Countdown to MTD for VAT

Share this article

Neil Warren answers some key questions about the new MTD regulations that will apply to most VAT registered businesses from April 2019

Key Points

What is the issue?

MTD represents a major change in procedures for many VAT registered businesses. It is important to be clear about what is required after April 2019 and which businesses will be included and excluded from the regulations.

What does it mean to me?

It is important to understand which records need to be kept in a digital format and also the figures to record, e.g., what figures must be digitally recorded from sales and purchase invoices.

What can I take away?

The article considers various quirks with the new rules – for example, it is not acceptable for a business to batch sales and purchase invoices into one MTD entry based on a statement or payment total – each invoice needs to be recorded in a digital format. And retailers must digitally record their daily gross takings figures but not the individual transactions that make up these totals.

What is the starting date for MTD?

MTD takes effect for VAT periods beginning on or after 1 April 2019 for most VAT registered businesses. This means, for example, that a business with quarters ending February, May, August and November must join MTD on 1 June 2019. However, about 3.5% of the VAT registered population with more complex VAT affairs will not join until periods beginning on or after 1 October 2019. This list (not exhaustive) includes trusts, VAT groups or divisions, payment on account businesses and those that use the annual accounting scheme.

Must all VAT registered businesses join MTD?

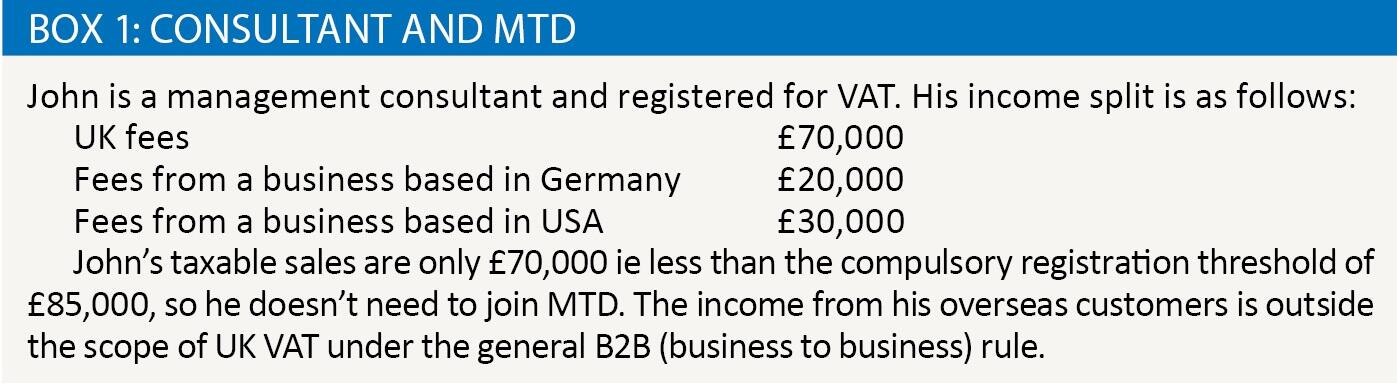

A business that is voluntarily registered does not need to join MTD, i.e., those registrations with annual taxable sales of less than £85,000. Income that is either exempt from VAT or outside the scope is excluded from the calculations – see Box 1. However, voluntary registrations must monitor their taxable sales on a rolling 12-month basis after April 2019 and if this figure exceeds £85,000 at any time, they must join MTD from the beginning of their next VAT period. Don’t forget that it is the responsibility of the business owner to identify his MTD joining date.

Can a business ever leave MTD once it has joined?

If a business has to join MTD because of a temporary boost to taxable sales which takes it over the £85,000 limit, it cannot leave again even if sales fall below £85,000. To quote a much-used phrase in recent months: ‘Once you’re in, you’re in for good.’ The only exit route will be when the business eventually deregisters.

A business can adopt either a full accounting software package to digitally prepare its returns or use spreadsheets. Does HMRC have a favoured option?

No – it is up to business owners to decide the format of their digital record keeping. The key point with spreadsheets is that bridging software will be needed to link the spreadsheet totals for, say, input tax and output tax, to the VAT return submission process (Notice 700 /22, para 3.2.3). The aim of MTD is for minimal human intervention in the whole accounting process, which HMRC controversially thinks will reduce VAT errors made by a business and increase the tax yield.

What records will need to be kept in a digital format?

It is important to identify the first document in an audit trail that needs to be kept in a digital format. For example, there is no need for a retailer (e.g. a coffee shop) to digitally record every sale that is made to a customer but it must record its daily gross takings figures in a digital format. And there is no need for an invoice-based business to raise its sales invoices electronically (a handwritten invoice is fine) but each invoice must be digitally recorded. Purchase invoices must also be recorded digitally unless a business uses the flat rate scheme (FRS). FRS users only need to digitally record purchase invoices where input tax is being claimed, i.e. spending on capital goods costing more than £2,000 including VAT (Notice 700 /22, para 3.6). Many businesses make VAT adjustments e.g. for partial exemption or the capital goods scheme – these adjustments can be calculated using any method (including a hand-written schedule) but the total must be entered into the digital system, e.g. by journal.

