Seeing the scope

Share this article

David Westgate considers the scope and impact of the new VAT domestic reverse charge on construction

Key Points

What is the issue?

A new VAT domestic reverse charge (DRC) will be introduced on 1 October 2019 for building and construction services. It is aimed at combatting fraud in the construction sector labour supply chains.

The change was originally planned for 1 October 2019 but on 6 September 2019 the Government announced a twelve month delay in introducing the new rules.

What does it mean to me?

Combatting the fraud is achieved by requiring the recipient of the supply – the customer – to account for the VAT as ‘output VAT’ directly to HMRC, rather than pay it to the supplier of the services. The customer can still recover the VAT as ‘input VAT’ in the normal way, subject to their own VAT position (e.g. partial exemption).

What can I take away?

Businesses will need to consider how the new rules impact their supply chains, cash flow, contractual provisions and accounting systems, and provide effective communication and training for appropriate personnel.

New legislation is being introduced that will impact businesses that receive supplies of building and construction services. These services clearly include heavy duty works but will also include things such as painting and decorating, general repairs, site clearance, and electrical and plumbing work. Goods or materials supplied in conjunction with the supply of building and construction services are also included.

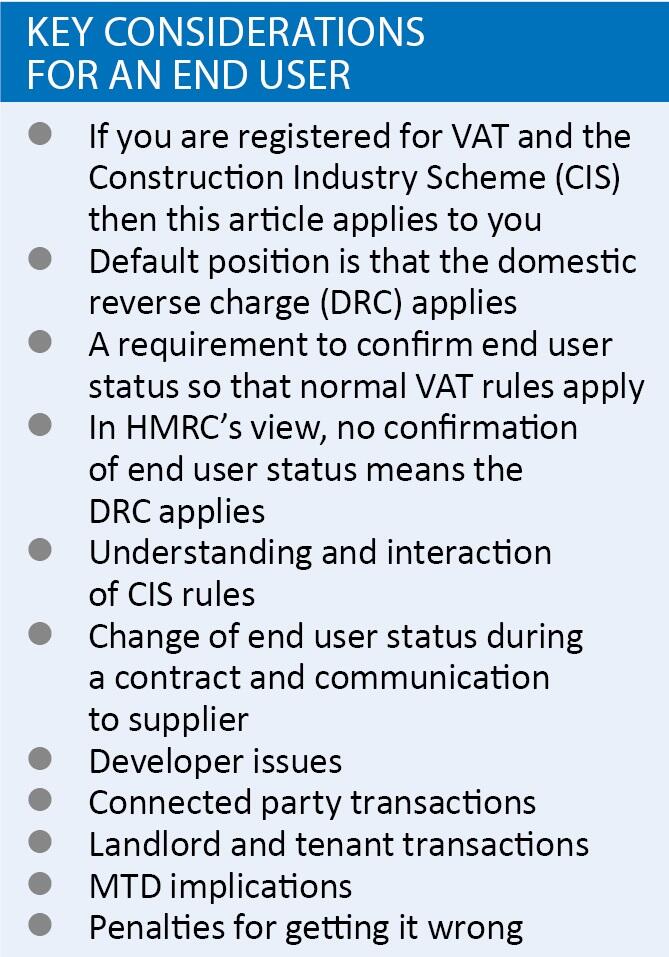

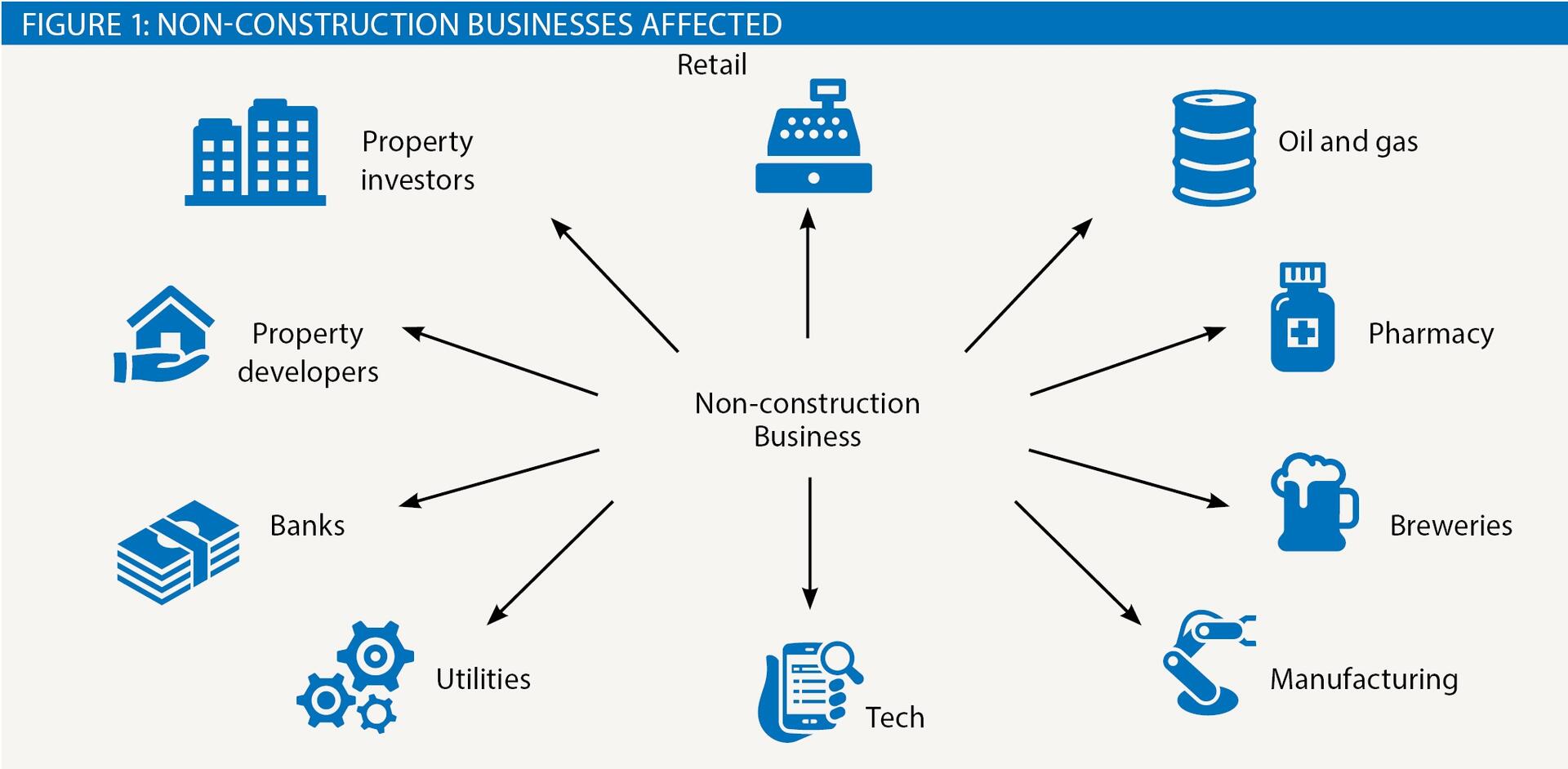

The purpose of this article is to outline the impact of this new legislation on businesses which receive supplies of building and construction services (‘specified services’) for use in their own business and not generally for the purpose of making an onward supply of such services. The new legislation refers to such businesses as ‘end users’. These businesses will be VAT registered, and deemed or mainstream contractors under CIS rules (FA 2004 s 59(1)) and will typically be non-construction businesses, as shown in Figure 1.

