The journey towards zero

Share this article

Colin Smith examines how the journey toward net zero greenhouse gas emissions will impact tax

Key Points

What is the issue?

The net zero agenda will impact tax laws and incentives, business operating models, and transparency and reporting. These in turn will impact tax teams and tax advisers.

What does it mean for me?

The tax implications and opportunities throughout the business lifecycle of any new operating model should be considered. Different tax considerations may be relevant at the development, construction, operation and decommissioning phases of a renewable energy project.

What can I take away?

Tax teams and their advisers will need to understand the relevant tax issues throughout the business lifecycle, and develop appropriate processes to manage, measure and explain them.

The net zero agenda is accelerating. A growing number of countries, investors, asset managers and businesses have committed to net zero greenhouse gas or carbon dioxide emissions goals.

Almost all countries have ratified the Paris Agreement and more than 110 have pledged to be carbon neutral by 2050. Governments are developing policies to achieve these goals, albeit some at a high level. In November 2020, the UK government announced its ‘Ten point plan for a green industrial revolution’ (see bit.ly/3dECfuT) and issued an Energy White Paper in December. The EU has its Green Deal (see bit.ly/3bCajp0) and Germany’s Energiewende plans include a €9 billion hydrogen strategy. Joe Biden’s plan for a ‘clean energy revolution’ was a key part of his presidential campaign. The US rejoined the Paris Agreement on President Biden’s first day in office and he has appointed a pro-environment treasury secretary.

Many investors and asset managers have made net zero pledges, public statements or signed up to cross-industry groups such as the Institutional Investors Group on Climate Change’s Net Zero Asset Managers initiative.

An increasing number of businesses have made net zero commitments, often aiming to achieve that goal significantly before 2050. Businesses are starting to embrace the opportunity to drive innovation, increase competitiveness and stimulate resilient growth on the journey to net zero.

Why is this important to tax teams and tax advisers?

The net zero agenda will impact tax laws and incentives, business operating models, and transparency and reporting. These in turn will impact tax teams and tax advisers.

Tax laws and incentives: Tax and fiscal policy may be used to encourage the transition to net zero. Governments may be tempted to increase the use of environmental taxes to alter behaviours. Further, as HM Treasury’s Net Zero Review Interim report (see bit.ly/3buOyY6 ) noted: ‘The transition to net zero and consequent structural changes in the economy will also have implications for the UK’s public finances and fiscal sustainability.’ As such, there may be tax law changes as a result of the transition to net zero, as well as to encourage it.

Business operating model changes:

The journey to net zero will be different for each business. For some businesses, the transition from producing or using fossil fuel sources of energy to renewable sources will be the main action. For others, the journey to net zero may focus more on the emissions in their supply chains, making energy efficiency improvements in buildings and processes, reducing the emissions associated with business travel or investing in carbon removal projects.

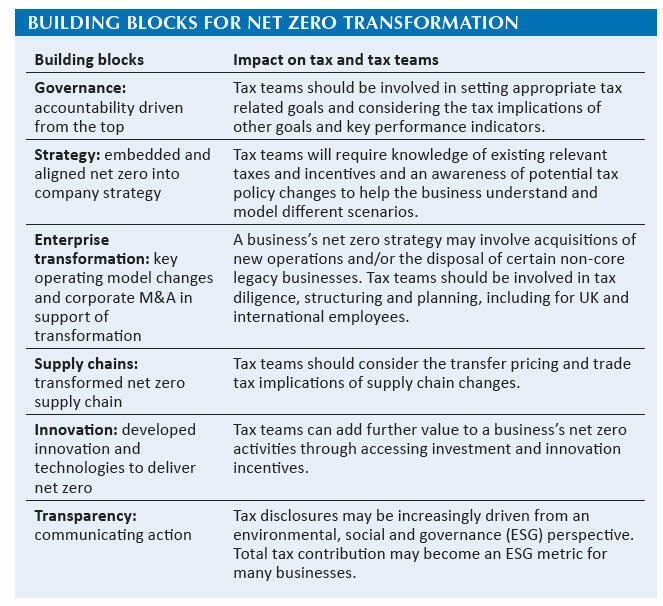

Regardless of the specifics, there are likely to be some consistent building blocks for net zero transformation, such as those highlighted by the Transform to Net Zero initiative (see bit.ly/3bvnmbt). See the box Building blocks for net zero transformation for some of the impacts on tax and tax teams of the actions required to embed net zero aspiration within businesses.

