The costs of a wealth tax

Share this article

Bill Dodwell asks whether the UK should have a wealth tax, and if so how it should go about it

Two academics and a barrister (Dr Arun Advani, Emma Chamberlain and Dr Andy Summers) – together called the Wealth Tax Commission – have published a report on a possible wealth tax for the UK (see www.wealthtaxcommission.uk). Their work has been supported by a wide range of other, mainly academic, contributors. Their website contains a wide range of background papers, which are well worth reading.

What is a wealth tax?

A wealth tax is a tax levied by reference to an individual’s assets, net of any debt. Unlike a capital gains tax or a gift tax, it is not levied on an event (a disposal or a receipt) but is levied on a one-off or annual basis by reference to the value of an individual’s net assets on a defined day.

What do we own?

The authors have used the ONS Wealth and Assets Survey Wave 5 (see bit.ly/3nq4YWk) to highlight what we own. (I would recommend visiting the site to see how our asset ownership is broken down (see bit.ly/3ab1x1Q)). There is some doubt over whether the ONS survey captures enough of the wealth of the wealthiest and so the report authors have used the Sunday Times Rich List for additional data.

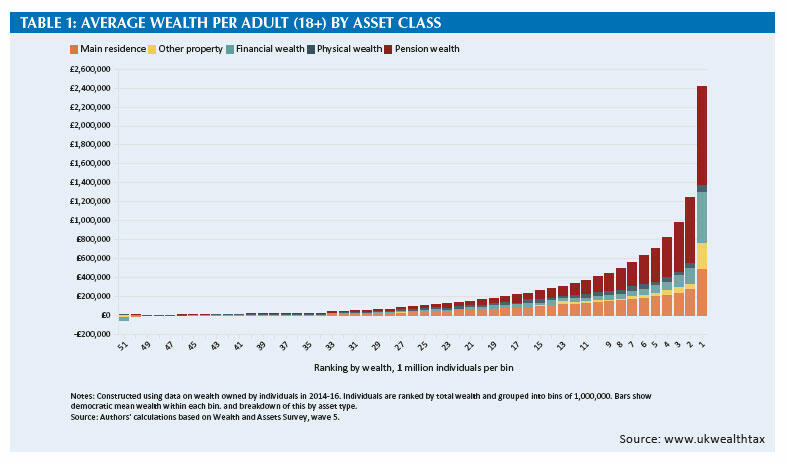

Just over 8 million adult individuals have net assets of £500,000 or more with the top 1 million having average assets of £2.45 million. Assets are split into main residence; other property; financial assets; physical wealth and pensions. The highest ranked 11 million individuals have more in their pensions than in their main residence and it is only the top 1 million who have significant financial assets, as well as other property interests beyond the main home. Financial assets include owner-managed companies, as well as cash in banks or building societies, shares or unit trusts and open-ended investment companies (OEICs) and other more exotic arrangements. Physical wealth is of course our personal possessions, which most of us probably do not quite see as wealth. For some, physical wealth could include some investments, such as an art or classic car collection. (See Table 1: Average wealth per adult by asset class.)

Perhaps as a point of reference we should note that the average house price in the UK was £244,000 in September 2020 (see bit.ly/3nmOwGf); 3 million individuals have a main residence worth at least that (net of mortgage debt).

How does the UK currently tax wealth?

