Business or non-business?

Share this article

That is the question… Neil Warren considers the importance of ensuring that a genuine business is in place before VAT registration is applied for or input tax is claimed on expenses

Key Points

What is the issue?

Deciding if a source of income is ‘business’ or ‘non-business’ could determine if a business or organisation is either able to register for VAT on a voluntary basis or, in many cases, must register on a compulsory basis. The article considers the Lord Fisher tests which help this process.

What does it mean to me?

Input tax can only be claimed on expenses if firstly they relate to a business activity, and secondly they relate to taxable sales. This issue is particularly important if only zero-rated sales are being made; i.e. where repayment VAT returns will be submitted each period.

What can I take away?

In most cases, it will be clear if business supplies are being made. This outcome often depends on the motives and intentions of the owner. But in cases of doubt (e.g. charities), it is worth consulting HMRC’s policy manuals for more guidance.

Why is it important to be clear about what is a business activity? The reason is that because as far as VAT is concerned, if a source of income is non-business, then it cannot be subject to output tax (VATA 1994 s 4). And if an expense is not for the purpose of a business, then input tax cannot be claimed (VATA 1994 s 24).

In this article, I will analyse the key issues to consider on the business or non-business questi on, including a review of two recent tribunal cases, both lost by the taxpayer.

A one-off sale can be business

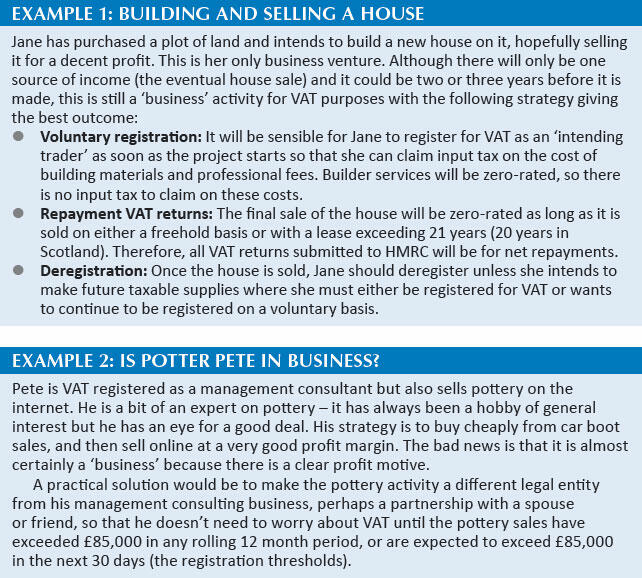

The legislation gives guidance about ‘what is a business’. For example, VATA 1994 s 94 confirms that it includes any ‘trade, profession or vacation’, as well as the supply of facilities or advantages provided by a ‘club, association or organisation’ for the payment of a subscription or other monies. But a business can also apply to a one-off project or deal. See Example 1: Building and selling a house.

Lord Fisher case: six business tests

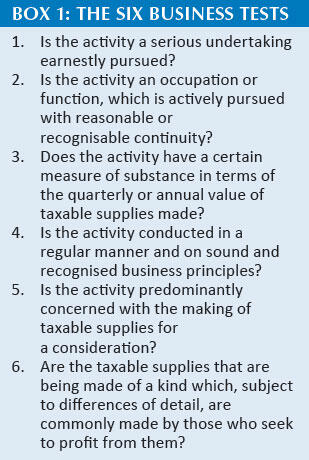

VAT enthusiasts will be familiar with the historic tribunal case of Lord Fisher [1981] STC 238, which has stood the test of time. The case considered if certain activities on Lord Fisher’s estate qualified as ‘business’; e.g. farming shoots organised between a group of friends where fees were collected from the participants. The case led to six key questions being asked in order to determine if a business is evident. See Box 1: The six business tests.