Enterprise transformation: key operating model changes

The tax implications and opportunities throughout the business lifecycle of any new operating model should be considered. As an example, businesses making investments in renewable energy generation should bear in mind that different tax considerations may be relevant at the development, construction, operation and decommissioning phases of a renewable energy project.

Development and construction: Effective UK corporation tax relief for expenditure is generally only available once a company has started to trade. Broadly, a renewable energy business will only start to trade for UK corporation tax purposes once it is generating income. A business in the development or construction phases is likely to be ‘pre-trading’ with no income and therefore no current tax relief for expenses. Designing appropriate processes to monitor and categorise the nature of the development and capital expenses incurred can help to maximise tax relief.

Decommissioning: Decommissioning

is a significant expense for many projects. UK corporation tax relief for decommissioning is generally available only when the costs are incurred – often when the business has little revenue, or indeed has ceased to trade. Where viable commercially, consideration could be given to decommissioning certain assets whilst continuing to operate others.

The new operating model may involve existing assets being used in different ways. For example, UK oil and gas infrastructure may be used for activities such as carbon capture, usage and storage, offshore wind, gas storage, green hydrogen production/storage or floating solar. Tax teams should seek to understand the tax consequences of any change of use of existing assets.

Enterprise transformation: corporate M&A

A business’s net zero strategy may involve acquisitions of new operations and/or the disposal of certain non-core legacy businesses. Some key points on M&A are included below.

Acquisitions: Undertaking tax due diligence will help tax teams and the business to understand the tax issues and risks associated with the new business and its tax attributes. An appropriate acquisition structuring and financing structuring should be implemented, aiming to maximise legitimate tax deductions for any interest costs and to minimise tax leakage on cash extraction from the acquired business.

Land and transaction-based taxes may be relevant, including business specific issues. For example, onshore windfarms typically can consist of an exclusivity agreement followed by a lease, with the developer paying the Crown Estate a rent linked to the power generated. If there is a premium, stamp duty land tax of up to 5% may be payable. As the rent is uncertain:

- the stamp duty land tax on the rent is charged on the best estimate of what the rent will be for five years (2% rate for rent); and

- after five years, when the rent can be ascertained, a revised calculation must be done and further stamp duty land tax paid or refund issued as applicable.

Similar rules apply for solar panels; however, in cases where the landlord has a right to use any of the electricity generated, HMRC has stated that it will treat this as consideration given by the lessee to the landlord and therefore liable to stamp duty land tax.

Disposals: Many disposals are exempt from UK corporation tax. However, renewable energy generation projects often involve minority interests and ‘joint venture of joint venture’ structures, which can mean that the substantial shareholding exemption is not available. The vendor should ensure that its tax affairs are in order and that the team

has a good understanding of relevant tax attributes and risks; in some cases, it may be appropriate to consider vendor due diligence.

Enterprise transformation: capital investments

Many net zero transition activities will involve capital expenditure. The availability of tax deductions can influence the financial viability of a project. Ideally, the correct capital allowance rates should be taken into account when modelling expected financial returns. Temporary super deductions of up to 130% for capital expenditure were announced in the Budget. Even the normal UK capital allowance rates vary significantly from 100% to 3%, with 150% for qualifying expenditure on removing pollutants from derelict or contaminated land.

In the context of the UK government’s ambition to achieve net zero by 2050, it is perhaps odd that solar panels are specifically defined as falling within the less generous long life assets category and that 100% capital allowances for certain environmentally beneficial plant and machinery and certain energy-saving plant and machinery were abolished from April 2020. Perhaps this is an area of tax policy that the government may reconsider.

Some capital allowances depend on the company having an interest in the land to which the machinery is fixed, at the time the machinery is fixed to the ground. It is therefore important that tax teams ensure that relevant contracts are signed at the right time, in the right order and by the right parties.

Supply chains

The actions required to achieve net zero are likely to affect each business’s global operations and so are likely to have significant transfer pricing consequences.

