A clean getaway

Share this article

Gary Ashford considers the FA 2017 clauses affecting the cleansing of mixed funds

Key Points

What is the issue?

After a false start by way of the government calling a snap election and the majority of clauses falling out of the Finance Act 2017, we are back with the opportunity to cleanse mixed funds as the clauses are reintroduced in FA 2017.

What does it mean to me?

The opportunity to cleanse mixed funds is a good one. Over the years we have all spent lots of time with clients frustrated of course that, for one reason or another, they are significantly restricted in what they can or can’t do with their offshore funds because they have a mixed fund.

What can I take away?

The hope for this legislation is that it will free up capital and that non-dom resident clients can return to the UK and support the UK economy. Used carefully, the access to new clean capital clearly assists in offsetting some of the challenges of deemed domiciled.

After a false start by way of the government calling a snap election and the majority of clauses falling out of the Finance Act 2017, we are back with the opportunity to cleanse mixed funds as the clauses are reintroduced in Finance Act 2017. HMRC also recently issued its own guidance on the subject.

The cleansing mixed funds clauses provide significant opportunity to those UK resident non-domicile clients who have, for various reasons, found themselves with a mixed fund.

A mixed fund is any account or asset which is made up of any combination of capital, income and/or capital gains. Mixed funds per se are not problematic as long as the UK resident non-domicile does not make any remittances to the UK, or at least appreciates the tax position before doing so. However, where a remittance is made, this can trigger a tax liability and because of the way the rules are constructed (and the Case Law before that). The remittance will be matched firstly against income, then gains etc. on a year by year basis before it can be matched to capital.

With the significant changes to the non-domicile rules introduced in Finance Act 2008, the mixed fund rules were codified. Before 2008, case law provided the guiding principles, with Scottish Provident Institution v Allan 4 TC 409 viewed as one of the leading cases.

The mixed funds rules are such that even if funds are transferred to another offshore account (perhaps before bringing money into the UK), the new account will essentially be made up of the same component parts, to ensure that an offshore transfer prior to remittance to the UK cannot by-pass the rules.

Finance Act 2017

Turning to the legislation, Para 44 Schedule 16 links to the the remittance rules within Part 14 ITA 2007.

Under the remittance rules ITA 2007s 809 Q sets out the rules for transfers from mixed funds.

Paragraph 2 of Para 44 states that s 809R(4) (the current transfers from mixed funds rules) will not apply in certain circumstances. The rules at s 809R(4) state ‘treat an offshore transfer from a mixed fund as containing the appropriate proportion of each kind of income or capital in the fund immediately before the transfer’.

The specific circumstances for ‘switching off’ the composition of a mixed fund rules are as follows:

a. the transfer is made in the tax year 2017/18 or 2018/19;

b the transfer is of money (we will return to this later);

c. the mixed funds from which the transfer is made is an overseas account (‘account A’) and the transaction is made to another overseas account (‘account B’);

d. the transfer is nominated by P;

e. at the time of the nomination, there is no other transfer from A to B; and

f. P is a qualifying individual.

Para 44(3) Schedule 16 sets out the definition of a qualifying individual as follows:

a. they must have claimed the remittance basis in any of the post Finance Act 2008 years up to 2016/17; and

b they were not born in the UK with a UK domicile of origin.

The legislation restricts cleansing of mixed funds to individuals.

