Changing winds

Share this article

Michael Steed looks at the shifting landscape regarding mental health awareness and asks if there are any discernible trends in tribunal decisions, pressure from the media, or HMRC policy as to what constitutes a ‘reasonable excuse’

Key Points

What’s the issue?

A taxpayer may claim to have a reasonable excuse and HMRC must consider ‘special circumstances’ for the late filing of an SA return.

What does it mean to me?

The legislation may not have kept pace with social awareness of mental health issues.

What can I take away?

That the landscape is not static and that a growing awareness of mental health issues could and should affect attitudes towards reasonable excuse.

FA 2009 Schedule 55, which came into force on 6 April 2011, provides that late filing penalties will automatically apply for late returns for a wide range of taxes and include an SA return under TMA 1970 s 8(1)(a).

In this article, I will examine the legislation and recent tribunal cases relating to what constitutes a ‘reasonable excuse’ and how the ‘special reduction’ provisions in FA 2009 sch 55 Para 16 are applied in respect of SA returns.

I will also examine any discernible trends in what constitutes reasonable excuse and special circumstances over time and how the law might develop as we become more aware of and sympathetic to mental health issues.

I will only be looking at reasonable excuse and special reduction here, but acknowledge that this is part of the wider landscape for Schedule 55 penalties, such as late appeals, whether a human has to make the assessment (Khan Properties Ltd (TC6225)(2018)), or, if a notice to submit a return had not been validly made, whether a Schedule 55 penalty would arise in the first place (D J Wood v HMRC [2018] UKFTT 0074 (TC).

The legislation

The penalties for late-filing of SA returns are imposed by FA 2009 Sch 55. The starting point is paragraph 3 of Schedule 55 which imposes a fixed £100 penalty if a self-assessment return is submitted late. There are progressive penalties when a return is more than three months, more than six months late and more than 12 months late.

