Thus far but no further

Share this article

Ray Chidell considers the capital allowances case of Telfer v HMRC and argues that HMRC may be overstepping the mark with some of the restrictions on claiming allowances

Key Points

What is the issue?

Capital allowances for plant and machinery may be available for employees, but first principles concerning the definition of plant must still be considered.

What does it mean to me?

Some of the statutory restrictions preventing claims for capital allowances are onerous, but there is a danger that HMRC may take those restrictions too far.

What can I take away?

HMRC reasoning is not always correct, and there are plenty of grey areas in relation to capital allowances.

When Apple launched the iPhone 7 in September, the BBC’s Rory Cellan-Jones made an ironic comment about tapping ‘a huge audience of swimmers who want to play Pokemon Go underwater’. By the same token, a tax case concerning a capital allowances claim by an employee for the cost of two caravans may appear to be of rather narrow application, even for readers of this esteemed publication. The reality, however, is that the recent decision in Telfer v HMRC [2016] UKFTT 614 (TC) is something of a textbook case for addressing three key principles of capital allowances law.

Mr Telfer was an employee of the Caravan Club. His claim ultimately failed, but he successfully negotiated two of the three hurdles before falling at the third. HMRC’s reasoning on some aspects of the case was poor.

Capital allowances for employees

Most capital allowances claims for plant and machinery are made for trades (including professions) and property businesses, but the list of qualifying activities also has various other categories, including that of ‘an employment or office’ (CAA 2001 s 15). In principle, therefore, an employee may be able to claim allowances for the cost of plant or machinery.

Some special rules apply, however, to restrict the extent to which employees may claim allowances (s 36). The most familiar restriction is for cars, though in reality the scope of the exclusion is somewhat wider as it catches any mechanically propelled road vehicle, and also cycles (s 36(1)(a)).

Mr Telfer’s caravans, each costing in the region of £20,000, were not mechanically propelled and so did not fall foul of that provision. It was still necessary, however, to consider a second restriction, which denies allowances for employees unless the plant or machinery is ‘necessarily provided for use in the performance of the duties of the employment or office’ (s 36(1)(b)). Anyone familiar with employment tax law will know that the dual tests of ‘necessarily provided’ and ‘in the performance of the duties’ together present a formidable obstacle that has denied tax relief to many employees, whether the expenditure in question was capital or otherwise.

The key facts in this case were that Mr Telfer and his wife were both employed by the Caravan Club for various intermittent periods, under a succession of separate contracts, starting in 2007 and continuing until at least 2013. From 2009, the role was of ‘assistant warden’. Assistant wardens were required to live on site but were rarely (if ever) provided with accommodation. According to the terms and conditions, ‘wardens will normally live on Site in their own caravan/motor home on a pitch provided for them’. Wardens and assistant wardens were also provided with certain shower, WC, refrigeration and other facilities.

Unsurprisingly, HMRC sought to argue that the ‘necessarily provided’ test was a rigorous one and that the necessity had to be imposed not by the employer but by the duties of the employment themselves.

On this aspect, the Tribunal found for the taxpayer: ‘We accept that the test imposed by section 36(1)(b) CAA goes beyond a legal requirement by the employer that the asset concerned is provided by the employee and requires an examination of whether or not the duties of the employment objectively require the provision of the asset. In this case, the duties of Mr Telfer’s employment did objectively require him to live on site “in his own outfit”. The duties required Mr Telfer to be on site at all times, and to be ready to move to another site at the Caravan Club’s discretion, and on any realistic basis this means that those duties required him to live in his caravan on site. The caravans were used (as shelter and living accommodation) by Mr Telfer in the performance of the duties of his employment(s).’

The decision with regard to this aspect seems reasonable on the facts. Although not directly referred to in the case report, the outcome does not appear to be in serious conflict with HMRC’s guidance on this issue in the Employment Income Manual at EIM 36560: ‘If the expense is substantial, it would be reasonable to expect the contract of employment to include a specific reference to the requirement to incur it. If there is nothing explicit in the contract, find out whether the employee has approached the employer to provide the item, or to reimburse its cost, and, if so, with what response. If the employer is not prepared to bear the cost and advances the view that the expense is not considered necessary this will clearly weaken the taxpayer’s claim, though without being entirely conclusive.’

