Worth next to nothing

Share this article

Caroline McCabe explains why negligible value claims are not of negligible value

Key Points

What is the issue?

Negligible value claims can be easy to miss, but this valuable relief should not be overlooked

What does it mean to me?

All negligible value claims should be reviewed regularly, especially towards the end of a tax year. It is vital that the claims are not left too late if they are to succeed. In particular, claims cannot be made once the asset has ceased to exist

What can I take away?

Claims can be backdated for up to two tax years. In some cases, losses from them can be set against taxable income, instead of gains

Negligible value claims can be useful in reducing an individual’s tax liability if they own assets that have become worthless since their acquisition. The legislation is found in TCGA 1992 s 24. Companies may also make negligible value claims on chargeable assets but this article deals solely with the personal tax aspects of such claims.

When a taxpayer makes a negligible value claim, they are treated as if they had sold the asset and immediately reacquired it for its value at the time the claim is made. This results in a capital loss that the taxpayer can set against capital gains and, in some cases, income.

To make a negligible value claim, the taxpayer must own the asset at the time the claim is made. Therefore, in order to make a claim in relation to shares in a company, the company must still be in existence. If a company has been dissolved, no negligible value claim can be made. In effect, the shares ceased to exist at the dissolution of the company, so can no longer be said to be in the taxpayer’s possession.

The claim must state the asset’s value at the time of the claim. Negligible value is not defined by statute, but HMRC states: ‘An asset is of negligible value if it is worth next to nothing’ (HS286). A list of shares formerly quoted on the London Stock Exchange that have been declared of negligible value by HMRC’s Shares and Valuations Office is updated monthly on the GOV.UK website.

Backdating claims

Negligible value claims can be backdated, as long as these conditions are satisfied:

- the taxpayer owned the asset at the earlier specified time;

- the asset had become of negligible value at that time; and

- the earlier time is not more than two years before the beginning of the tax year in which the claim is made.

This can be useful if a taxpayer has not made any capital gains in the current tax year but has done in the previous two. Since the asset must have already become of negligible value at the time to which the claim is being backdated, this will be useful only if the possibility of a negligible value claim was missed at the time of the earlier gain. However, it is conceivable that such an opportunity may come to light only when preparing the previous year’s tax return.

Since the claim can be backdated to the beginning of the tax year starting two years before the current tax year, it is especially useful to review the possibility of negligible value claims in the run-up to the end of each tax year. A claim made on 5 April 2016 can be backdated as far as 6 April 2013 (as long as the other conditions are met). If that claim were made only one day later on 6 April 2016, it could be backdated only as far as 6 April 2014, nearly a whole year later.

Purchased goodwill

A negligible value claim is also possible on purchased goodwill. However some basic conditions must be met, namely that the taxpayer still owns the asset at the time of the claim and the asset has become of negligible value since it was acquired.

Whether the goodwill has become of negligible value is a question of fact. It is not enough to show that it has been written off in the accounts. It must be shown that the goodwill of the business as a whole has next to no value at the date of the claim.

A negligible value claim cannot be made once the business has ceased to trade because, in effect, the goodwill ceases on the permanent cessation of the business to which it relates and therefore the taxpayer no longer owns the goodwill. An allowable loss may, however, arise under TCGA 1992 s 24(1), whereby the entire loss, destruction, dissipation or extinction of an asset constitutes a disposal of it for the purposes of TCGA 1992. The disadvantage of this is that such losses cannot be backdated like negligible value claims, so they will only be available to use against gains in the current tax year (or to carry forward for use against future gains). This highlights the importance of reviewing the possibility of negligible value claims before it is too late.

A partner can claim that their fractional share of goodwill has become of negligible value only if that of the entire partnership has become likewise. For instance, if a partnership agreement includes a clause that retiring partners will not be paid for goodwill and new partners do not need to buy goodwill, the goodwill becomes worthless to a partner on retirement. However, no negligible value claim is possible. Although the goodwill has become of negligible value to the retiring partner, the goodwill of the partnership as a whole has not.

Setting negligible value claims against income

In some circumstances, the loss arising from a negligible value claim can be set against income, either of the same or the preceding tax year (or both) instead of against capital gains. The relief must be claimed within one year of the 31 January after the year in which the claim is made. Thus, for negligible value claims made in 2015/16, the claim to set the loss against income must be made on or before 31 January 2018.

The rules governing this are contained in ITA 2007 s 131 et seq.

First, the assets must be qualifying shares. That is, either enterprise investment scheme (EIS) relief is attributable to them or they are shares in a qualifying trading company that have been subscribed for by the taxpayer. The conditions to be met by a qualifying trading company are similar to those for a qualifying EIS company. For instance:

- the shares cannot have been listed on a recognised stock exchange at the time of issue;

- the same gross assets test must be satisfied; and

- the list of excluded trades for EIS purposes applies.

However, unlike EIS relief, there is no limit on the number of employees a company can have.

In addition, the company must have been a trading company throughout the six years to the date of disposal, or for its entire existence if that is less than six years. If the company stopped trading before the disposal of the shares, the relief is still available if these conditions are met:

- the company stopped trading no more than three years before the disposal;

- the company has not started a non-qualifying activity (such as investment); and

- at the date it stopped trading, it satisfied the ‘six-years test’ explained above.

