Business rates reform: new compliance obligations

Share this article

Business rates tax is about to undergo significant changes. We examine how ratepayers in England can prepare for the proposed developments.

Key Points

What is the issue?

Business rates tax and the framework surrounding it are about to undergo a seismic amount of change on a scale not seen before. Changes are due to be introduced largely through the Non‑Domestic Rating Bill 2023 and other open consultations yet to conclude.

What does it mean to me?

Ratepayers need to understand new compliance obligations, alongside key framework changes which impact how they can effectively review and challenge business rates tax liabilities to ensure cost effectiveness.

What can I take away?

Those that invest the time to understand the road map for change will be able to best ensure they are challenging liabilities effectively and are adhering to tax compliant duties timely and effectively.

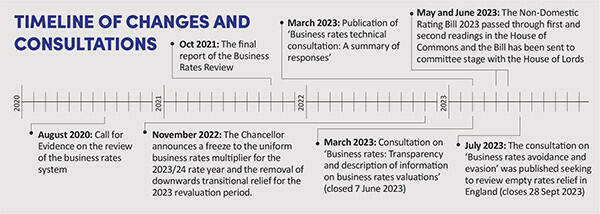

Business rates and the system and policy surrounding it are about to undergo changes on a scale not seen before. Since 2020, business rates have been a topic of constant discussion, with the 2020 Call for Evidence and subsequent Business Rates Review (see tinyurl.com/yc37eadj) seeking to establish whether the tax on occupation of commercial property was still ‘fit for purpose’.

According to the review, business rates are most certainly here to stay. It concluded that a tax on the use and value of commercial property is an important part of a balanced tax system, alongside taxes on profit and consumption. The review went on to recommend key changes that should be implemented to improve the system and the framework for the tax. These vast changes will significantly alter the system as we know it.

The present Non-Domestic Rating Bill 2023 making its way through Parliament will implement many of the changes set out in the findings. Further change will come from parallel open consultations, notably the ‘Business rates avoidance and evasion’ consultation published on 6 July 2023.

As it becomes harder to raise debt to fund property investment, it is going to be key for investors to understand the costs they will face from day one of investment, as well as the challenges there may be in securing empty rates relief. The tightening of the rules around applying for empty rates relief will place an additional burden on ratepayers in an increasingly tough economic market.

Much of the proposed change remains ‘under the radar’ for ratepayers in England. There has been limited communications to date on the changes, leaving many businesses unaware and lacking knowledge on how to plan for its implementation.

This article seeks to highlight the changes and how businesses can understand and prepare for what is coming. The main changes in the Non-Domestic Rating Bill 2023 are set out below.

Shortening the revaluation period

Business rates reflect an opinion of rental value of commercial property at a snapshot in time known as the antecedent valuation date (AVD). Historically, the tax has been reset against a new market rental valuation date every five years. Towards the end of each five-year period, there is inevitably greater disconnection between a property’s current rental value and that pegged to the AVD. More frequent revaluations should, in theory, ensure that tax assessments across all commercial property sectors align more closely with the reality of the rental market and economic climate, limiting the scope for disparity. Increased frequency may be a benefit to those occupying property in secondary and tertiary locations. However, it will be less welcome news for those occupying commercial property in prime sector and market locations.

The new compliance regime

To support the greater frequency of the revaluations, new compliance obligations will be introduced. Three key obligations will be placed upon the ratepayer.

Notifications to the VOA

The first two obligations involve notifications to the Valuation Office Agency (VOA):

- a duty to notify the VOA of notifiable events in real time (i.e. within 60 days of the event): broadly speaking, this involves any changes to the property, tenancy or usage that affect rental value, or trade information if the property is valued on a receipts and expenditure basis; and

- an annual duty to notify the VOA that all data held is correct within 60 days of 1 April each year. The notification must be made via an online platform.

There will be penalties for failure to comply within the timeframe or for the provision of false data:

- False data offences carry a maximum penalty of 3% of rateable value plus £500. The new VOA information duty also includes criminal sanctions where false information has been knowingly or recklessly provided.

- Failing to comply with the penalty notice within 30 days of service could result in a maximum penalty of the greater of 2% of rateable value and £900, plus £60 per day.

Notifications to HMRC

Taxpayers also are also obliged to provide their taxpayer’s unique reference number to HMRC on becoming a ratepayer of a property for the first time, using a new online platform. (This adheres to the new digitalising business rates agenda.)