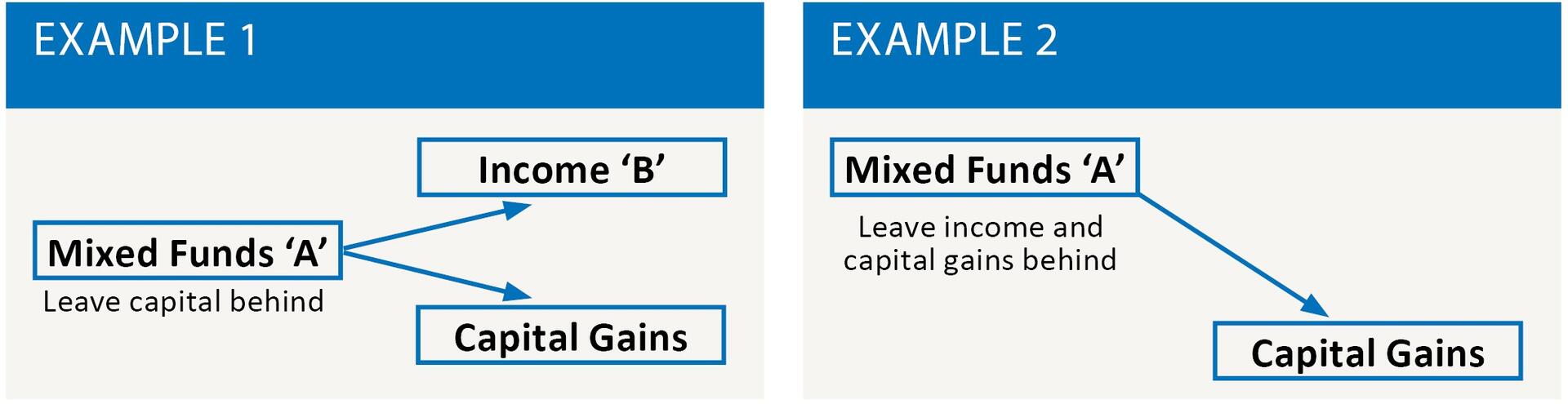

Subparagraphs c) and d) of Para 44(2), states that if you have a mixed fund you can make multiple transfers out of the account into different accounts, but not into the same account. See one possible opportunity in example 1.

There was much discussion before the legislation became final that it was necessary to cleanse in steps, for example moving all income and gains into one new account (say called account B) and then make a new transfer, say of capital gains out of account B into a new account, say called account C, but both the legislation and the HMRC guidance confirm that multiple transfers out into separate accounts at the same time are possible (see example 1).

An alternative approach to transferring the income and capital gains as shown in example 1 is to move clean capital into account B and leave a mixed fund behind in A, See example 2 (although that may have long term implications, as after 6 April 2019, that remaining mixed fund cannot be cleansed).

The legislation states that the transfer must be of money and so any asset that amounts to mixed funds will likely have to be turned into cash before cleansing can take place (the capital gains tax rebasing at Part 3 Para 41 Schedule 16 of the legislation may assist if a disposal is required. (But, it is important to appreciate that rebasing, unlike the cleansing rules, is restricted to those non-doms becoming deemed domicile).

By virtue of the fact that Para 44 Schedule 16 ‘switches off’ s 809R(4), it specifically refers to the remittance rules post 2008. Those who were following the draft legislation will be aware that the legislation set out in the original Finance Bill 2017 (withdrawn prior to the General Election) did not effectively address years before 2008/09.

Mixed Funds pre 2008

Paragraphs 45 and 46 of Schedule 16 specifically include pre 2008.

Paragraph 45 replicates most of the same qualifying criteria as Paragraph 44, but applies to a mixed fund containing pre 6 April 2008 income or expected gains.

Under both Paras 44 and 45, it is very important to make nominations of the proposed transfers (and to keep a record). Invalid nominations (e.g. of amounts greater in proportion, than the amounts available) will invalidate the transfers and will result in the normal mixed funds rules being re-applied.

Para 46b sets out the rules around the composition of the Para 45 (pre 2008) mixed fund.

The first part of Para 46, 46 (2), looks at transactions made before 6 April 2008 from the mixed fund to another overseas account. The second part, Para 46 (6) looks at a transfer made before 6 April and where there is sufficient evidence to determine the composition of the transaction.

Paragraph 46(3) sets out various steps to calculating the component parts of a transfer and of the mixed fund to another overseas account:

a. calculate the total amount of income and chargeable gains in the fund immediately before the transaction (total income and gains); and

b. calculate the proportion of the total that is income and chargeable gain.

Then, if the amount of any transfer does not exceed the total income and gains, it is treated as consisting of income and gains in the proportion of b).

If the amount of transfer exceeds the total income and gains, the transfer consists of:

a. all income and gains in the mixed fund; and

b. any other capital in the fund (up to the amount of the transfer).

Paragraph 46(7) sets out the formula where there is a transfer from another overseas account to the mixed fund and there is insufficient evidence. The basic formula is the same:

a. Calculate the total income and chargeable gains in the overseas account immediately before the transaction (the total income and gains).

b. Calculate which proportion of total income and gains is income or chargeable gains.

However, where there is insufficient evidence to determine which is income or chargeable gains, the rules state those unascertainable amounts should be deemed to be income.

Summary

The opportunity to cleanse mixed funds is a good one. Over the years tax advisers have spent significant time with frustrated clients, explaining where, for one reason or another, those clients are significantly restricted in what they can or can’t do with their offshore funds, because they have a mixed fund.

As the UK faces Brexit, and as non-doms are faced with the new deemed domicile rules, any good news is always welcome. The hope for this legislation is that it will free up capital and that non-dom resident clients can return capital to the UK to support the UK economy. Used carefully, the access to new clean capital clearly assists in offsetting some of the challenges of the new deemed domiciled rules.

Finally, it is also worth reminding ourselves, when embarking on a detailed mixed funds analysis, of the new rules within Schedule 18 of Finance Act 2 (Requirement to correct Certain Offshore Tax non Compliance (RTC). The RTC proposals will require any offshore tax non-compliance existing as at 5 April 2017 to be corrected before 30 September 2018. This would extend to an inadvertent remittance from a mixed fund.

You can read more about RTC...