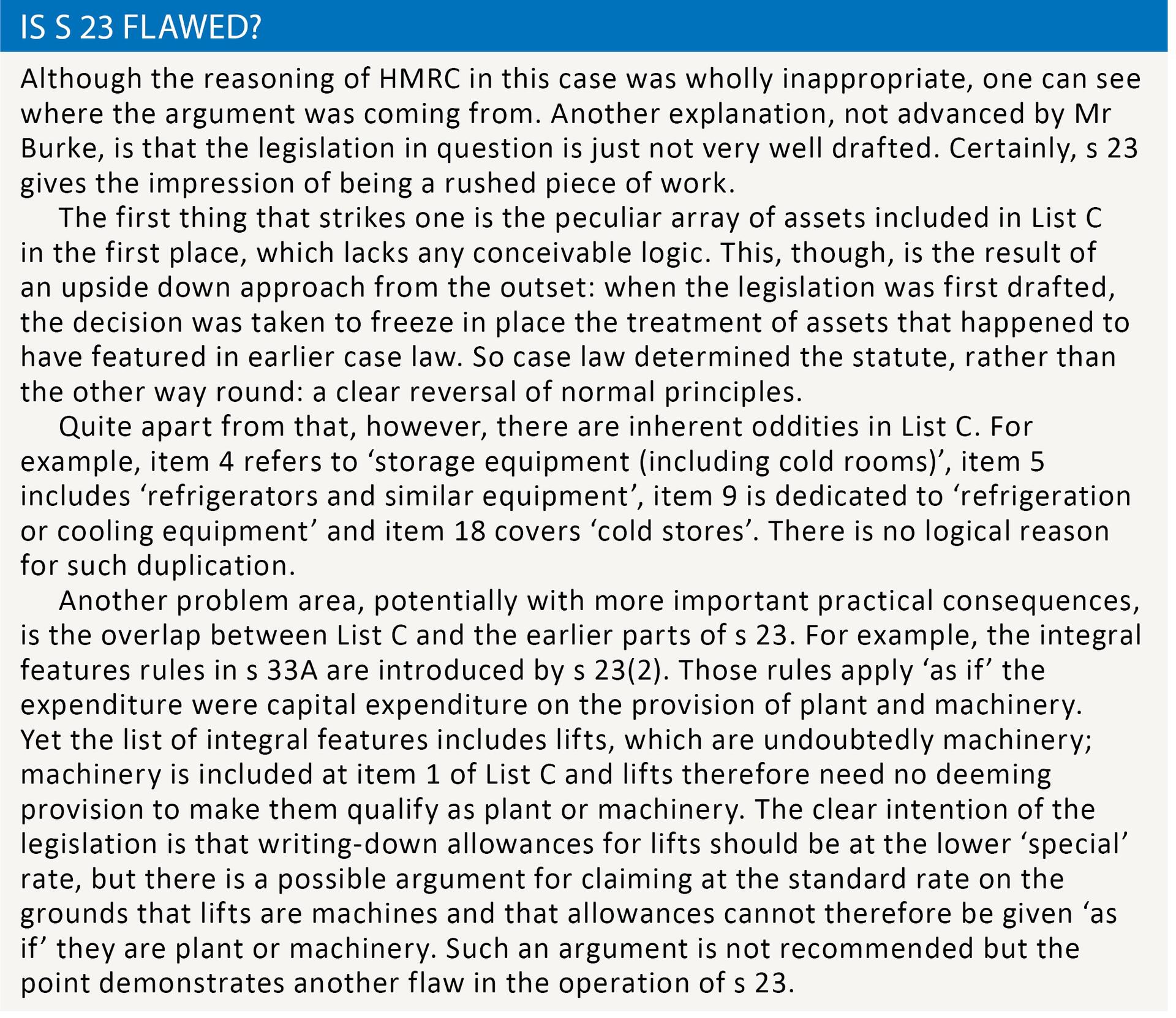

Buildings and structures

The provisions of CAA 2001 ss 21–23 come into their own in the context of fixtures in property, so it was rather surprising to see them making an appearance in relation to a pair of moveable caravans.

The HMRC reasoning on this point was inappropriate and misguided, so it is worth being clear about the way these sections work.

