Construction Industry Scheme reforms could result in tax simplification

Share this article

A number of Construction Industry Scheme reforms could result in tax simplification, benefiting landlords, tenants and HMRC. We take a look at three areas which are ripe for review.

Key Points

What is the issue?

Landlords are now collaborating with tenants to assist them in obtaining early possession and in modelling space to suit their needs, rather than remodelling what they are presented with by landlords.

What does it mean to me?

For Construction Industry Scheme purposes, the landlord may need to withhold tax from Category A payments to a tenant if the tenant is not registered for gross payment under the scheme.

What can I take away?

The CIS rules place a significant burden on tenants, the majority of whom are not in the construction industry but rather unrelated industries.

The purpose of this article is to highlight three areas ripe for review in relation to the Construction Industry Scheme (CIS).

1. CIS implications of landlord contributions to tenants

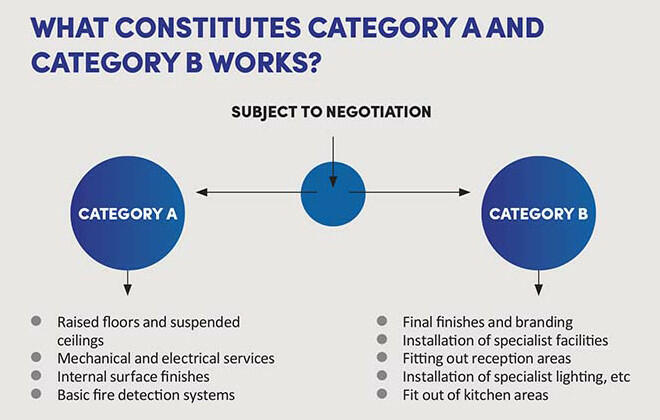

Landlord contributions to tenants for landlord works (Category A) and for tenant works (Category B) are becoming more common. Landlords are now collaborating more with tenants to assist them in obtaining early possession and in modelling space to suit their needs, rather than remodelling what they are presented with by landlords. This has time, cost and environmental benefits. For CIS purposes, the key issue is that the landlord may need to withhold tax from Category A payments to a tenant if the tenant is not registered for gross payment under the scheme. Incorrect classification of contributions results in disputes with tenants and potentially significant tax liabilities and penalties.

From a CIS perspective, there is no statutory definition of what constitutes Category A and Category B works. Most works fall into one of those categories but the identification problem pertains to the ‘grey’ area in between. Both the landlord and the tenant will need to agree the categorisation of these grey areas, which could include back-up generators, roof terrace enhancements or additional air-cooling requirements, for example.

Often, the proposal for allocating costs between Category A and Category B will be influenced by the tax and accounting treatment of both the landlord and tenant, so their initial analysis may reflect these influences.

This article addresses the issues pertaining to Category A works, as this is the area that is problematic from a CIS perspective.

Application of CIS to Category A works

The main commercial drivers for making contributions to tenants’ works are efficiency, and improving timing to facilitate early possession.

A tenant may wish to start their own works prior to or at the same time as the landlord’s Category A works. In this case, a landlord may agree that the tenant can use their own building contractors to carry out or finish the landlord’s works in conjunction with their own Category B works. Dovetailing the works is more efficient and ensures that the works are carried out to a consistent standard.

Alternatively, the tenant may require a higher specification for their own purposes and wish to enhance a particular area over and above the standard specification, using their own building contractors.

Payments fall within CIS if they are made under a construction contract, defined in Finance Act 2004 s 57 as a contract relating to construction operations (which is not a contract of employment) where one party is a sub-contractor and the other is a contractor. As things currently stand, the tenant (as sub-contractor) in receipt of a Category A contribution must undertake to comply with the requirements of the CIS scheme under Finance Act 2004 Part 3 Chapter 3 and the Income Tax (Construction Industry Scheme) Regulations 2005 (SI 2005/2045) (‘the Regulations’). The tenant will either be registered for gross payment or subject to deduction of tax at the relevant percentage stated under the scheme rules under Finance Act 2004 s 61.

Notwithstanding the above, certain payments are excluded from the rules, in particular:

- If the payment from the landlord to the tenant is an incentive to enter into the lease: This is a reverse premium (or would be a reverse premium but for the capital allowances carve-out) under regulation 20 of the Regulations. Most Category B items are taxed as reverse premiums in the tenant’s hands and therefore outside the scope of CIS under this regulation.

- If the tenant is not contractually obliged to do the work, they would not then be a ‘sub-contractor’ (Finance Act 2004 s 58): Sometimes the landlord will allow this even for Category A contributions, relying on a combination of commercial reality (as the tenant will want to do the works) and the rent review clause.