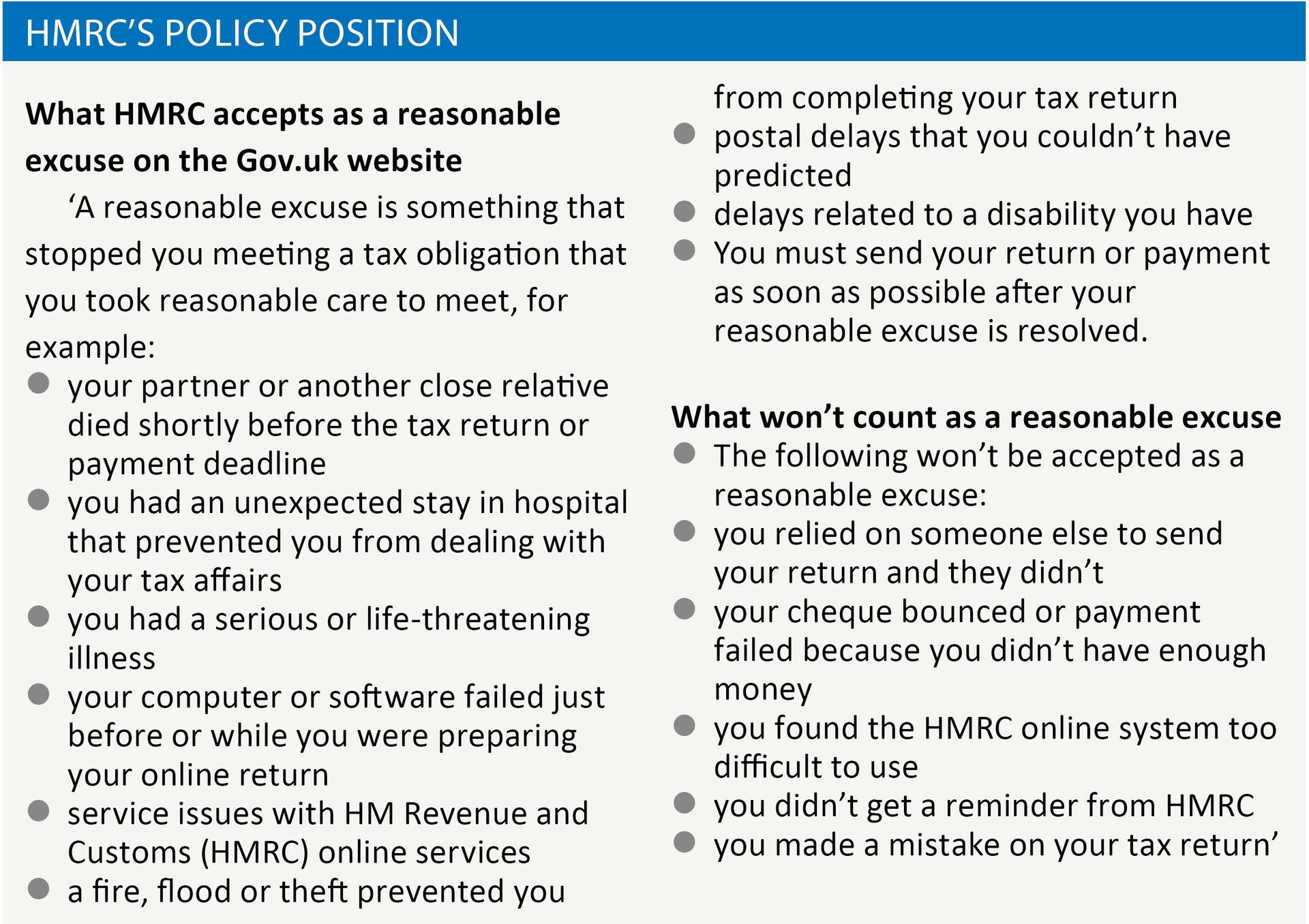

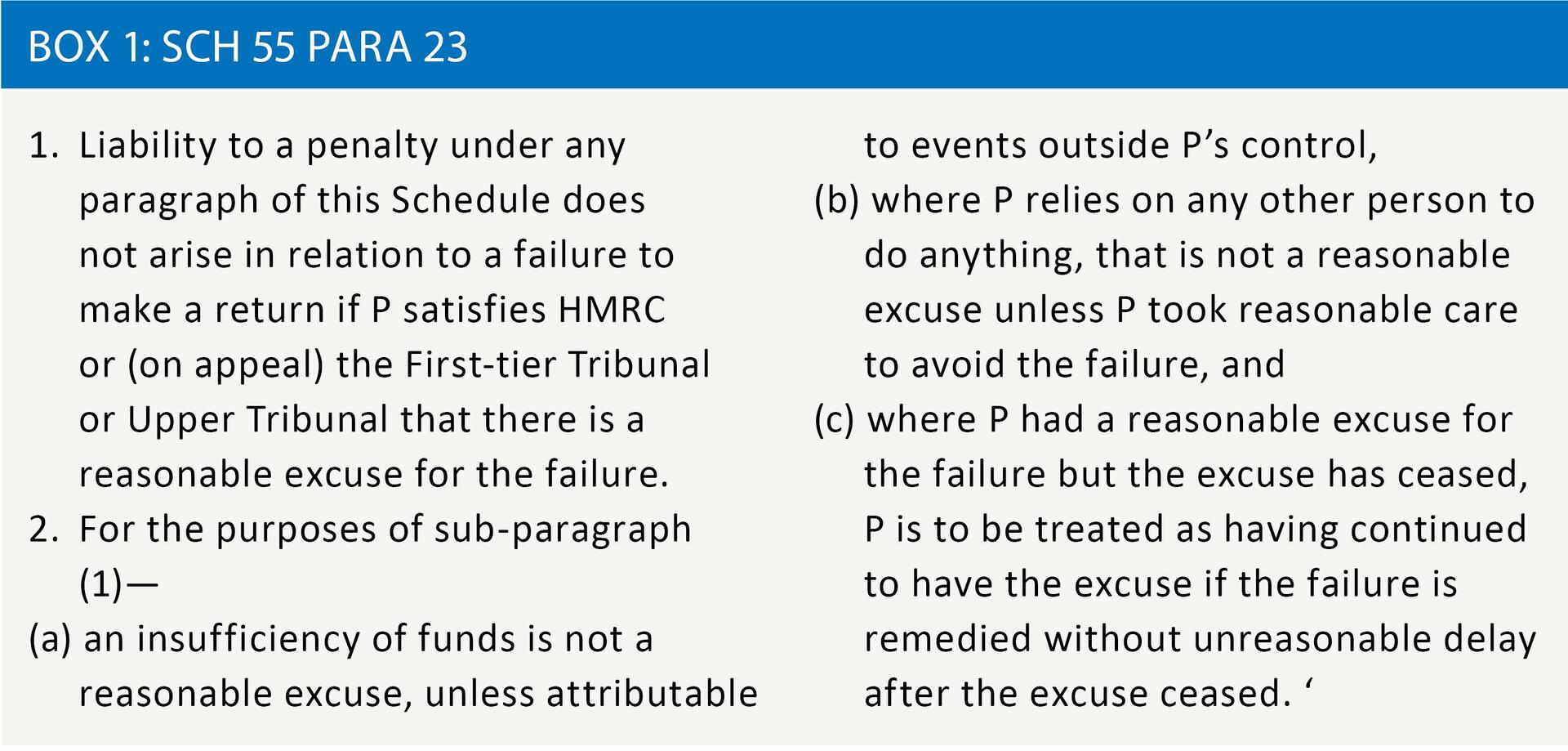

Paragraph 23 of Schedule 55 contains a defence of ‘reasonable excuse’ as shown in box 1.