As a reminder, s 21 denies allowances for most buildings, and s 22 has a similar effect for structures. However, s 23 then disapplies both of those sections in relation to a wide variety of specified assets, allowing the treatment of many items to be considered on normal case law principles, unhindered by any statutory restrictions.

As an illustration, fire alarm systems are incorporated in a building, and allowances are therefore initially denied by virtue of s 21(3). However, they are also included in ‘List C’ at s 23. This rescues them from the statutory restrictions of s 21 and allows their treatment to be determined on case law principles. Those principles lead to a clear conclusion that fire alarms are plant, so allowances may be claimed.

The proper approach to this legislation is therefore clear enough. The only effect of s 23 is to undo the mischief imposed by ss 21 and 22, so if those two earlier sections do not apply we do not need to worry about s 23. In this case, it was clear that the caravans in question were not buildings. Furthermore, nobody was suggesting that they were fixed structures (as would be required for the restriction to be imposed). So the three sections were of no relevance.

HMRC argued, however, that they must indeed be of relevance as item 19 at List C refers to ‘caravans provided mainly for holiday lettings’. Unfortunately, the wording of the Tribunal case report – for the most part clear – is not as helpful as it might be at this particular point: ‘Mr Burke [for HMRC] argued that we should infer from the inclusion of item 19 in List C in section 23(4), that the exclusion of expenditure on the provision of buildings, structures and other assets in section 21 and 22 from the relevant concept of expenditure on plant or machinery, that expenditure on some caravans came within that exclusion.’

Although inelegantly expressed, the intended meaning is reasonably clear. HMRC were arguing that as item 19 removes a restriction on claiming for certain caravans, it must follow that caravans generally are within the restrictions for buildings and structures in the first place. It is common enough to see poor statutory logic coming from unrepresented or badly represented taxpayers at Tribunal, but this is an inexcusable stance from HMRC. If they wished to bring these sections into play, the onus was entirely on HMRC to demonstrate that the caravans in question were either buildings or fixed structures. In reality, of course, they were clearly neither.

In rejecting the HMRC stance on this point the Tribunal was back to its normal clarity: ‘This is an argument from redundancy – that is, an argument that it would be redundant for a class of caravans to be excluded from the application of sections 21 and 22 by section 23 CAA, if section 21 or section 22 did not apply to caravans. Lord Hoffmann famously said that he seldom thought that an argument from redundancy carried great weight (Walker v Centaur Clothes Group Ltd [2000] 1 WLR 799 at 805D), and we respectfully agree. Further, it seems to us that section 21 or section 22 CAA could only apply to fixed caravans and plainly Mr Telfer’s caravans were not fixed.’

Precisely!

One possible explanation for the apparent anomaly is that s 23 is in fact flawed legislation, a point explored below.

But is it plant?

Having negotiated the employment tax hurdle, and (to change the sporting metaphor) having booted the s23 nonsense into touch, the taxpayer still had to face one last test if his claim was to succeed. (A question about pre-trading expenditure also arose, but that was of no great interest in this case.)

This last test was the most fundamental issue of all, namely the question of whether the caravans were plant on ordinary case law principles. Sadly (but correctly, on the facts) the Tribunal held that they were not: ‘Although we readily accept that Mr Telfer could not legally (via-à-vis the Caravan Club), or realistically on the facts, have performed the duties of his employment as an assistant warden without the use of the caravans, we are driven to the conclusion that the caravans were not something by means of which those duties were in part carried on, but were instead structures which played no part in the carrying on of those duties, but were merely the place within which they were carried on.’

In summary

In my view, the Tribunal reached the right conclusion in this case, and for all the correct reasons. The employment tax issue was a difficult one, but the Tribunal came down on the right side of the line. The s 23 argument should never have been advanced by HMRC and was properly given short shrift. But in the end, the question of whether something is or is not plant always depends both on the nature of the asset and the use to which that asset is being put; in this case, the caravans were functioning as premises and not as apparatus, and were therefore not plant. So HMRC rightly won the day, but in one sense did not deserve to do so. Paradoxically, it is the meaning of plant that usually offers so much scope for argument, but in this instance that aspect was rather clear cut and the interesting points at dispute were in relation to other provisions of the capital allowances legislation.