The approach with the six tests is that you must not expect all six to be passed in order to tick the business box; they are not a checklist. For example, in Example 1 which addresses Jane’s house sale, regular quarterly or annual supplies are not being made so it would fail the third test. It is a case of standing back and looking at the bigger picture as to whether a business is in place. See Example 2: Is Potter Pete in business?

Case law: church social club

An example of how things can go wrong was highlighted in the recent First-tier Tribunal (FTT) case of Marites Salabit [2019] UKFTT 675, when HMRC decided that Ms Salabit was in business on her own account, operati ng the social club at St Pius X Roman Catholic Church.

The turnover from bar sales exceeded the registration threshold and she was liable to register for VAT between April 2014 and December 2015, with net VAT owed of £10,617. In her opinion, she was doing the church a favour (she and her mother were both involved as active members) and she was not running a business. However, the deciding factor was that Ms Salabit signed and agreed a contract with the church in February 2013, with the following terms and conditions:

- She paid rent of £625 per week to the church. This was a fixed cost and payable irrespective of how much money the bar took. (Note that the rent was subsequently reduced to £500 per week because the bar was not profitable.)

- She was also responsible for staff costs and paying suppliers, as well as rates and insurance overheads.

- She could retain any profi ts herself and bar takings were banked into her personal bank account rather than any church account.

The basis of Ms Salabit’s appeal was that she was a ‘manager of the social club’ and not running a business. Her accountant argued that the church should have been registered instead. However, the commercial arrangements and contract clearly showed that she was in business on her own account and liable to register for VAT. The appeal was dismissed.

Case law: input tax on a farm

The case of Potter Pete in Example 2 highlighted when and why a taxpayer would argue against being in business. So as to balance the books, I will now consider a case where the taxpayer argued that his company was making business (taxable) sales and was therefore entitled to claim input tax but HMRC disagreed.

In Babylon Farm Ltd [2019] UKFTT 562, the taxpayer registered for VAT in 2014 and claimed input tax of £19,765 in the three years up to 2017, with no output tax declared in this period. The only income earned by the company, apart from an exempt property sale (a capital disposal), was about £500 each year for selling hay to a connected business (hay sales being zero-rated).

HMRC disallowed all input tax on the basis that there was ‘a negligible level of substance to the business activity’ and it was ‘not conducted on sound and recognisable business principles’. The input tax claims mainly related to the construction of a new barn, supposedly used to store the equipment and machinery used to make the hay. However, the reality is that a commercially driven business would not spend £100,000 in order to earn an annual income of £500 – it would take 200 years to recover the outlay.

The tribunal considered the Lord Fisher tests and agreed with HMRC that the company was ‘not predominantly concerned with the making of taxable supplies for consideration’. The appeal was dismissed.

Charities

One of the most controversial aspects of VAT can oft en be about whether a charity is making business supplies or otherwise. The argument is often clouded by the fact that charges for certain supplies of goods or services are often made by a charity at a rate that is below market value.

It is a well-accepted fact that a business arrangement does not necessarily involve making a profit, as the Salabit case showed. And in most cases, the charging of a fee by a charity means that business supplies are being made.

For more guidance, it is worth consulting HMRC’s internal policy manual for charities and the series of notes in the VCHAR3000 series. There is also a separate HMRC manual for Business/Non-business issues, with the reference series here starting at VBNB10000.

Final thoughts

I was chatting to an accountant recently who said that it was very unfair that a sole trader registered for VAT has to account for output tax on all income earned in his own name if the income is VATable. This is partly true – a sole trader must account for VAT on all ‘business income’ earned in his own name. For example, if a VAT registered builder has an interest in historic stamps, and buys and sells stamps as part of his hobby, the stamp sales would not be business income subject to VAT. But if he retired as a builder, and became a full-time stamp trader, the goalposts could move.

In summary, when it comes to looking at whether an arrangement is business or non-business, there is no clear cut answer and it is often a case of weighing up all of the relevant facts to arrive at a sensible outcome. And needless to say, HMRC will sometimes disagree with our conclusions.