Impact of the CIS rules on tenants

The CIS rules place a significant burden on tenants, the majority of whom are not in the construction industry but rather unrelated industries, including hospitality, technology, and media and publishing, to name a few. For companies such as these, registering as a sub‑contractor for CIS (in order to receive gross payments from the landlord) is time consuming and costly. Due to the complexity of the rules, they will often ask their legal teams or accountants to make the application to register as a sub-contractor on their behalf.

An inordinate amount of time and money can also be spent by the landlord and tenant agreeing legal wording to ensure that the contributions are identified, categorised and invoiced correctly. In the event that a tenant is not registered for gross payment as a sub‑contractor, the landlord’s right to deduct must be properly documented.

Obtaining gross payment status can be difficult for tenants setting up a business or expanding into the UK for the first time because they will not have a trading history. In the absence of obtaining gross payment status, a tenant will be subject to deduction of tax at either 20% (if registered) or 30% (if not registered), which can lead to severe cash flow problems:

- Start-ups and owner-occupied businesses may struggle to recoup the CIS deduction against relevant liabilities because they do not have the payroll capacity to offset the amounts. They will often have to wait until the end of the tax year for the deduction to either be refunded or offset against any corporation tax due.

- Tenants may need to pay their sub‑contractors in full but due to the CIS deduction being applied on the payment from the landlord, they will have a shortfall which they will have to fund until they are repaid by HMRC.

In many cases – especially the hospitality sector, which has suffered more than most during Covid – the cash flow problem created by the CIS deduction can result in protracted negotiations between the parties as they attempt to mitigate the impact. Some of these mitigation measures include:

- a change in the works specification;

- the tenants having to secure additional funding; and

- in extreme cases, the landlord funding the shortfall on behalf of the tenant.

All three situations result in delays to the tenant commencing operations from the property.

Caught in the middle

When a landlord makes a contribution to a tenant to carry out works, the tenant in most cases is not physically carrying out the works but sub-contracting them to a third-party building contractor.

The tenant may not qualify as a deemed contractor, such that any payments they make to the building contractor are not deemed to be CIS ‘contract payments’. That is because of the exemption under regulation 22 of the Regulations for ‘own build’ works, which applies where:

- the expenditure is in respect of works to their own premises;

- the property is ‘used for the purposes of the business of [the tenant]’; and

- at the point when the tenant makes the payment, they have incurred more than £3 million on construction operations in the past year.

Thus, the effect of regulation 22 can be that the tenant does not have to apply CIS when they make payment to their building contractor for works carried out at the start of the lease (regardless of the nature of the works).

The interposition of the tenant between the landlord and the tenant’s third-party building contractor can mean that the tenant has to suffer a deduction from a payment from the landlord but will not be able to make a deduction from payments to the third party because regulation 22 applies. It is this asymmetry in treatment which creates a cash-flow difficulty. Even where regulation 22 does not apply to a particular payment, perhaps because the tenant has not at that point passed the £3 million threshold, there would still likely be asymmetry in the treatment if the tenant’s third-party building contractors were registered for gross payment.

The mischief the rules were originally intended to capture should only be a concern in relation to the building contractor physically carrying out the construction works on behalf of the tenant. Applying the scheme to payments between landlord and tenants for the same works seems to be outside the original policy intent.

2. CIS grouping

The concept of grouping does not currently exist for CIS, so a large group company must register all subsidiaries individually for CIS (assuming they are deemed or main contractors). The compliance burden in having to report each subsidiary is significant in terms of administration time, such as collation of data by each company, verifying the same sub-contractor, making withholding tax payments and online filing for each company.

Introducing a group CIS return to ease the administrative burden in a similar vein to VAT grouping (where you nominate a representative member with joint and several liability for all members of the CIS group) would seem a sensible solution.

Submitting one CIS return under one PAYE reference is not only administratively beneficial for businesses but also for HMRC.

3. Intragroup transactions

CIS also applies if one company in a corporate group acts as a developer under a development management agreement providing services to another group member. The company providing the services to another group member will have to register as a sub-contractor and additionally function as a deemed/mainstream contractor in respect of the contracts it operates with ‘genuine’ third party contractors.

For the same reasons as above, it seems to be outside of the original policy intent that the rules should apply within a corporate group. The revenue is protected because of the requirement for a group member, acting as a developer, to register as a deemed/main contractor (subject to any exclusions) when dealing with the third-party building contractors. This scenario is administratively burdensome, and another example of where innocent transactions are caught under the scheme because the CIS net is cast too wide.

The way forward

These issues should be at the front of the queue for consideration by HMRC as an easy-win tax simplification measure.

Members in industry and the profession are engaging with HMRC. If you would like to assist in making a positive change to the existing CIS rules, please see the note in Tax Adviser by the CIOT’s Kate Willis, ‘Construction Industry Scheme: landlord contributions to tenant works’ (see bit.ly/3wNmBqu), where there is an email address for correspondence.