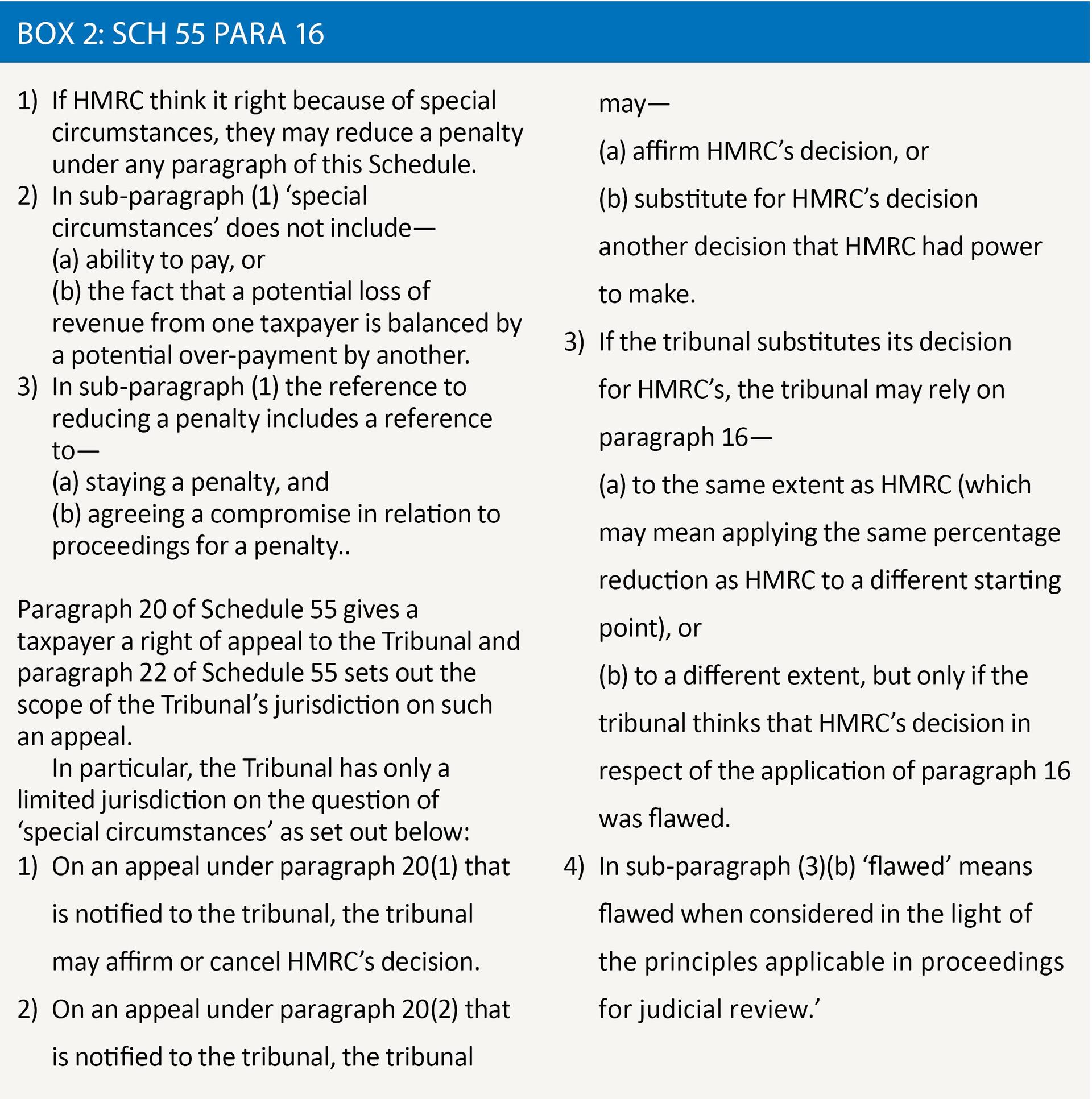

Paragraph 16 of Schedule 55 gives HMRC power to reduce penalties owing to the presence of ‘special circumstances’ as shown in box 2.

How have the courts interpreted a reasonable excuse?

Tribunals have consistently used a VAT case (The Clean Car Co Ltd v C&E Commissioners [1991] VATTR 234) to set out the criteria for a reasonable excuse in direct tax cases:

The judge said: ‘The test of whether or not there is a reasonable excuse is an objective one. In my judgment it is an objective test in this sense. One must ask oneself: was what the taxpayer did a reasonable thing for a responsible trader conscious of and intending to comply with his obligations regarding tax, but having the experience and other relevant attributes of the taxpayer and placed in the situation that the taxpayer found himself at the relevant time, a reasonable thing to do?’

In the First-tier Tribunal case of Nigel Barrett [2015] UKFTT0329 (a case on late filing penalties under the CIS), the Judge held: ‘The test of reasonable excuse involves the application of an impersonal, and objective, legal standard to a particular set of facts and circumstances. The test is to determine what a reasonable taxpayer in the position of the taxpayer would have done in those circumstances, and by reference to that test to determine whether the conduct of the taxpayer can be regarded as conforming to that standard.’

Blame the accountant: some recent cases

The legislation is clear that reliance on another to complete a task does not normally constitute a reasonable excuse. The Tribunals generally consider that where an appellant has appointed an agent to act on his behalf then if that agent for some reason fails in his duties for there to be a reasonable excuse an appellant has to be able to demonstrate that he was diligent in his supervision of the agent he appointed.

You sometimes hear of an accountant’s service that is poor, but this may not be enough to avert a late-filing penalty unless the taxpayer has actively supervised the accountant, or at least contacted HMRC to explain the problem, (and HMRC may have accepted estimated returns (see Christopher Burke Murray [2018] UKFTT 0100 (TC)).

Let’s look at a recent tribunal case where a taxpayer relied on an accountant and the accountant negligently failed to submit the return (Deividas Krzeveckij v HMRC ([2018] UKFTT 0094 (TC)). In this case, HMRC said that where a taxpayer relies on any other person to do anything, that is not a reasonable excuse unless he took reasonable care to avoid the failure.

The Tribunal found that he did place complete reliance on his agent to complete and submit his returns on his behalf. He accepted entirely that he did not have the knowledge or expertise to do this himself and had therefore appointed the agent to do the returns for him.

The taxpayer was relying on his agent as a professional adviser, rather than as a mere functionary, as those terms were distinguished in Elizabeth Mariner v HMRC ([2013] UKFTT 657 (TC)). On the question of whether he had taken reasonable care to avoid the failure, HMRC submitted that, because there had been penalties incurred for late filing in previous years, he should have put appropriate procedures in place to make sure that his obligations in relation to his tax compliance have been met.

