The complex web of support

Share this article

James Geary gives an overview of the different forms of state aid, including the recent Covid-19 support measures, and how these different forms of state aid interact

Key Points

What is the issue?

What are the diff erent forms of state aid and how are all the tax incenti ves and Covid-19 support packages categorised?

What does it mean for me?

There are limits on the number of types of aid and the amounts a business can receive. It is important not to fall foul of these limits as a clawback of support at a later date can be very damaging to a business, especially if the support is tax related and a clawback involves not just the aid received but also interest, penalti es and professional fees.

What can I take away?

Armed with a basic understanding of the state aid rules, you can help your clients to ask the right questi ons when seeking support, and make sure they are keeping the records they need to show they have taken due care.

In these unprecedented times, we are seeing support mechanisms from the government which are very generous and wide ranging. These are going a long way towards helping businesses to keep going and weather the storm so that hopefully they can come back stronger in what is looking increasingly like a very different post-Covid-19 world.

The existence of these new schemes has raised a lot of questions around the implications of state aid. We are still bound by the European rules, at least for the time being – we are currently in a transition period which is due to end on 31 December 2020. After this date (which could change), the UK will be free of many of the European Union restraints on the provision of aid; however, as I understand it the European Commission will maintain some supervisory powers for up to four years following this date, which it will use to review approved measures.

What is state aid?

As defined by the EU treaties, ‘state aid’ is a term used to describe any assistance or subsidy given by a member state that confers an advantage on a selective basis to organisations that take part in economic activity, which distorts or threatens to distort competition. In essence, the state aid rules exist to prevent unfair advantages being given to selected businesses. State aid is permissible when it is by measures that can be demonstrated to have a wider economic benefit, despite their rewarding individual businesses.

There are financial limits as to how much state aid a business can receive, and therefore it is crucial to keep an eye on how the different forms of aid interact. Failure to do so could, in the most extreme cases, mean that a valuable relief or support mechanism is denied to a business because it has previously harnessed another (potentially far less valuable) relief.

Worse, if the aid was a tax incentive (such as research and development (R&D) tax relief or seed enterprise investment scheme (SEIS) income tax relief) and is later withdrawn, it is entirely possible that HMRC may be required to seek late payment interest and penalties in addition to the clawed back cash.

For example, R&D tax relief under the SME scheme is notified state aid. If other forms of aid have been received, there is a risk that CTA 2009 s 1138(1)(a) may deny the R&D relief, instead pushing that claim into the less beneficial R&D expenditure credit (RDEC) scheme. If HMRC discovers this in an enquiry, it is likely to seek penalties if it considers that the business owner has not taken reasonable care.

The different types of state aid

State aid can take a large number of forms, both national and local. It includes some seemingly innocuous support, such as short sessions with a business coach for free or at a reduced price, free or subsidised training courses, and continuing professional development (CPD). However, this article focuses primarily on financial measures which broadly fall into one of two types of state aid: notified state aid and de minimis state aid.

Notified state aid

Notified state aid is provided at a level that requires the provider (whether a government department, local authority or otherwise) to make a specific notification to the European Commission. It is not permitted for a recipient to receive more than one form of notified state aid in respect of any ‘defined project’. I have spoken to businesses which have fallen foul of this when they have received a small start-up grant for a product development project, but have then been denied R&D tax credits which, in hindsight, would have been worth far more.

Notified state aid includes the following:

- R&D tax relief under the SME scheme;

- grant funding: not all grants are so classified but a lot are, including most from Innovate UK – grant providers should always be able to advise whether they are notifiable or not; and

- support under the Coronavirus Business Interruption Loan Scheme (CBILS) and Bounce Back Loan Scheme (BBLS).

To avoid falling foul of the notified state aid rules, businesses should be clear exactly what the funds will be used for in their applications for grants and support. In the case of CBILS and BBLS, it is likely that the funds are for generally supporting the business rather than specifically for an R&D project, so eligibility for R&D tax relief under the SME scheme is unlikely to be affected. However, it is crucial to be clear about this in applications for CBILS and BBLS and also to keep records to evidence what the funds have been used for.

In particular, the BBLS application process is so straightforward that there is no facility in the process to specify what the loan is for. Internal records would therefore need to be kept to make it clear that the loan is, for example, to provide working capital for the business.

Grants which are notified state aid are often from Innovate UK and are often for 70% of defined project costs. While this means that R&D tax credits cannot be claimed for the same project, at a 70% funding rate this is more beneficial anyway (an R&D tax credit will be worth a maximum of around 33% of qualifying costs) so businesses do not lose out overall. However, where the rate of funding from a grant is lower than 70%, the business owner should always seek advice from their R&D tax adviser so that they can understand the potential impact on their ongoing R&D claims.

If the business cannot claim the R&D tax credits because of the existence of other notified state aid, it can still claim R&D support under the large company R&D expenditure credit (RDEC) scheme. Although this is not as beneficial, it is still worthwhile. Projects which have not been the subject of other forms of notified state aid can still be claimed under the SME scheme.