If the conditions are satisfied and a claim is made, the relief is given by deducting the allowable loss from a taxpayer’s total income before any income tax, such as the personal allowance. The claim cannot be restricted to preserve any income tax allowances available. Where the claim is made against income of both years, it must show which year is to take priority and must be used against the first year to the fullest extent possible (thus wasting the personal allowance for that year) before it can be set against income of the second year – see the Example.

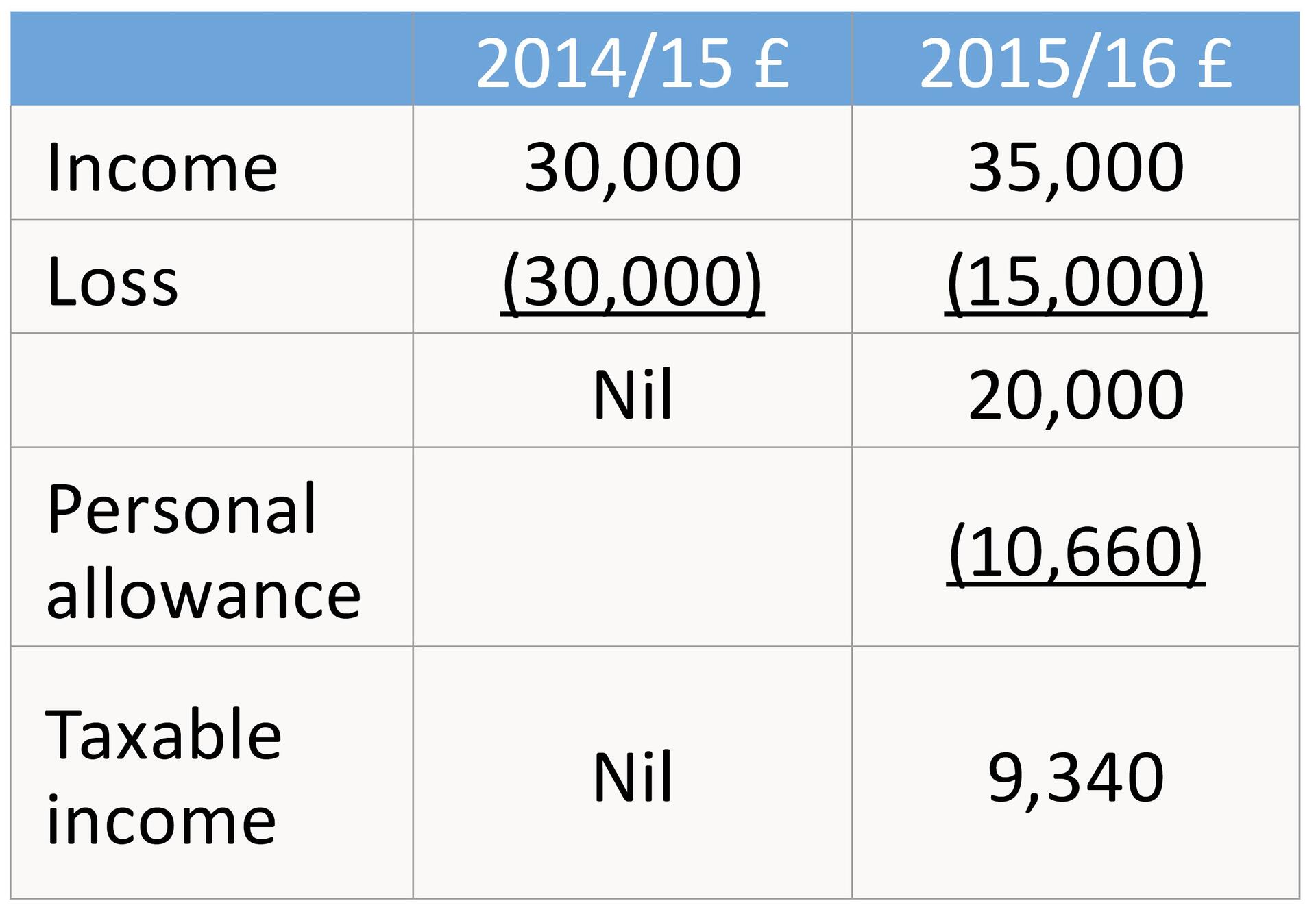

Example – Claim relief against two-year income

In 2002, Mrs Y subscribed £45,000 for ordinary share capital in a qualifying trading company. The company fails in July 2015 and Mrs Y makes a negligible value claim in 2015/16, when the shares are worth nothing. The allowable loss is £45,000. All the conditions for setting the loss against income are satisfied. Mrs Y’s income was £30,000 in 2014/15 and £35,000 in 2015/16.

Mrs Y claims first against 2014/15, using up as much of the loss as possible, as shown below:

Claiming against 2014/15 in priority to 2015/16 results in a slightly lower overall tax liability for Mrs Y because she preserves the use of the higher personal allowance in 2015/16.