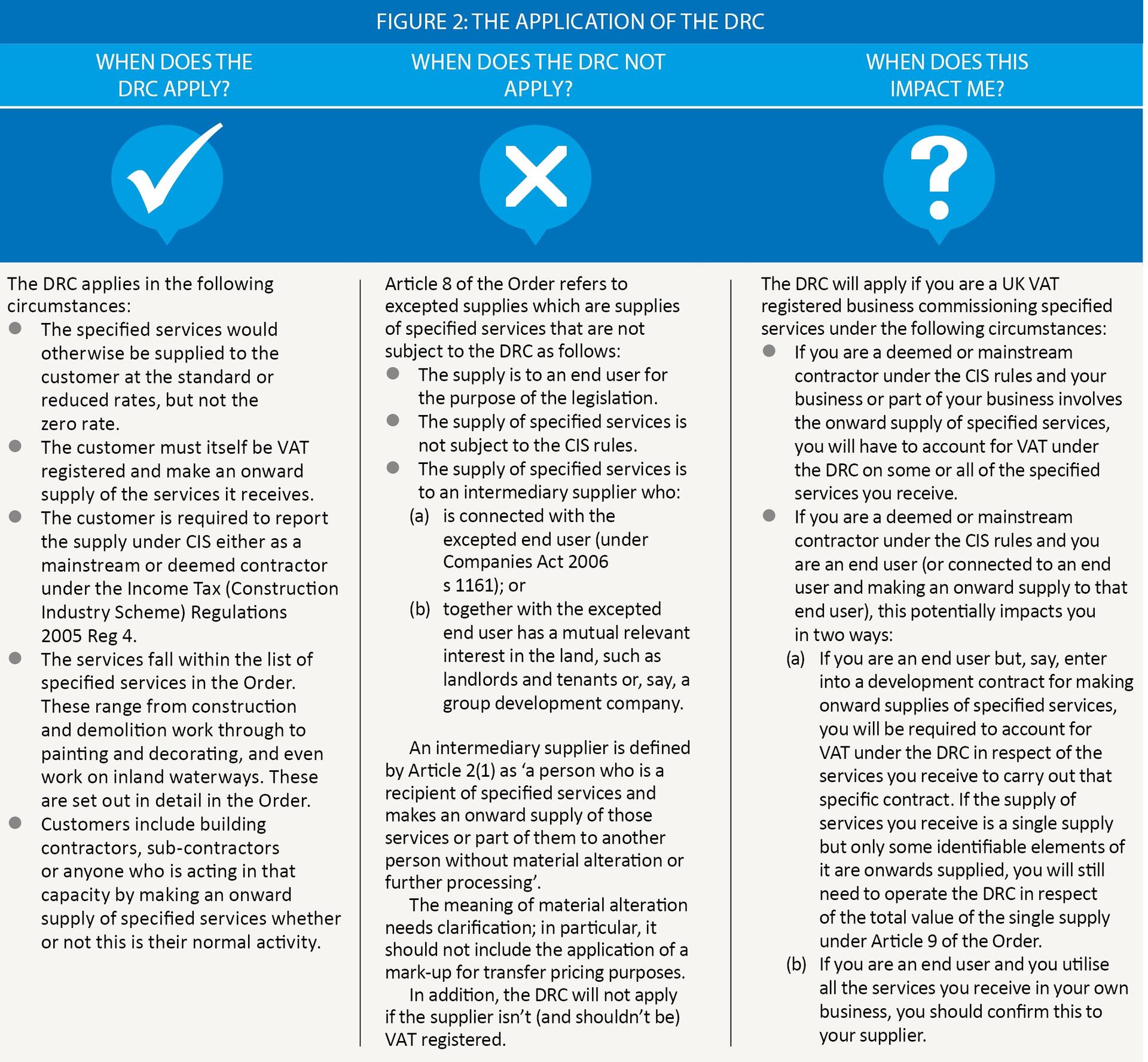

Application of the DRC

A new VAT domestic reverse charge (DRC) will be introduced on 1 October 2019 for building and construction services. It is aimed at combatting fraud in the construction sector labour supply chains.

According to HMRC, the fraud is most commonly found among sub-contractors further down the supply chain who provide groups of workers to the construction sector. They typically have low recoverable VAT costs (mainly wages not subject to VAT) but charge VAT on the supply of construction services and don’t pay the VAT to HMRC.

Combatting such fraud is achieved by requiring the recipient of the supply – the customer – to account for the VAT as ‘output VAT’ directly to HMRC, rather than pay it to the supplier of the services. The customer can still recover the VAT as ‘input VAT’ in the normal way, subject to their own VAT position (e.g. partial exemption). Because the customer both pays VAT and recovers VAT, the net cash position is zero (subject very occasionally to partial exemption (PE)) and HMRC receive the money due to them.

The DRC removes the opportunity for suppliers of construction and building services to charge VAT and disappear before paying it over to the Exchequer. HMRC estimate that around £100m a year is lost due to this type of fraud.

The DRC does not apply if the customer is not VAT and CIS registered. Nor does it apply if the customer is an ‘end user’, meaning that the specified services it receives from the supplier are not in turn used to make onward supplies of those services to customers. In both cases, the supplier will charge VAT in the normal way and the burden of the VAT cost will fall on the customer. The supplier will need to account for the VAT to HMRC as output VAT in the normal way.

The Construction Industry Scheme (CIS) was also developed to combat fraud and the DRC is closely aligned with it. The DRC does not apply if the customer does not operate CIS, even if the services supplied are closely aligned with those covered by the CIS (though separately defined by the relevant statutory Instrument).