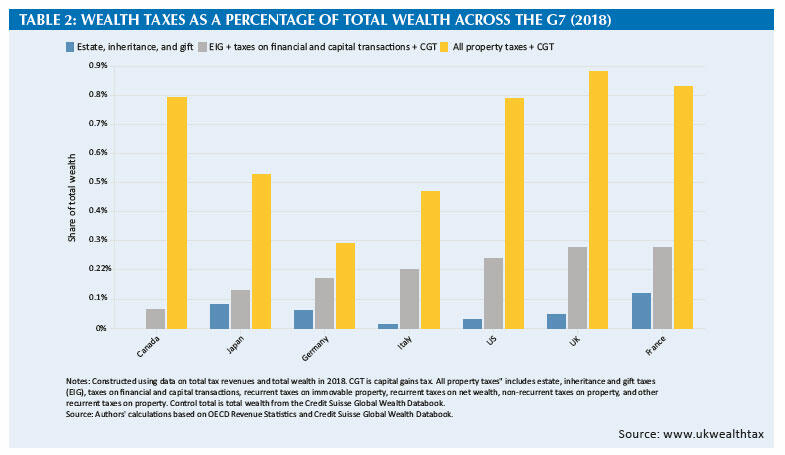

The UK, like most countries, has a wide range of asset-based taxes. Inheritance tax brings in over £5 billion annually, paid by about 25,000 estates. Capital gains tax brings in about £8 billion, paid by about 280,000 individuals and trusts. Property transactions taxes are expected to bring in about £9 billion this year but typically yield about £12.5 billion. Stamp duties bring in £3.5 billion. Finally, council tax brings in over £38 billion. Business rates typically yield about £32 billion, although the Covid-19 measures have dropped the current yield to £19 billion. The UK has a similar overall yield from asset taxes compared to other G7 members and has the highest level of property taxes, which bring in about 4% of GDP. (See Table 2: Wealth taxes as a percentage of total wealth across the G7 (2018).)

What do other countries do?

There is a useful background paper from the OECD’s Sarah Perret, which looks at examples of wealth taxes (see bit.ly/2WgAs5l). There are currently very few examples, although France and Germany (and others) used to have annual wealth taxes. Today, the only significant tax is in Switzerland, where the annual wealth tax raises 1.1% of GDP and 3.9% of total Swiss taxes. However, Switzerland does not levy capital gains tax and most cantons do not levy inheritance or gift tax. The other OECD countries with an annual wealth tax are Spain and Norway.

The most common exemptions from wealth taxes covered pensions and the main home but some countries introduced a much broader range of exemptions or reduced rates, before repealing them. Perret notes: ‘The most commonly cited justifications for the repeal of wealth taxes were that they reduced savings and investment, they encouraged migration, they were not effectively borne by the wealthiest households who could engage in tax avoidance and evasion, and they generated substantial administrative and compliance costs, especially compared to the limited revenues they raised.’

How long could it take to introduce?A background paper from Thomas Pope and Gemma Tetlow at the Institute for Government discusses the issues for a government in considering a wealth tax (see bit.ly/3mgPlPL). Whilst the UK has introduced a number of new taxes in recent years, they have typically applied to businesses and not to millions of individuals. Their paper concludes: ‘It could take over four years to rigorously consider the options, build public support and effectively legislate for and implement a new net wealth tax. However, such a long timescale may not be consistent with the UK’s five-year electoral cycles … Ministers could seek to expedite the process but there would be risks in doing so, particularly if the tax were to affect a relatively large proportion of the population and if the government had no existing mandate for this reform.’

Public opinion

Yet another background paper by Karen Rowlingson at the University of Birmingham, and Amrita Sood and Trinh Tu at Ipsos MORI looks at public attitudes through a representative sample survey, supported by four online focus groups (see bit.ly/37iHkp2). As with other recent public surveys, it found a high level of public support for a net wealth tax, although increases in council tax and capital gains tax were quite close behind. The interesting findings covered what the public thought should be subject to a wealth tax and its level. There was strong support for including financial investments and property wealth (after excluding the main home) as the base, but firm opposition to including pension wealth, the main home and cash savings. The majority of the public supported a threshold of £500,000 for the tax at a rate of at least 1%, followed by a £2 million threshold. The question made it clear that a £500,000 threshold would affect over 7 million people.

The recommendations

The final report, published on 9 December, recommends that the government should introduce a one-off wealth tax, potentially payable in instalments (see bit.ly/3oY86ct). It does not recommend an annual wealth tax, recommending instead that existing asset-based taxes are reformed to increase yield. The authors recommend that the taxable base should be all assets owned by an individual, net of debt. It thus includes the main residence, pension savings, personal property, cash savings, financial investments and other property.

