Uniformed VAT

Share this article

VAT on staff benefits – Uniformed VAT

Key Points

What is the issue?

There are VAT savings to be made on staff benefits and perks, but output tax is due on many supplies of goods given free

What does it mean for me?

Many HMRC officers apply checks to staff-related issues on compliance visits, so it is important to be aware of the rules and the correct treatment to adopt

What can I take away?

It is difficult for free clothing given to an employee to qualify as a ‘uniform’

Imagine this: you are a clothes retailer who gives your staff a quarterly allowance of free clothing. They will wear some of the items while on duty and some will be used away from work only. What is the VAT position in relation to these free supplies of stock? The answers may be sought in a First-tier Tribunal case involving a major high-street retailer. However, other staff perks common in the business world may also be liable to VAT.

Business gift rules

A gift of goods or services takes place if no payment is received from the recipient. It should always be remembered that payment can be in a non-monetary form as well as cash. Nearly 30 years ago as a Customs and Excise officer I visited a window cleaner who was plying his trade in return for free golf club membership, free meals at restaurants and even the free use of a car from a local hire company. There was no gift situation here and there was an output tax liability on the value of the benefits he had received from all of these customers.

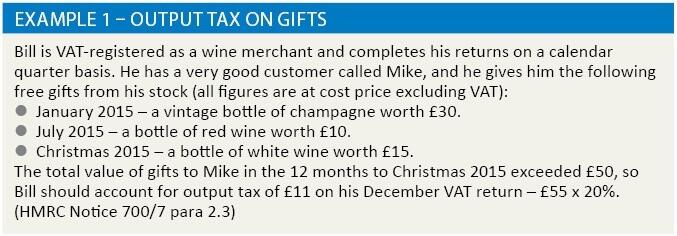

The good news is that a business providing free services does not usually have an output tax liability. But the rules are different for goods. In such cases, no output tax is due if the value of the gift, including the total of all other gifts to the same person in any 12-month period, is less than £50 and the gift was given for business purposes, perhaps to reward a loyal customer or staff member. The £50 limit is VAT exclusive and is based on the cost of the item to the business when it bought it, rather than the retail price. The bad news is that, if the £50 limit is exceeded, the earlier gifts also become subject to output tax. See Example 1.

As a final twist to the tale, what would be the situation if Bill bought a case of wine for his friend Steve’s birthday, with whom he has no business dealings, and paid for the wine through his business bank account? In this situation, the input tax on the purchase should be blocked because it is not relevant to taxable supplies, or if Bill is diverting existing stock where input tax has already been claimed, he should account for output tax on the day the wine is given to Steve.

What is a uniform?

The issue in the case of French Connection Ltd (TC43467) was whether free clothing given to employees represented a supply for VAT purposes and therefore a liability for output tax purposes. Each employee receives a quarterly clothing allowance. This is free unless the employee leaves the company within three months of receiving the items, in which case they are charged an amount equal to 30% of their annual allowance through their salary and output tax is paid on these deductions.

The taxpayer agreed that the supply was subject to output tax if the annual value of the gift exceeded £50 but claimed that the items relating to store staff were for a business purpose – as a uniform – so no output tax was payable. However, the tribunal disagreed and felt that there was no difference between a non-business or business purpose for the supply. If input tax had been recovered on the initial purchase of the goods, there was an output tax liability when they were given to the employee, adjusting for the £50 gift allowance. To quote from the report:

‘The wide variety of clothing which staff members may select, particularly to assist in promotion of the French Connection brand, means that in formal terms the description of such clothing as a “uniform” is not appropriate. The adjective “uniform” as defined in the Concise Oxford English Dictionary is: “The same in all cases and at all times; not varying.” We do not consider that the clothing is “uniform” in that sense.’

The taxpayer’s final argument was that the key date for output tax purposes was three months after the supply, at which point the employee would not be required to make any payment for the goods received if they were still in the company’s employment. The tribunal rejected this approach and confirmed that the relevant date was when the items were first supplied to the employee. HMRC’s assessment was therefore correct.

So the conclusion from this case is that it is difficult for an item of clothing to qualify as a ‘uniform’ if it can be used personally by employees when they finish work.

Food and drink for staff

Let us imagine another situation: a business wants to celebrate its trading success by hiring a private box at a football ground. The day’s festivities, including free food and drink, will be enjoyed by a 50-50 split of ten staff and ten customers. What is the input tax treatment on the costs?

The bad news is that there is an input tax block on the costs relevant to the customers under the business entertaining rules (HMRC Notice 700/65, para 2.1) but the position for the employees depends on their role at the game. If they are to act as hosts for the customers, to ensure they have a good day and place lots of orders with the company, the input tax is also blocked on their costs. But if they are able to enjoy the day without any hosting function, a claim on 50% of the costs is fine (HMRC Notice 700/65, para 3.3). This is because free supplies of food and drink to staff is considered to be a legitimate business expense as long as there is no hosting of non-staff involved.

Supply of mobile phones

A new employee has started work for a local firm of estate agents, and has been given a free pay-as-you-go mobile phone by his very generous employer. He will use the phone for business and private purposes and, as long as the monthly cost of the calls does not exceed £100 plus VAT to the employer (deemed to be the business use each month), the employee need not make a financial contribution. But if the bill exceeds this figure, the employee must pay the difference by a payroll deduction. What is the VAT position here?

The VAT rules on mobile phones supplied to employees are explained in VAT Notice 700, section 12A. In the situation above input tax can be fully claimed by the employer on the payment to the phone company, but output tax is payable on the contributions from the employee. If the employer allowed the employee to make unlimited private calls without payment, the employer would need to apportion input tax to reflect the non-business use. However, the commercial reality is that most employers allow employees to make a small number of private calls without charge, and HMRC demonstrate a common sense approach at para 12A.2.1:

‘We realise that in practice businesses…tolerate a small amount of private calls. We are prepared to treat such minimal use as being insignificant for VAT purposes and it will not prevent a business treating all the tax it incurs on calls as input tax.’

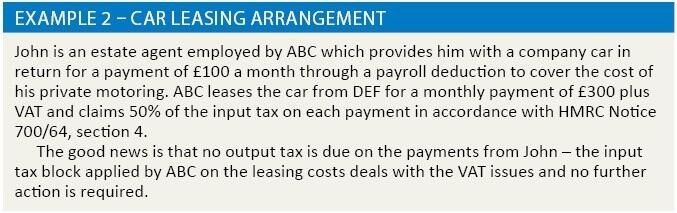

Final example – lease car and payroll deduction

Here is one of my favourite VAT tips because it is one that often causes confusion among advisers. In Example 2, there is no need to account for output tax on the £100 payments received from John because this would in effect give HMRC a double tax windfall if the input tax was also apportioned.

As a final reminder, remember that, if an employer claims input tax on road fuel bills where part of the fuel is used for an employee’s private travel, the easiest way to deal with the VAT challenge is to account for output tax with the scale charge system based on the CO2 emissions of the vehicle – see HMRC Notice 700/64, section 9.