Eat in or take away?

Share this article

Michael Steed returns to one of his favourite areas of tax and considers tax relief for ‘food on the go’

Key Points

What is the issue?

Food on the go is often raised as a deduction issue for both self-employed and employed taxpayers. zzWhat does it mean to me?The travel and subsistence rules are not always clear.

What can I take away?

Care is needed to correctly identify the rules and then to apply them.

Editor’s note: Since this article was written, our decisions about how and where we can eat and travel have been significantly impacted. We considered holding this article back until life starts to return to normal but, in a spirit of optimism, have decided to publish. We hope you don’t find it too tantalising…

One of the reasons that I signed up for tax is that some simple questions can have such complicated answers and food on the go is a good example! So, can I get tax relief for food on the go?

We need to break the problem into two areas: self-employed and employed. However, even this is complicated by the issue of workers in the gig economy, as the bipartite tax system does not accord with the tripartite employment law boxes of employed, self-employed and something in the middle (the worker or dependent contractor). (See the case of Uber v Aslam [2018] EWCA Civ 2748 about taxi driver employment rights.)

This doesn’t readily resolve into tax clarity. So, to make this analysis fit into a reasonable space, I will park the gig economy workers until a later article and concentrate instead on the tax analysis of self-employed and employed.

As a practical tool, my starting point is a general statement that if the travel is good, the food is good; by which I mean that if we can obtain tax relief on the travel expenses in question, it is generally true that tax relief on the food and drink is also obtainable. The position for self-employed taxpayers is in ITTOIA 2005 s 57A. Employees are entitled to tax relief for the full costs they are obliged to incur when travelling in the performance of their duties or when travelling to or from a place they have to attend in the performance of their duties – as long as the journey is not ordinary commuting or private travel (ITEPA 2003 ss 337 and 338).

I’d also like to make clear that in my analysis food and drink go together. As advisers, you don’t have to stand as moral guardians over your clients, worrying about the state of their livers. If you get tax relief for one, you get tax relief for the other. How many times at conferences have I heard advisers say: ‘Oh, I never let them have alcohol!’ Where did that one come from?

Let’s review the two groups.

1. Self-employed taxpayers

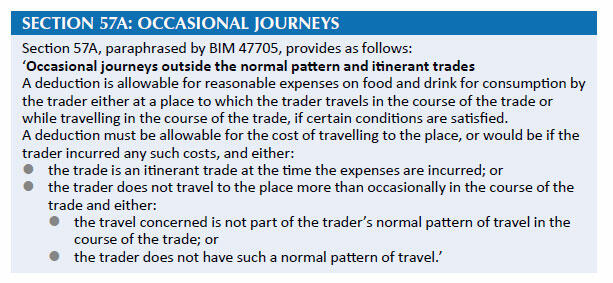

The legislation is a bit sparse, but it is powerful: ITTOIA 2005 s 57A (see box 1).

Just to be clear, this provision was introduced in 2009 at the same time that the benchmark scale rates for employment were introduced into ITEPA 2003 (see below).

The provisions effectively replaced the longstanding decision in Caillebotte v Quinn [1975] 50 TC 222), where food on the go was held to offend the ‘wholly and exclusively’ provisions, now in ITTOIA 2005 s 34.

But what does s 57A mean?

The first and obvious point is that the legislation only allows ‘reasonable expenses on food and drink for consumption by the trader’, so HMRC is unwilling to allow gluttonous excess (although gluttonous excess may be in order). We could spend all night debating the meaning of the word ‘reasonable’, but the clear message from the legislation and the guidance is that food and drink are allowable.

In practical terms, I would personally be comfortable defending a taxpayer’s three course meal and a bottle of wine, say. How do I feel about a second bottle? I’m beginning to wince! This feels less reasonable (and I’m beginning to worry about liver problems…).

The second point, which is worth underlining, is that the section confirms the relationship between travel and subsistence: that if the travel is good to go for tax relief, the food and drink are also good to go.

The third point is that the phrase ‘whilst travelling in the course of the trade’ allows us to conclude that, for example, a self-employed tax adviser, travelling to see a client will be allowed to claim tax relief on food and drink on the go. But note that this is qualified by the use of the word ‘occasionally’. If you went to see the same client every week, then food and drink on the go would arguably not be allowed.

The fourth point, to my eye, is that if the taxpayer has an ‘itinerant trade’, then that is a good place to be as far as tax relief on subsistence is concerned.

The leading case on an itinerant trade for a self-employed taxpayer is Horton v Young [1971] 47 TC 60.

This is what BIM 37620 says about travel costs for an itinerant trader:

‘Where an “itinerant” trader’s base of operations is at their residence, you should allow the costs of travelling between the residence and the sites at which the trader works. An itinerant trader is one who travels from their home to a number of different locations for the purely temporary purpose at each such place of their completing a job of work, at the conclusion of which they attend at a different location. A typical example would be a jobbing builder.’

So, my practical conclusion, within the scope of this article, is that if the travel is good, the subsistence will also be good. As a group, therefore, itinerant traders should be able to claim for the reasonable costs of food and drink on the go.

Overnight subsistence and accommodation expenses

What happens when a taxpayer needs to spend a night or nights away on business? BIM37670 provides an answer:

‘Where a business trip by a trader necessitates one or more nights away from home, the hotel accommodation and reasonable costs of overnight subsistence are deductible. The reasonable costs of meals taken in conjunction with overnight accommodation are allowable, whether or not paid on the same bill.

The same treatment may be extended to traders who do not use hotels, for example, self-employed long distance lorry drivers who spend the night in their cabs rather than take overnight accommodation.’