The taxpayer reference notification must be made within 60 days of becoming liable for rates on a property. Failure to make the notification in the time scale or giving incorrect tax reference numbers will hold penalties of £100 for a failure to notify and up to £3,000 for false data. If the ratepayer fails to comply with the penalty notice, there will be an additional fine of £60 per day capped at £1,800.

Ramifications for ratepayers

There are numerous implications for ratepayers. The first is to understand that this new compliance obligation is compulsory and that there are penalties for both delays and the provision of false data, given unwittingly or not.

Organisations need to start familiarising themselves with who will be responsible for compliance with these new requirements. Business rates are often left to in-house property or facilities teams, and often treated differently from other business tax compliance tasks within the organisation.

The intention is that the compliance regime will accommodate large bulk transfers of data. However, at this stage nothing has been confirmed and ratepayers must begin preparing for the possibility that they may have to undertake these tasks on a property by property basis. This would be a sizeable task for ratepayers occupying or owning vast property portfolios.

At present, it is the desire of the VOA and HMRC to have one single online platform for the proposed new duties and to challenge assessments. However, this is yet to be unveiled. Ratepayers need to be aware of the possibility that there could be multiple online platforms for these functions.

Ratepayers need to think about organising their data. It is key to have an internal awareness of what is required at any given moment throughout the rate year – tracking when the business is liable; providing notifications within the timescale; and ensuring data can be transferred on time and in the right format. The onus will be on the ratepayer to take reasonable steps to familiarise themselves with their new obligations and the platform or platforms on which to complete and transfer the data.

The new duties are expected to improve the quantity and quality of the rental data that the VOA can utilise to compile valuations. This should also streamline the process of setting the tax and challenging it in the longer term.

Introduction of new reliefs

There will also be an introduction of business rates reliefs. For ratepayers looking to invest and make improvements to properties they occupy, a new improvement rate relief will be available from 1 April 2024. This is targeted at light programmes of improvement and not major redevelopments.

The programme of works must be ‘qualifying works’ and the ratepayer must remain in situ throughout the period of the improvement. The result must be improved rateable value. Under the relief, no increase in value will be attributed to the property for 12 months following completion of the works. The improvement relief will run to 2028, when it will be reviewed again.

On 1 April 2022, the Chancellor introduced a 100% exemption until 31 March 2035 for eligible plant and machinery used in on-site renewable energy generation, such as electric vehicle charging points, solar panels, and battery storage used with renewables. In addition to this, 100% heat network rate relief for low carbon heat networks that have their own rates bills, effective from 1 April 2024. The Non-Domestic Rating Bill 2023 also allows the government and Welsh government to deliver this.

Improved transparency and data gateway sharing

The Business Rates Review also highlighted the need for greater ratepayer understanding of the compilation of the business rates assessments and the values utilised. This has led to a two-phased approach, which is due to be implemented:

- Phase 1 will ensure that there is greater access online to information on the valuation methods used.

- Phase 2 is to provide access to the comparable data utilised.

Only ratepayers who have complied with the new obligations to notify will be able to request the rental analysis the VOA have utilised to compile the business rates assessment. The request for data is made independently from and made prior to a business rates challenge on the 2026 revaluation.

The recent consultation on ‘Business rates: transparency and disclosure of data’ highlights the need to protect sensitive rental data and landlord and tenant agreements. Concerns have been raised by landlords in particular about the sensitivity of the rental evidence information requested and shared.

The new system will ringfence data requests to ratepayers and rating agents. It will also omit any further data around incentives and turnover arrangements. The proposed layout of the provided evidence analysis still fails to provide information on challenges received on comparable properties. This lack of data overlooks the principle of ‘tone of the list’ when challenges to and agreements on comparable properties begin to take precedence over the rents nearest the AVD.

Although a step in the right direction, flaws remain in the intended provision of comparable evidence data by the VOA as set out in the recent business rates: transparency and disclosure of information on business rates consultation. For the ratepayer to truly understand the fair composition of the tax assessment, they need to know more factors involved in the rental analysis, the incentives or uplifts attributable, and the basis on which the rents have been analysed. More information shared at the pre-challenge stage would reduce the need for ratepayers to make a challenge to obtain data. The consultation findings are yet to be disclosed.

Tightening the scope for securing disturbance allowances

Raising a challenge to secure an end allowance for a disturbance or a market event is known as a material change in circumstance challenge. Following the review of the impact of Covid and the subsequent legislative change, the scope of what qualifies for a material change in circumstance will now be tightened. Major market events will be factored into the revaluations instead of providing an opportunity to lodge a challenge on the basis of a material change in circumstance.

