Time to plan

Share this article

In his second article on the VAT domestic reverse charge for construction, David Westgate examines the areas which will require further clarification and issues impacting developers

Key Points

What is the issue?

The guidance on the VAT domestic reverse charge for building and construction services will need to clarify the position in relation to a number of elements.

What does it mean to me?

It is likely that some businesses will be required to account for the reverse charge for the first time, so their accounting systems may have to be adapted to deal with this.

What can I take away?

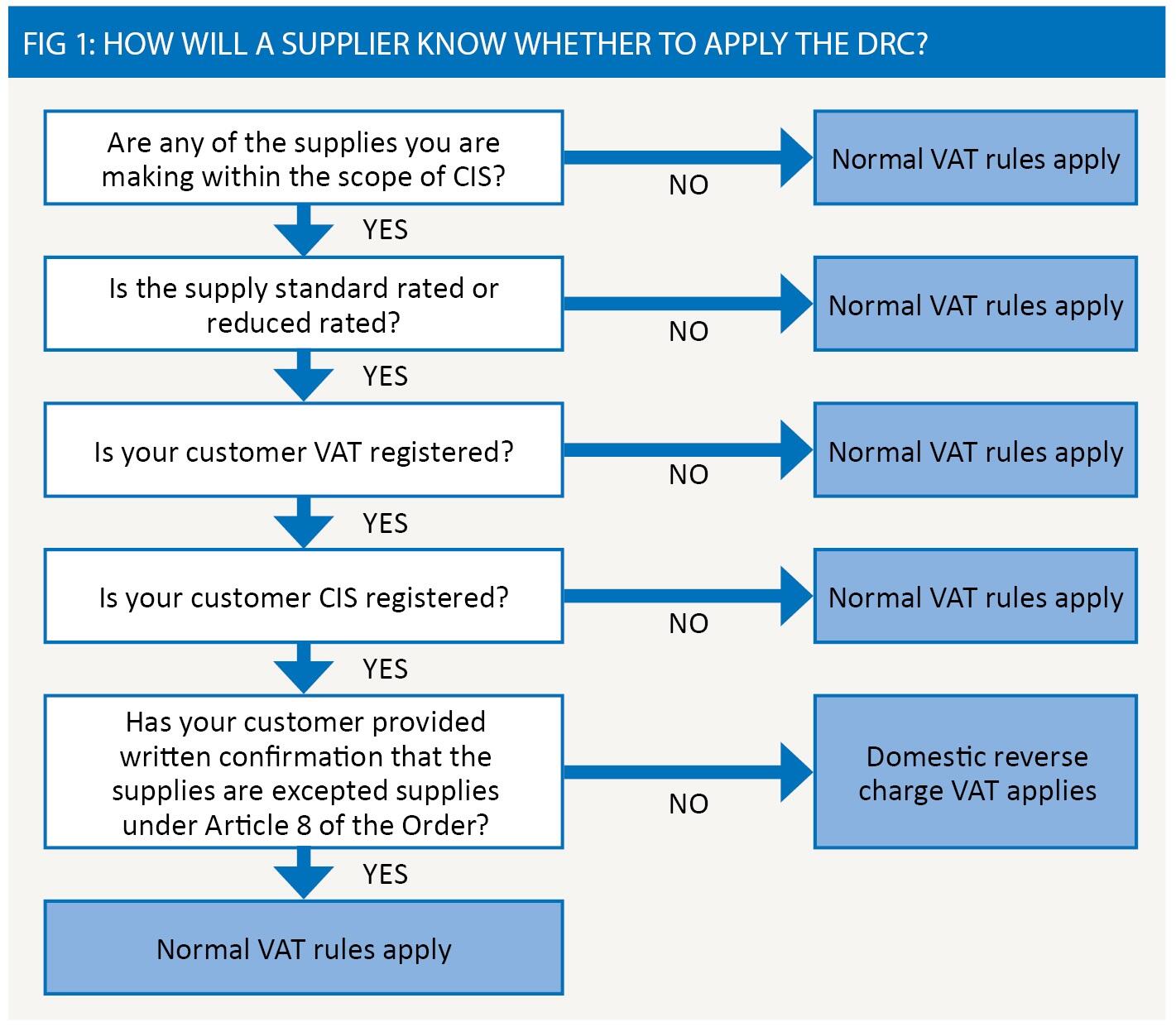

The default position is that DRC applies unless the customer states otherwise. It is therefore critical that end users are clear as to when the DRC rules apply.