There are financial limits as to how much state aid a business can receive, and it is crucial to keep an eye on how the different forms of aid interact.

De minimis state aid

Some forms of aid, typically not quite so generous, are classed as ‘de minimis’ aid, which is subject to an overall financial limit of €200,000 over a rolling three year period. In a small number of business sectors, this figure is lower.

There is a lot of support which classifies as de minimis aid, including:

- seed enterprise investment scheme (SEIS);

- employment allowance; and

- Covid-19 support grants under the Small Business Grants Fund and the Retail, Hospitality and Leisure Grant Fund.

There is also a lot of other local and national state funded support, including discounted advertising or consultancy services, discounted or free training, and purchases of land or property at less than market value. But there are many more forms of support too.

De minimis aid should be tracked on a continuous basis by businesses as there are so many sources. Most small businesses are unlikely to fall foul of the rules for this. However, where a fledgling high growth business is obtaining equity finance, it will want to make use of SEIS to make it more attractive to angel investors.

A note about SEIS

SEIS status means that an investor can potentially claim a tax refund equal to 50% of the amount they invest for shares. However, this relief is classified as de minimis aid and counts against the company’s rolling three year limit of €200,000.

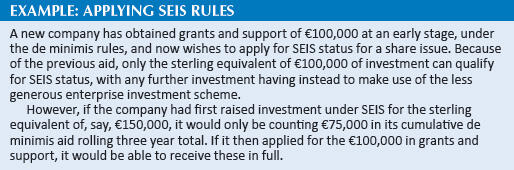

The way this works is rather odd (see example above). When a company is seeking SEIS investment, the maximum it can obtain under the scheme is £150,000, and any de minimis aid obtained in the previous three years will be deducted from the amount it can raise under the scheme. However, if things happen the other way round, and SEIS shares have been issued for £150,000, then the amount the company has to track is the tax relief obtained by the investors; therefore, potentially only £75,000 (converted to euros at the time of the investment) has to be tracked for the following three years. This approach is confirmed by HMRC in its manuals at VCM2040.

General Block Exemption Regulations

Certain forms of aid fall under the EC’s General Block Exemption Regulations framework. This framework covers a range of types of state aid that (subject to conditions) do not require notification to the EC.

In practice, where aid falls into the Block Exemption rules, a business can be confident that this will not affect its eligibility for other forms of state aid.

The forms of aid covered by the Block Exemption rules is wide ranging, but in terms of tax this includes risk finance investments, in particular the enterprise investment scheme (EIS).

When the conditions for a state aid to fall under Block Exemption are examined, many of these are identical to the rules of the EIS scheme, in particular the limit of €15 million of support and the requirement that the aid commences (broadly) within seven years of a first commercial sale.

Other support which is not state aid Forms of support which are not classed as state aid include the following very current support mechanisms:

- The Coronavirus Job Retention Scheme: Although generous, this is not classed as a state aid because it is not a selective measure and therefore is not considered to distort competition.

- The Future Fund: The government has confirmed that this scheme is a convertible loan advanced on commercial terms, and is therefore not classified as state aid.

Innovate UK’s current range of continuity grants and loans, although technically state aid, fall under a Temporary Framework for State Aid which applies until 31 December 2020, and has a limit of €800,000 per business. This framework was introduced by the EC in March in specific response to the Covid-19 pandemic and exists to provide EC member states with the ability to offer a wider range of support to minimise the economic impact of the crisis.

Companies in difficulty

Many forms of state aid have a requirement that the business must not be ‘in difficulty’ by virtue of the EC rules. The Covid-19 specific support mechanisms, while still bound by this rule, usually require a snapshot of the business at 31 December 2019 in determining this, so that the pandemic itself should not have impacted the business at that stage.

There are various ways a business can be classed as ‘in difficulty’, but for a continuing business the usual test is quite formulaic, and requires you to determine whether accumulated negative profit and loss reserves are more than 50% of the subscribed share capital. Where it appears that this may be an issue, particularly for an early stage company worth reviewing the company’s capitalisation policies, particularly around R&D where a product is not yet commercialised. Many SME businesses will simply expense their qualifying R&D costs instead of capitalising these as intangible assets, and often it will be possible to capitalise these R&D costs with the result that the ‘in difficulty’ test will not be an issue.

The accountant and the client will have to critically review the capitalised R&D each year and write off any costs in full that relate to aborted projects, as well as amortising any commercialised project R&D at an appropriate rate at the appropriate time.

In conclusion

As there are now so many kinds of state aid available, it has become more important this, in particular where this is ‘de minimis’ aid. For example, if a business hits the €200,000 maximum, it would be very easy to do something which all small businesses may take for granted now and claim their employment allowance of £4,000 through the payroll to discount the employer’s NIC – without realising they might not be allowed to do so due to the level of de minimis aid received elsewhere.

With the UK’s impending exit from the EU, and the time approaching when we will no longer be bound by the EC regulations, it is a somewhat ironic turn of events that have led to such a large number of support mechanisms being launched in 2020, meaning that it has suddenly become so important to ensure a basic understanding of state aid interactions.