VAT errors and adjustments: some practical examples

Share this article

What is the difference between a VAT error and an adjustment? We consider this question with the help of some practical examples.

Key Points

What is the issue?

VAT adjustments are declared on a return for both over and underpayments of tax. They are not classed as errors because they are made in accordance with the legislation. Common adjustments apply to partially exempt businesses, retail scheme users, and businesses that are not on the cash accounting scheme and incur bad debts.

What does it mean for me?

If adjustments are incorrectly notified to HMRC as error corrections, then any underpayments will usually be subject to interest, which could be costly. When annual adjustments are made on a return, the annual calculation always supersedes the declarations or claims made on returns submitted within the year.

What can I take away?

Errors where the net tax owed or owing is less than £10,000 can be included on the next VAT return rather than disclosed separately to HMRC. Larger businesses can adjust net errors of up to £50,000 on the return in some cases.

© Getty images/iStockphoto

HMRC has recently introduced a new online form to correct errors made by a business on past VAT returns. I have just used it for the first time to adjust a client’s output tax errors for the previous four years and – pause for dramatic effect – I give it a mark of ten out of ten. The main advantage of the form is that it can be both completed and submitted online to HMRC, and you are able to attach supporting documents to help HMRC verify that the claim is correct; e.g. Word documents and spreadsheets.

In this article, I will remind readers of the basic rules for correcting errors and also some important VAT adjustments that must always be considered. Adjustments are not classed as errors.

Bad debt relief

Claiming VAT on bad debts will be a subject of increased interest due to the economic recession. The basic rules for bad debt relief are straightforward:

- Bad debt relief only applies where output tax has been declared on a VAT return based on the invoice rather than payment date. In other words, the business does not use the cash accounting scheme where bad debt relief is automatic.

- If a sales invoice is more than six months overdue for payment and has been written off in the business accounts – crediting the sales ledger and debiting the profit and loss account with a bad debt expense entry – the VAT can be reclaimed on the next return. There is no error correction situation here; it is a VAT adjustment.

- There is an extra bonus if a business uses the flat rate scheme. (See VAT Notice 733 s 14.)

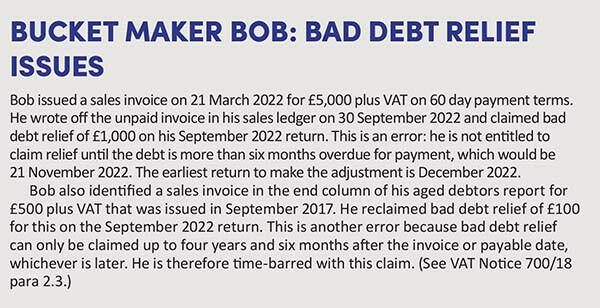

To share some twists with the rules, and an example of two errors rather than adjustments, see Bucket maker Bob: bad debt relief issues.

Partial exemption annual adjustment

Here is a VAT poser: when will a business that is partially exempt – having both taxable and exempt income – not have to do an annual adjustment calculation? The answer is: if the business uses the annual accounting scheme and therefore submits only one return a year, which coincides with its partial exemption tax year. However, all other partially exempt businesses must do the annual calculation, which is carried out up to 31 March, 30 April or 31 May, depending on the VAT periods of the business. It is 31 March for a business that submits monthly returns.

Here are three important tips:

- A business using the standard method – which is based on the percentage split between taxable and exempt sales – can round up its residual input tax claim to the next whole number if the residual input tax is less than £400,000 per month on average. So, for example, if 65.1% of sales are taxable, then 66% input tax can be claimed. Residual input tax is the VAT incurred on general overheads or costs that relate to both taxable and exempt activities; e.g. the cost of an advert in a newspaper that promotes the whole business.

- Any tax owed or owing after the calculation has been carried out must either be included on the March, April or May return or the return for the following period. The taxpayer has the choice, so if it is a repayment outcome, it is sensible to claim it on the earlier return.