Improvements to the uniform business rate multiplier

The uniform business rate (UBR) multiplier will now be pegged to CPI inflation instead of RPI and the new multiplier will not have to be set or announced for the preceding year until February.

The Chancellor took the decision at the Autumn budget 2022 to freeze the uniform business rates multiplier for the 2023/24 rate year. This seeks to support the ratepayer keeping the multiplier capped to 49.9p for properties with rateable values to £50,999 and 51.2p for properties with £51,000 or more rateable value. Despite the freeze the multiplier is still very high and ultimately dictates a high level of rates payable. Ratepayers should remain aware and mindful that the rate at which liability is heavily linked to this rate which tracks CPI inflation.

Billing authorities and discretionary rate relief

The Non-Domestic Rating Bill 2023 also seeks to allow billing authorities the ability to retrospectively award discretionary rate relief at any time.

The current position is that they will be precluded from doing so for six months after the close of each financial year. In reality, this has meant that many ratepayers who delayed seeking discretionary relief missed out on savings. This was common with the retail rate relief discount schemes and covid assistance relief funds.

This change is really positive for both the ratepayer and the billing authority ensuring reliefs are given to those most in need and are there to support the ratepayer. Ratepayers who are eligible for reliefs should look to pursue them at the first opportunity but will not be penalised if they fail to.

Reforming empty property rates relief

Another finding from the 2020 Business Rate Review was that empty property rates relief was not working as intended in England, with many ratepayers seemingly abusing the empty property rates relief scheme. Consequently, the publication of the ‘Business rates avoidance and evasion’ consultation on 6 July 2023 set out the intention to review and amend the six week reset period for making a further application for empty rates relief; and to increase the reset period to three or six months on certain commercial property assets.

The increase in the reset period seeks to disincentivise ratepayers from engaging in avoidance activity. There is also discussion in the consultation about limiting the number of times a property can benefit from empty rates relief, as well as a possible amendment of the Non-Domestic Rating (Unoccupied Property) (England) Regulations 2008 to require 50% of a floor space to be occupied to qualify.

Abuse of the empty rates relief or any discretionary rate relief system will be evident through the new information collected through the compliance obligations. HMRC’s newly collected data will allow it to share data with billing authorities, who can then verify ratepayers’ eligibility for relief schemes.

HMRC will also be able to identify ratepayer breaches where they occupy multiple properties across different billing authorities; and where they may have made a claim for small business rate relief or exceeded the cash caps in respect of the total amount of retail, hospitality and leisure relief being claimed.

It is highly unlikely that limiting the ability to mitigate empty rates will lead to a sudden reoccupation of commercial property. There needs to be a balanced understanding that the tightening of the relief will place additional pressures on businesses against the backdrop of rising interest rates and the cost of living crisis.

Be aware and be ready

The tide of change in business rates represents a seismic shift in the administrative framework of the tax, which includes transferring the onus to provide information onto the ratepayer. Business rates will be brought more into line with the compliance requirements relating to other business taxes. Ratepayers must start thinking now about how they will deliver on their compliance obligations and understand how to track, organise and return data.

More frequent revaluations will hopefully bring greater alignment of the rating assessment to the rental markets, reducing disparity in the figures. The increase in commitment to sharing evidence analysis will also be welcome news to ratepayers and rating agents alike. This will allow the review and challenge of assessments to be fairer for the ratepayer, who currently has limited accessibility to the facts on which the assessment has been compiled. However, only those who comply with new obligations will have the ability to access the evidence analysis.

Those occupying or owning large property portfolios with high vacancy rates need to be mindful of the intended amendments to the empty rates relief scheme, which could culminate in increased void costs and reduced capital value of assets.

With the rising levels of interest rates, increased costs and the shortage of labour in the UK market, it is prudent to keep track of outgoings. Shrewd ratepayers will understand the imminent changes to the system requiring them to undertake new obligations. Timely completion and tracking and sharing of key data will enable them to capitalise on business rates savings effectively and allow them if necessary to challenge future business rates assessments at greater speed and effectiveness.

Businesses need to understand and embrace the changes to maximise saving. Those who can confidently navigate the change will ensure costs are controlled and can feel at ease that they are comfortable and confident that they are paying the right amount in business rates tax.