of the donor dying within seven years and the property being sold. The replacement provisions in ss 113A and 113B require the donee who sells business property to use the entire sale proceeds to buy replacement business property. If the shares are split between, say, two trusts, each trust can decide whether to invest their sale proceeds in new property to avoid a clawback of relief. It allows Trust 1 to invest in non-business assets without jeopardising relief on Trust 2, which reinvests the proceeds from their shares.

Disadvantages of multiple trusts

There are downsides in having multiple trusts. Apart from additional administrative costs, setting up a series of trusts will restrict the annual capital gains tax exemption and income tax standard rate band of the trusts. Later transfers of assets between separate settlements will be capital gains tax disposals and may have stamp duty land tax disadvantages (contrast transfers between sub-funds of a single settlement, which give rise to no capital gains tax or stamp duty land tax). Losses of one trust cannot be set against gains of another.

Conclusions

The use of multiple trusts may still have advantages even after the changes in Finance (No 2) Act 2015, particularly in the case of business property. The advantages for excluded property trusts is because of, rather than despite, Finance (No 2) Act 2015, given that non-relevant property comprised in related settlements is no longer included when calculating the rate. It is perhaps surprising that there are not provisions similar to those of related property between husband and wife that apply to trusts set up by the same settlor.

As for pre-2014 trusts, watch carefully any additions to such trusts by the settlor in case this jeopardises existing protected status.

A detailed survey of the technicalities of relevant property regime and the variety of different trusts can be found in the forthcoming 5th edition of Chamberlain and Whitehouse on Trust Taxation.