What information from sales and purchase invoices needs to be recorded digitally?

Purchase invoices

It is necessary to record the total value of the invoice excluding VAT and the input tax being claimed. There is no need to digitally record transactions that are excluded from the VAT return, e.g. wages paid to employees.

Example: John is VAT registered and buys a business book for £50 (zero-rated) and some business stationery for £60 plus VAT on the same invoice. He must digitally record the net total figure of £110 and the input tax being claimed, i.e. £12.

Reference: Notice 700 /22, para 3.3.3.

Sales invoices

The net figures subject to different rates of VAT must be recorded as well as the rate of VAT being charged.

Example – A wholesaler raises a sales invoice to a retailer for zero-rated cheese (£50) and standard rated wine (£60 plus VAT). The wholesaler will digitally record the net figures of £50 and £60 and the VAT rates that applies to these amounts, i.e. ZR and SR (0% and 20%).

In the case of both sales and purchase invoices, the processing date will be the invoice date unless the business uses the cash accounting scheme, when the payment date is adopted. Reference: Notice 700 /22, para 3.3.3.

Is it acceptable to digitally record total amounts paid and received by a business, e.g. a customer might pay six invoices within one payment so making one entry instead of six will save time?

This is potentially the biggest record keeping change for many small business owners, namely that each individual sales or purchase invoice must be recorded in a digital format. It is not acceptable to batch invoices together and make one entry based on a payment or statement total. HMRC would argue that this requirement has always applied but the practical reality is that many businesses using the cash accounting scheme have kept records based on payment totals.

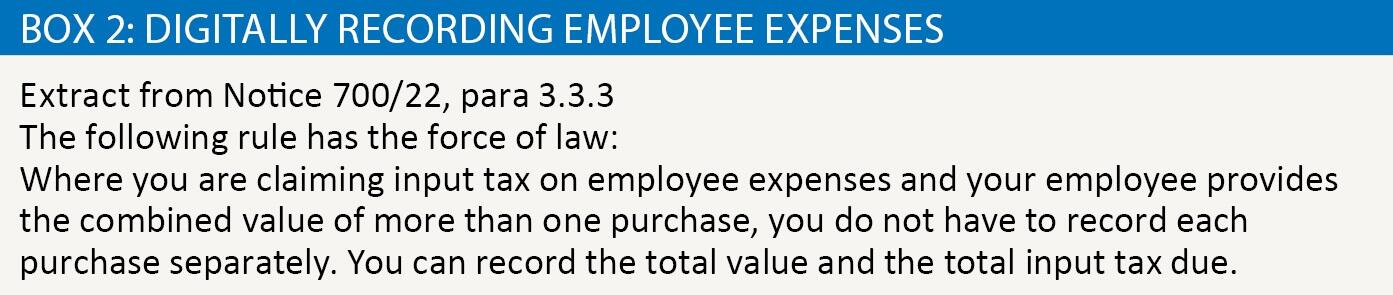

Must all purchase invoices and receipts be recorded digitally, even small amounts like meal and petrol receipts on an employee expense claim?

The good news is that there is a potential escape clause in the regulations that a transaction does not need to be recorded digitally if this would be ‘impossible, impractical or unduly onerous.’ HMRC has confirmed this would apply to employee expenses – see Box 2.

How will VAT returns be submitted to HMRC?

Voluntary registrations will continue to use the Government Gateway but businesses involved with MTD will have to submit their returns through HMRC’s API (Application Programming Interface) platform. An aim of MTD is that the business owner will be able to view the nine boxes of the VAT return displayed on his accounting software and, if he is happy with the figures, will just press the send button to submit the return, i.e. making a digital exchange with HMRC. It is important to remember that HMRC still only receives the totals from the nine boxes on the return.

What involvement can agents have in the VAT return process?

Many clients will be happy to directly submit their returns to HMRC using their own accounting software (or bridging software with spreadsheets) with no agent involvement. Another option is for the client and agent to set up a cloud-based arrangement, giving the agent the opportunity to check the return before it is submitted by the client. This option also shows that reasonable care has been taken to prevent errors if there is a potential penalty situation. Alternatively, the client could transmit data to the agent via a digital link (which includes a USB stick), and then the agent checks the return and submits it via his own software and his agent account with HMRC (Notice 700 /22, section 6).

Finally, what does it mean when HMRC talk of a ‘soft landing’ period for penalties in the first year of MTD?

HMRC recognises that the biggest challenge for some businesses will be to establish digital links between different parts of an accounting system.

HMRC has said that there will be no penalties issued until VAT periods beginning after April 2020 if a business does not have digital links in place between different parts of its accounting system and uses, say, cut and paste to create those links.

For businesses with more complex VAT affairs which do not join MTD until periods beginning after 1 October 2019, the soft-landing period runs until 30 September 2020.