Legislation and guidance

VATA 1994 s 55A sets out the framework for anti-fraud measures of this kind and allows for a reverse charge to be introduced for particular types of supply by Treasury Order. The final version of the draft Value Added Tax (Section 55A) (Specified Services and Excepted Supplies) Order 2019 was issued on 7 November 2018, together with related guidance. The final Order itself was laid in spring 2019.

Interaction with CIS

The CIS definition in Articles 5 to 7 of the Order is taken directly from FA 2004 s 74(2) and (3). Although helpful in providing a description of the types of works that fall within CIS, businesses would be well advised to refer to the CIS regulations and guidance. HMRC have confirmed that they expect to see the reverse charge apply where CIS applies unless explicitly provided for otherwise, for example for end users and intermediaries.

Some of the areas in the CIS guidance that provide further clarification are:

- Installation of systems: Installation of systems only applies in a CIS context if a new system is installed, not to repairing it or replacing parts of the old system. Installation of a security system must be a system, not simply a building feature that incidentally fulfils a security purpose.

- Professional services: Generally, the services of professionals, such as architects, surveyors or consultants, are outside the scope of the CIS, but only where they are providing services that are within their normal professional discipline. The CIS guidance states that any work that goes beyond a consultative or advisory role – and becomes the supervision of labour or the co-ordination of construction work using that labour – isn’t excluded from the scheme. Therefore, it is important to clearly establish the nature of the services being provided. Where the services provided are both executive and advisory under one contract, all the services provided will be within the scope of the CIS provisions.

Clearly, given the reliance that will be placed on the legislation, and considering the number of people that will have to familiarise themselves with the CIS definitions for the first time, it’s imperative that people refer to the DRC guidance and manuals, as well as the CIS regulations and related guidance in CIS 340, particularly in large organisations where the CIS and VAT functions are separated and people may therefore need to liaise.

Customers connected with end users

Article 8 (1)(b)(ii)(aa) treats the supply of specified services to an intermediary supplier who is connected with the end user as being excluded from the DRC and subject to VAT. The meaning of ‘connected’ is defined in the statutory instrument under Article 2(2)(a) and ultimately refers to the Companies Act 2006 s 1161. It applies where one company is an undertaking in relation to which the other is a group undertaking (subject to the conditions being satisfied in s 1162). Basically, this means that any company which is consolidated in the group accounts is treated as a single end user of specified services. Therefore:

- A development company procuring construction services on behalf of another group company that is an end user is treated as an end user and does not need to apply the DRC. It will pay VAT on the works under normal VAT rules.

- A group company may procure services to construct a building mock-up, which is not the same company undertaking the main development. The works which are closely connected with the main development may be carried out by the same contractor or a different contractor depending on the purpose of the mock-up. The company procuring the mock-up is treated as an end user and does not need to apply the DRC and pays for VAT on the works under normal VAT rules.

Note, the connection test above applies regardless of the number of VAT groups within a group undertaking. You effectively look through the VAT groups for the purpose of this test.

Landlord and tenant arrangements

Supplies of specified services procured by landlords and recharged to tenants (or vice versa) are excluded from the DRC under Article 8(1)(b)(ii)(bb). Therefore, if a landlord commissions works for a tenant or a tenant commissions work for a landlord, VAT will apply in the normal way. The effect is to treat landlords and tenants collectively as a single end user of specified services.

Reference to landlord and tenant arrangements should be taken to include sub-tenants, licensors and licensees, although consideration needs to be given to Article 2(2)(b)(ii) where a temporary entitlement to occupy land for the purpose of making supplies of specified services would not be excepted supplies under the Order.

The rule concerning temporary entitlement was primarily designed for contractors to ensure that they are still subject to the DRC by making it clear they do not have a relevant interest in the land. Contractors will normally obtain a licence to access the building site in order to carry out works (including the use of a site office for the duration of the works). However, the meaning of ‘temporary’ is not clearly defined under the Order and prospective end users will need to be alert to this point.

Based on the latest legislation, the guidance on the VAT domestic reverse charge should clarify the position in relation to a number issues, including prospective tenants under an agreement for lease, works to common parts, landlords procuring works for the tenant under an AFL, and written end user confirmation. These issues, as well as those relating to developers, will be examined in the second part of this article.