The Tribunal accepted that it is not sufficient for a taxpayer simply to appoint an agent and wash his hands of all matters relating to his tax returns.

However, the Tribunal found that the taxpayer had appointed an agent, submitted the necessary information to her in ample time to meet the deadlines and, crucially, contacted her to check that she had received the information and had submitted the return and received confirmation in response that she had submitted the return (by text).

The Judge held that while an exchange of text messages may not be the most common way to deal with an accountant, it was clearly the way in which Mr Krzeveckij corresponded with his agent and it showed sufficient evidence that he had taken reasonable care to avoid the failure to submit the return, so his appeal was allowed.

In Robin MacInnes [2018] UKFTT 0044 (TC), an ice cream salesman who knew nothing about self-assessment instructed an accountant in respect of his affairs and who, despite assurances, didn’t file returns on time. The Tribunal accepted that Mr MacInnes kept contacting the accountant and phoning HMRC, so that was accepted as a reasonable excuse.

Special reduction

In Raul Daniel Garcia [2018] UKFTT 0088 (TC), the taxpayer did not raise an argument relating to ‘special circumstances’. Nonetheless, the Tribunal observed that it must consider whether HMRC should have made a special reduction because of special circumstances within paragraph 16 of Schedule 55.

A special circumstance is generally taken to mean something exceptional, abnormal or unusual. The Tribunal’s jurisdiction in this context is limited by paragraph 22 to circumstances where it considers HMRC’s decision in respect of the application of paragraph 16 was flawed when considered in the light of the principles applicable in judicial review proceedings.

In Garcia it was not apparent from the letters sent or the submissions made that HMRC made any decision at all on special circumstances, which failure was, in itself, a flawed decision.

Where there is such a flawed decision, the Tribunal is able to substitute for HMRC’s decision another decision that HMRC had power to make.

In the Garcia case, the Tribunal nevertheless found that none of the information presented by the taxpayer represented a special circumstance different from the reasonable excuse that the Tribunal had found.

Therefore the decision it substituted was that there were no special circumstances that would give rise to a penalty reduction.

Developments in mental health awareness

Even if a reasonable excuse is established, the taxpayer must file without unreasonable delay once the excuse has ceased. For example, if illness prevented them from filing on time, they must file as soon as reasonably practicable when they recover from their illness.

There have been significant strides in awareness of mental health issues in recent years and this begs the question of whether HMRC would accept mental illness as a reasonable excuse.

Let’s be more specific: suppose you had a long-term mental health issue. Would that constitute a reasonable excuse?

On the basis of HMRC’s stated position that’s a no, on the basis that a reasonable excuse cannot be an enduring issue; it’s something that happens all of a sudden.

But what if a former soldier started to develop PTSD – a common condition? That’s very likely, in my view, to be accepted as a reasonable excuse. Additionally, royal interest in the condition and sustained media coverage has put it in the spotlight. However, it’s much less clear if the condition is chronic but comes in waves.

Would HMRC accept that this would constitute a reasonable excuse on successive occasions? Certainly depression affects different people in different ways and it would arguably be unfair if HMRC were to stand on its traditional position that a reasonable taxpayer would take steps to deal with the issue that gave rise to a reasonable excuse in the first place and this, in my view, is the problem.

Mental health is not like physical health, so a taxpayer’s ability to deal with the issue may of itself be impaired to the point where that person is incapable of making any rational decision for extended periods of time.

But even if HMRC would not accept a reasonable excuse, there is considerable scope in the special reduction provisions which arguably go well beyond the reasonable excuse provisions.

So, for example if HMRC had been told of a taxpayer that needed enhanced support because of mental health issues, then failing to reflect upon this before imposing penalties would be a flawed decision within Para 16 and would allow the Tribunal to consider the circumstances themselves.

Conclusion

Reasonable excuse will not go away. The Tribunal judges deal with scores of cases every year and many of them fall within a predictable pattern. But mental health appears to be a growing problem in our world and our legislation and judiciary will increasingly be called upon to deal with it.