At the start of a business’s net zero journey, relevant expertise and resources are likely to be scarce and centralised within the group. The pricing of new, innovative services may be at risk of greater challenge by tax authorities. Early consideration of the transfer pricing is important.

As businesses consider entry into new markets, they are likely to transfer assets and make intra-group payments. As shown by the ongoing Ørsted tax case in Denmark, the design and operation of a new business model (in that case relating to UK offshore wind farms of a Danish group) can have material tax risks, potentially affecting the economic return. Different trade taxes such as customs duties may apply to the net zero aligned business supply chains.

Innovation

Whether it is efficiency improvements in photovoltaic solar panels, the computer systems behind energy-as-a-service or carbon capture, usage and storage, many net zero transition activities will result in businesses developing innovative technology, products or services. Many jurisdictions’ investment and innovation incentives are administered through the tax systems. For example, the UK’s incentives include the following:

Research and development (R&D) tax credits: The R&D super-deduction available to SMEs is now 230% with the cash back available to loss making SMEs. The government has made the large company regime more generous by introducing the research and development expenditure credit (RDEC) of 13% of qualifying expenditure. RDEC allows larger companies to recognise the benefit of their R&D claim effectively as a grant, as opposed to within the tax line, which helps add visibility from an accounting perspective.

Patent box: The UK’s patent box regime provides an effective corporation tax rate of 10% tax rate on profits relating to the exploitation of intellectual property. The regime was modified in 2016 to limit benefits based on the proportion of relevant UK R&D undertaken as a proportion of global R&D.

Grants: The UK government offers both traditional grant funding and repayable funding schemes that can provide cash upfront with favourable repayment and interest terms to help unlock cash flow. Net zero aligned financial support includes national programmes such as:

- Innovate UK (for which ‘clean growth’ is one of the Industrial Strategy’s grand challenge areas);

- the Industrial Energy Transformation Fund, which supports the development and deployment of technologies that enable businesses with high energy use to transition to a low carbon future;

- the Carbon Capture and Storage Infrastructure Fund;

- the Net Zero Hydrogen Fund; and

- the Energy Entrepreneurs Fund, a competitive funding scheme to support the development of technologies, products and processes in energy efficiency, power generation and storage.

There are also smaller, regional programmes such as various energy efficiency grants, low carbon innovation funds, and grants to support the development of products and services that reduce carbon usage and emissions.

Tax teams should ensure that their businesses are benefiting from the full range of reliefs and credits available, including an international perspective.

What might happen next?

Countries will issue more detailed plans on their net zero strategies, which will stimulate more investment by businesses.

More businesses will announce net zero pledges and those businesses will increasingly start taking action to achieve those pledges by:

- focusing more on the use of water and emissions in their supply chains;

- making energy efficiency improvements to buildings and processes;

- reducing the emissions associated with business travel; and

- investing in nature-based carbon removal projects.

There will be greater use of taxes and incentives that support the journey to net zero – and environmental, social and governance (ESG) goals more broadly – such as carbon taxes and the UK’s plastic packaging tax which will apply from April 2021 (see ‘The changing tax environment’, Tax Adviser, January 2021).

On 17 February 2021, the House of Commons Environmental Audit Committee stated that the Chancellor should use the Budget as a springboard to kickstart the green industrial revolution (see bit.ly/3pSjwP6). It suggested specific policies, including reducing the rates of VAT on repair services and products containing reused or recycled materials and a VAT reduction on home upgrades to incentivise the installation of low-carbon domestic technologies and improve energy efficiency of homes.

Despite this, the Budget contained very few new tax or spending announcements relating to net zero or the energy transition.

A move towards a single standard on ESG disclosures may include total tax contribution, especially following the publication in September 2020 of the International Business Council of the World Economic Forum’s white paper (see bit.ly/3khnwaI) designed to establish consistency and comparability for companies reporting on their ESG performance. The white paper included 21 core ESG metrics and disclosures, including total tax paid.

Summary

The transition to a net zero greenhouse gas environment is starting and is likely to involve significant business change, which will almost certainly have tax consequences. Tax teams and their advisers will need to understand the relevant tax issues throughout the business lifecycle, and develop appropriate processes to manage, measure and explain them.