A new VAT domestic reverse charge (DRC) will be introduced on 1 October 2020 for building and construction services. (This was originally 1 October 2019; see Revenue and Customs Brief (10), dated 6 September 2019.) The final version of the draft Value Added Tax (Section 55A) (Specified Services and Excepted Supplies) Order 2019 was issued on 7 November 2018 together with related guidance.

The first part of this article, published in the September issue of Tax Adviser, considered the application of the DRC and its interaction with the construction industry scheme (CIS).

Need for further clarification

Based on the latest legislation, the guidance will need to clarify the position in relation to a number of elements, which are set out below.

Landlord and tenant arrangements

1. Prospective tenants under an agreement for lease

Article 2(2)(b)(ii) precludes any temporary entitlement to occupy land for the purposes of making supplies of construction services from being a ‘relevant interest’. This could be interpreted to mean that a tenant under an agreement for lease (AFL), undertaking works for its prospective landlord (or vice versa), has only a temporary entitlement to occupy the land for the purpose of making specified supplies and so does not have a ‘relevant interest’.

It is helpful that the latest guidance has attempted to clarify the position by stating that ‘having an agreement for lease is also a relevant interest in land’, although it would have been more helpful to amend the SI. It would have been clearer if the SI had stated that any reference to landlord, lessor, tenant and lessee shall be interpreted as if an agreement for lease of land, buildings or civil engineering works were an [actual] lease of such land, building or civil engineering works on such terms as are provided for under or pursuant to that agreement for lease.

2. Works to common parts

It is still unclear whether the exceptions to the new rules include a landlord or tenant where the works are carried out outside the property demised. To ensure that supplies in relation to common parts are covered, it would be helpful if the Order could be amended to add ‘or for the purposes of’ immediately after ‘in relation to’ in para 8(1) (b)(ii)(bb), or clarify the position in guidance. I would suggest that the tenant has a permanent licence to go onto the common parts, even if not to occupy them, and therefore has a relevant interest under Article 2(2)(b)(i). However, this needs to be clarified.

Written end user confirmation

The default position for DRC is that the reverse charge applies unless the supply is an excepted supply under Article 8 of the Order. In its guidance, HMRC states that ‘if the end user does not provide its supplier with written confirmation of its end user status, it will still be responsible for accounting for the reverse charge’. It is not clear that this is embedded in statute, but nonetheless customers have been put on notice. This means that if a supplier does not charge VAT (when it should have done), the customer becomes liable to account for it under DRC (even if it is an end user).

Customers must be vigilant in policing their status on all transactions, including all invoices from suppliers. A customer’s written confirmation of end user status (that the supply it has received is an excepted supply under Article 8 of the Order) may be in any format, e.g. included in the contract/order, in an email or delivery of a written statement.

There is no specific wording required for this written confirmation, but the following should be acceptable:

‘[The customer] considers that the services supplied by [the supplier] under [this contract/order] are excepted supplies under Article 8 of The VAT (Section 55A) (Specified Services and Excepted Supplies) Order 2019 and that the services are not subject to domestic reverse charge VAT. VAT at the appropriate rate should be charged by [the supplier] on the services supplied.’

For companies that only have to operate the reverse charge in very limited circumstances (as most operations fall within the excepted supplies definition under Article 8), having a blanket ‘Certification’ in all its contracts and orders may be a workable solution. The situation is different for companies that have a mixture of services, so they will have to consider whether the exception in Article 8 applies for each and every contract they enter into.

Mixed developments

It is quite common that a customer procures specified services from a single supplier (though not as a single supply) for more than one purpose, or that the status of the customer may change during the contract. This can cause complications in having to deal with differing VAT treatments, as parts of the supply will be within DRC and other parts under the normal VAT rules.

To deal with this, the legislation has been rather helpful. For example, Article 8(2) provides a voluntary mechanism for avoiding apportionment of the contract, allowing the parties to agree that all the supplies under the contract will not be treated as excepted supplies under Article 8(1) and the DRC will apply. This could arise in a situation where a contractor procures specified services under the same contract partly for an onward supply and partly as an end user.

Article 9 applies where there is a single supply for VAT and the supply is made up of several identifiable parts. Even though there are separately identifiable parts, the whole supply is still subject to the DRC unless each and every identifiable part is excepted from the DRC rules.

Developer issues

1. Prudential type arrangements

In certain cases, a landowner will sell the land under one contract to a purchaser and develop the building (which may be partially completed) for that purchaser under a separate contract. Under this structure, the landlord will have to account for the reverse charge on supplies from its contractor, as it would be supplying construction services to the purchaser. If, on the other hand, the landlord had sold the land and completed building under one contract to the purchaser after completing the development, it would not have had to account for the reverse charge on the construction costs, as it is not supplying specified services to the purchaser. It seems an odd result, given that if the contracts had not been separated out, the reverse charge would not be in point.