- The partial exemption de minimis limits mean that up to £7,500 of input tax in a tax year relevant to exempt supplies can be reclaimed if it is also less than 50% of the total input tax figure. There are two other de minimis tests that can be used. (See VAT Notice 706 s 11.)

Retail schemes

A retailer that only has sales subject to one rate of VAT must always use a ‘point of sale’ retail scheme; i.e. where VAT is calculated at the time a sale is made. Retailers with sales subject to more than one rate of VAT – such as a clothes shop selling zero-rated children’s clothing and standard rated adult wear – can use a point-of-sale scheme but also has the choice of using four separate schemes: Apportionment schemes 1 and 2; and Direct calculation schemes 1 and 2 (see VAT Notice 727 s 3 for details about how they work).

So, quiz time again, what are the use restrictions for each scheme and which of them require an annual adjustment?

The first answer is that a business can only use Apportionment scheme 1 and Direct calculation scheme 1 if its annual taxable retail sales are less than £1 million excluding VAT. The other two schemes can be used by any business if annual retail sales are less than £130 million excluding VAT. If sales exceed the latter figure, the business must agree a bespoke scheme with HMRC.

In terms of annual adjustments, these are relevant for Apportionment scheme 1 and Direct calculation scheme 2; the latter scheme requires an annual stock adjustment.

Payback and clawback adjustments

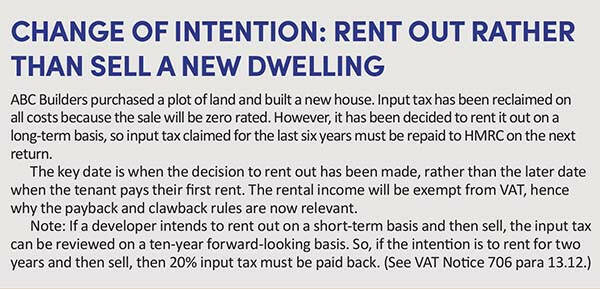

Imagine that you have a client who has built a house with a view to selling it. They have claimed input tax on their project costs because the sale will be zero-rated. But what happens if they change their mind and decide to rent it out on a long-term basis, so that the first income received will be exempt from VAT?

The payback and clawback regulations deal with the situation when expenses are incurred on a project where the sales are intended to be taxable but then the first actual sale is exempt from VAT. This is a ‘clawback’ situation because input tax needs to be repaid to HMRC. A ‘payback’ outcome means that intended exempt sales are superseded by actual taxable sales so input tax previously not claimed can be claimed on the next return. See Change of intention: rent out rather than sell a new dwelling.

Here are some important outcomes with the payback and clawback rules:

- Any adjustment with these regulations does not produce an ‘error’ situation. Corrections of under and overclaims of past input tax will always be included on a VAT return.

- The relevant time period for input tax adjustments is the last six years, which is different to the four-year period that applies to adjusting past errors on returns.

- A project might be intended to generate both taxable and exempt income – a mixed use – so the payback and clawback rules will apply if there is a chance of intention so that actual income is wholly taxable or exempt. The same rules apply if the change is vice-versa.

Error corrections procedures

If a past over or underpayment does not qualify as a VAT adjustment, it will be deemed to be an error. The audit trail is as follows:

- When the return is being completed, the business must calculate its total ‘net error’ figure for all errors made in the previous four years. If this figure is less than £10,000, it can be included on the return. So, if input tax has been overclaimed by £12,000 and output tax overpaid by £3,000 on past returns, the key figure is the £9,000 difference and not the fact that £15,000 worth of errors have been made.

- The tax can also be included on the return if the net error figure is between £10,000 and £50,000, and is also less than 1% of the total Box 6 outputs figure on the return where it is being corrected. So, for example, if your quarterly sales are £4 million in Box 6, you can include error adjustments of up to £40,000.

- If the net error exceeds the above amounts, it must be separately disclosed to HMRC, usually on form VAT 652. However, this can be done in a letter format if that is preferred.

- Errors that are more than four years old cannot be adjusted and are time-barred. The relevant date is the end of the VAT period; e.g. errors on the quarterly return to March 2019 can only be corrected on returns up to and including March 2023.