The authors have modelled the yield, using individual thresholds of £500,000, £1 million and £2 million. At these levels, a wealth tax would respectively cover 17%, 6%, and 1% of the adult population.

The report authors calculate that a one-off tax at 5% on assets above £500,000, payable by over 8 million individuals, would bring in about £260 billion. The report recommends that it should be paid in five equal annual instalments. An individual with assets of, say, £1 million would pay a charge of £25,000 (amounting to £5,000 each year).

If instead the tax was levied only on assets above £2 million, it would bring in about £80 billion, payable by about 626,000 individuals.

Other permutations are naturally possible, including a system of graduated rates, which are illustrated in the report.

The authors’ recommendation for a broad-based tax is based on the desire for horizontal equity: individuals of similar means should not be taxed differently because (for example) one owns a house while the other holds cash while they wait to buy a house, or one has their savings in a pension while the other has reinvested their savings in their business.

This economic view would immediately quite significantly reduce support from the public, which is opposed to taxing pensions and the main residence. However, the chart showing asset breakdown makes it clear that only the top 1 million individuals have significant assets other than pensions and their homes. There would be a stark political choice: should a wealth tax be charged only on those with very substantial assets, or would the need for revenue spread the tax to the 8 million with total assets of at least £500,000? (This is significantly more than the 4.7 million higher and additional rate income taxpayers.) The report rejects the idea of linking a wealth tax levy to levels of income, since its purpose is to be a tax on assets.

However, we must wonder whether basic rate taxpayers feel themselves truly wealthy.

Another question concerns the taxable unit. The authors plump for the individual rather than a married couple. This looks unreasonable to me, not least because assets are commonly not held by each spouse in the way in which they would be divided on a divorce. It would be fairer to allow married people to file together, thus helping to share whatever the exempt band happens to be.

One of the challenges with an asset-based tax concerns a potential lack of funds from which to pay the tax. This is acknowledged in the report, which defines an individual as ‘liquidity constrained’ where the wealth tax payable in a year exceeds 20% of their income net of other personal taxes and it exceeds the combined total of 10% of their net income plus liquid assets. Based on these criteria, it is estimated that at a threshold of £500,000, around 1 in 14 of the individuals liable to pay the tax would be liquidity constrained. The proportion of liquidity constrained individuals rises to 12% in the range of total wealth between £1-2 million, 26% between £2-5 million, and 40% above £5 million. Particularly at lower levels of wealth, a great part of the challenge comes from including pension assets. Accordingly, the authors propose that the charge attributable to the pension should be payable by the pension fund from the tax-free lump sum at the first opportunity to draw it.

The only recent one-off asset-based tax was in Ireland, where a temporary pensions levy was introduced from 2011 to 2015.

It was 0.6% of pension fund assets, payable for each of the four years 2011 to 2014 and an additional levy of 0.15% for 2014 and 2015. Therefore, in 2014 the levy increased to 0.75% and in 2015, the levy was 0.15%. The levy was based on the market value of the pension fund on 30 June each year. There is thus a precedent for collecting tax from pension funds. In addition, a statutory instalment payment scheme is recommended for those who have insufficient liquid funds to pay the tax.

The final area covered is valuation, where the authors bravely assert that HMRC’s valuation office would be able to value more than 8 million properties if the tax were to have a wide impact.

They compare the valuation process for inheritance tax – although the issues with valuing about 25,000 estates are not really comparable to something of the scale of a broad-based wealth tax.

Will it happen?

The initial feedback rather suggests that a tax affecting over 8 million individuals is highly unlikely – mainly because at the broad level of £500,000 most people’s wealth is tied up in their home and their pension. The challenge with introducing such a tax at a much higher level, excluding homes and pensions, is whether the yield is worth the complexity. This report from Dr Arun Advani, Dr Andy Summers and Emma Chamberlain is an excellent attempt to shine a light on all the issues of asset-based taxes.