2. Forward funding

A landlord may commence works on a speculative build with the intention of letting or finding a buyer on completion. In this respect, the landlord will be an end user and the DRC will not apply, such that VAT is payable in the normal way. There may, however, be situations where the landlord has pre-let the building and as such de-risked the development; and therefore decides to sell the development to an investor prior to completion but with an agreement to complete the development for that investor. This raises two issues.

Sale of the freehold: Where there is a sale of the freehold of the part-completed building, the landlord will enter into a development agreement acting as contractor to the investor. At this point, the landlord will no longer be an end user but rather a contractor supplying specified services to the investor. The landlord will account for the reverse charge and stop paying VAT to its contractors. The investor will become an end user and the landlord will invoice the investor with VAT in the normal way. Note that Article 8(2) is no help because it does not apply until there have been DRC supplies – there is no option but to change the VAT treatment mid-way.

Grant of a lease: The outcome above is different where there is a grant of a lease (whatever the duration). In this respect, the services of the landlord’s contractors will be excepted supplies under Article 8(1)(b)(ii)(bb) and the landlord will continue to be an end user and continue to pay VAT to its contractors.

3. Ongoing obligations

It is not clear whether any payments to a contractor in connection with ongoing construction obligations attaching to the vendor after it has sold the building to a third party are to be treated as excepted supplies (as the vendor at this point will not be an end user).

4. Retention payments

A retention payment represents monies withheld from works for a period pending any deficiencies in the works that may become apparent during the period. The retention period could last a number of years. If a payment for retention is made to the contractor after selling a building, it could potentially be treated as an onward supply of specified services and require the seller to apply the reverse charge.

To address the anomalies in points 3 and 4 above, the guidance needs to clearly state that the treatment of such supplies will follow the status of the customer at the time of practical completion of the contract to which the obligations or retention relate.

Mid-contract changes

Where there is a change in the status of the customer during a construction contract, i.e. in a forward funding type of arrangement, HMRC’s guidance should set out the process for managing the change to reverse charge invoicing. Two key aspects should be considered here.

Firstly, there is the event or trigger point which constitutes the change in treatment; it is suggested this should be the date that the relevant legal agreement is signed.

Secondly, it would be helpful if taxpayers have a reasonable period of time after the trigger date to effect an orderly transition to the new invoicing arrangements. In this respect, consideration will need to be given to how certain changes in the legal or other status of either party are to be communicated to the other, the main challenge in this instance being that the person with responsibility for such communication will need to be made aware of the new reverse charge rules.

Impacts for MTD and internal processes

It is likely that some businesses will be required to account for reverse charge for the first time, so accounting systems may have to be adapted to deal with this. Note that under Making Tax Digital (MTD), you will be required to account for reverse charge using functional compatible software, i.e. via your accounting system or Excel spreadsheets or both. Early planning is key to ensuring you comply.

Internal processes will need to be reviewed to ensure that there is interaction between the teams dealing with CIS and VAT. Often, these operations will be dealt with by separate teams.

Implications for the VAT threshold

The DRC will not count towards the customer’s taxable turnover for the VAT registration limit. This is to be achieved by an amendment to s 55A (by introduction of s 55A(9A)), as provided for in the Finance Act 2019 s 51, which now has Royal Assent. Article 10 of the draft Order also provides that the effect of VATA 1994 s 55A(3) (which makes provision for reverse charge supplies to be treated as supplies made by the recipient for the purposes of VAT registration limits) shall not apply.

Penalties

HMRC will be adopting a light touch approach for the first six months to give businesses a chance to become familiar with the new rules. However, taxpayers have suggested that a longer period of 12 months would be more appropriate and is also consistent with HMRC’s light touch approach for other new regimes, e.g. MTD.

As stated above, the default position is that DRC applies unless the customer states otherwise. However, if a customer’s status changes such that DRC is applicable to ongoing supplies from their contractor and their contractor continues to charge VAT (because the customer did not notify their change of status), then recovery of that VAT may be in doubt. In addition, penalties and interest may apply for not having operated the DRC, as well as having to account for the VAT.

It is therefore critical that end users are clear as to when the DRC rules apply (see Fig. 1). You can see difficulties arising; for instance, where an end user makes onward supplies of specified services but has not registered under CIS, either because they are unaware of the CIS rules or they register late. If the sub-contractor had initially confirmed that the customer is not subject to the CIS rules, it will charge VAT that may not be recoverable by the customer.