The landscape is much more uncertain where taxpayers spend longer periods away from home on business; for example, a contractor who spends three months away on a contract. Cases such as Prior v Saunders [1993] 66 TC 210 (involving a self-employed sub-contractor away for several months at a time) do not readily assist us for subsistence, as they are pre s 57A cases and were decided on the Caillebotte v Quinn principle.

Case law does, however, address extreme examples. In Hanlin v HMRC [2011] UKFTT 213 (TC), the taxpayer claimed, inter alia, overnight accommodation costs of £4,800 for staying in Dungeness during the week (48 weeks, four nights each week, £25 per night) while maintaining a home in Coventry. The taxpayer had been working on a particular contract in Dungeness for some seven or eight years. Not surprisingly, the FTT found that the accommodation expenses were not deductible. The taxpayer had chosen to live away from his base of operation.

The conclusion that I draw here is that costs for food on the go (as well as accommodation and travel) are allowable until such times as the works makes a fresh base of operation. How long? Sadly, the legislation and the decided cases do not allow us to make a sharp distinction, but HMRC in BIM37675 gives us some guidance:

‘The position is rather different where a subcontractor works at one or a very small number of different sites during the year. In such a case, it may be that the premises where the taxpayer carries on the business are, in fact, the business base. If this is so, the cost of travelling between the taxpayer’s home and the business base should be disallowed.

‘Following the decision in Horton v Young [1971] 47 TC 60, where a subcontractor works at two or more different sites during a year, travelling expenses between the taxpayer’s home and those sites should normally be allowed.

‘However, where the subcontractor works at a single site in the year and this is the normal pattern for the business, travelling expenditure (and hence subsistence costs) between the subcontractor’s home and the single site should only be allowed if the home is, in some real sense, the centre or base of the business. That will depend on the facts of the case and specifically what business activities are carried out at home.’

Would you like a patch test, sir?

Horton v Young is also useful for addressing the area worker (otherwise known as a patch worker). If a worker has an area – for example, a chimney sweep, a window cleaner or a milkman – then the ITTOIA 2005 s 34 test (wholly and exclusively) will block the travel from his home to the edge of his patch. By inference, if the travel is not deductible until the worker reaches the patch, then the subsistence will also be disallowed (see BIM37620).

2. Employed taxpayers

Let’s now look at our second group – employed taxpayers. Most employees will be reimbursed for actual travel and subsistence costs incurred. In this scenario, the employee will want to know if the payments received are taxable. If the reimbursed payments are within the scope of the rules, then no tax or NICs will be due.

If the employer won’t reimburse the cost, the employee can make a claim to reduce their earnings and this is likely to lead to a tax rebate.

The legislation for travel expenses for employed taxpayers is in ITEPA 2003 s 337 et seq. and is covered extensively in HMRC Booklet 490.

The well-known fault line for employees is between a permanent workplace and a temporary workplace. Broadly, the test of a temporary workplace is whether the employee has spent, or is likely to spend, more than 40% of their working time at a particular workplace over a period that lasts or is likely to last no more than 24 months. It is worth mentioning that the 40% rule is not in the legislation, but is only in the guidance.

In the Subsistence section (5.4) of Booklet 490, it says:

‘Travel expenses includes both the actual costs of travel together with any subsistence expenditure and other associated costs that are incurred in making the journey. This includes:

- any necessary subsistence costs incurred in the course of the journey;

- the cost of meals necessarily purchased whilst an employee is at a temporary workplace; and

- the cost of the accommodation and any necessary meals where an overnight stay is needed

– this will be the case even where the employee stays away for some time.’ [italics mine]

HMRC gives an example in this same section:

‘Michael is employed as a travelling salesman visiting customers across the UK throughout the day. He travels to his first customer direct from home and travels home directly from his last customer of the day. Each day he purchases and eats lunch whilst travelling between customers. Michael is travelling in the performance of his duties. Therefore, the costs of his travel both to and from home and between customers together with the cost of his meals incurred whilst en route will be allowable.’

In my view, the rules for employees on staying away for extended periods, are clearer than for self-employed taxpayers.

Booklet 490 gives the following example:

‘Chris is required to spend three months working at the site of one of his employer’s clients. He travels to the site each Monday morning, stays in a hotel close to the temporary workplace and travels home late each Friday evening, eating dinner on the way. During the week he takes some of his meals in the hotel and others at a nearby restaurant. The cost of the accommodation and all the meals are part of the cost of his business travel.’

But what about food on the go for employees on shift; say, an ambulance driver or a policeman? Sadly and not surprisingly, there are no tax reliefs for shift workers on the go.

Reimbursed expenses

I want to finish this brief review by considering the reimbursement issue by employers.

The basic shape of this is that an employer will reimburse expenses (if they wish to do so), in one of three ways:

- reimbursing actual qualifying expenses (including subsistence);

- paying on the benchmark scale rates for subsistence under the Income Tax (Approved Expenses) Regulations 2016 (SI 2015/1948); and

- paying on a bespoke and agreed scale rate (not considered here).

The benchmark scale rates are a way for employers to pay on a published rate for subsistence expenses. Payments within the rates are not reportable on P11Ds and are not taxable or subject to national insurance. Excess payments are reportable and they are taxable and subject to national insurance as earnings. Employees have to actually spend the amount and employers will need to check that the qualifying travel has actually taken place.

The current HMRC benchmark scale rates are: £5 for qualifying travel of 5 hours or more; £10 for qualifying travel of 10 hours or more; and £25 for qualifying travel of 15 hours or more.

Note that the over 15 hour rate for subsistence will almost always apply where an employee is required to stay away overnight, provided the cost of any meals is not also included in an accommodation payment. This £25 rate applies when an employee is still out at 8pm.

Conclusion

The issue of tax deductibility for travel and subsistence costs is not going away and as advisers, we need to be able to carefully and accurately tease the strands of clients’ questions apart, to be able to give them accurate advice.