Cry to let

Share this article

Matt Parfitt and Ian Brewer consider the impact of recent changes to income tax and SDLT/LBTT on residential landlords

Key Points

What is the issue?

Residential landlords are impacted by changes to both income tax and SDLT (LBTT in Scotland) but the new rules come with some quirks that have a wider impact than the headline announcements suggested.

What does it mean to me?

It is important for landlords and their advisers to understand the full impact of the new legislation. Residential property purchasers, and their lawyers, also need to mindful of some unexpected pitfalls.

What can I take away?

It’s not just higher-rate tax paying landlords who are impacted and there are some important questions to be faced by potentially anyone investing in a property, even as their main residence.

Landlords could be forgiven for perhaps feeling a little persecuted by the government of late. With the double whammy of the recently introduced higher SDLT and land and building transaction tax (LBTT) rates for purchases of additional residential properties and the upcoming changes to income tax relief for finance costs, Buy To Let properties are possibly no longer quite the investment that they have been over the past couple of decades, and that is apparently the government’s intention behind these policy decisions.

On top of this, there are some strange and arguably harsh consequences of both the income tax and SDLT changes and which appear to impact a wider audience than originally intended or explained; and what about the impacts on the private rental market for exactly those whom these changes seek to protect?

Income tax

Changes are being introduced to the income tax relief on property finance costs (e.g. mortgage interest payments) such that relief will be restricted to basic rate only. However, this isn’t just a case of limiting the level of relief but also involves a fundamental change to the method of obtaining relief, as no deduction will be allowed for finance costs when calculating taxable property income and, instead, the resulting tax liability can be reduced by the basic rate (20% currently) of the finance costs.

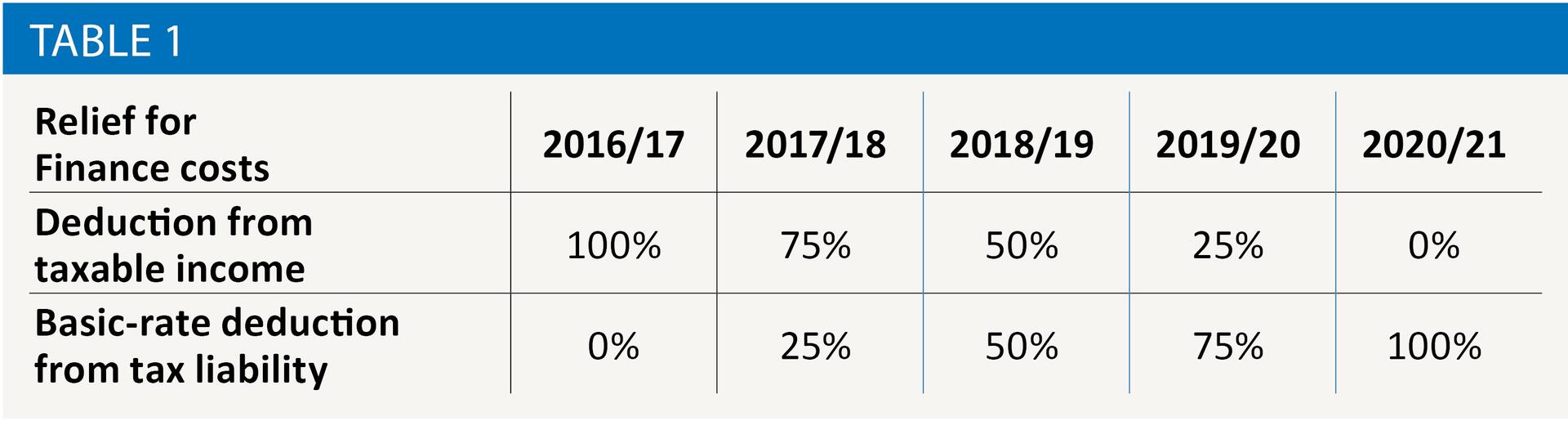

The changes are being phased in from 2017/18 such that relief for finance costs is split between the existing and new rules until 2020/21, when only the new rules apply. Table 1 shows how this phasing-in will apply.

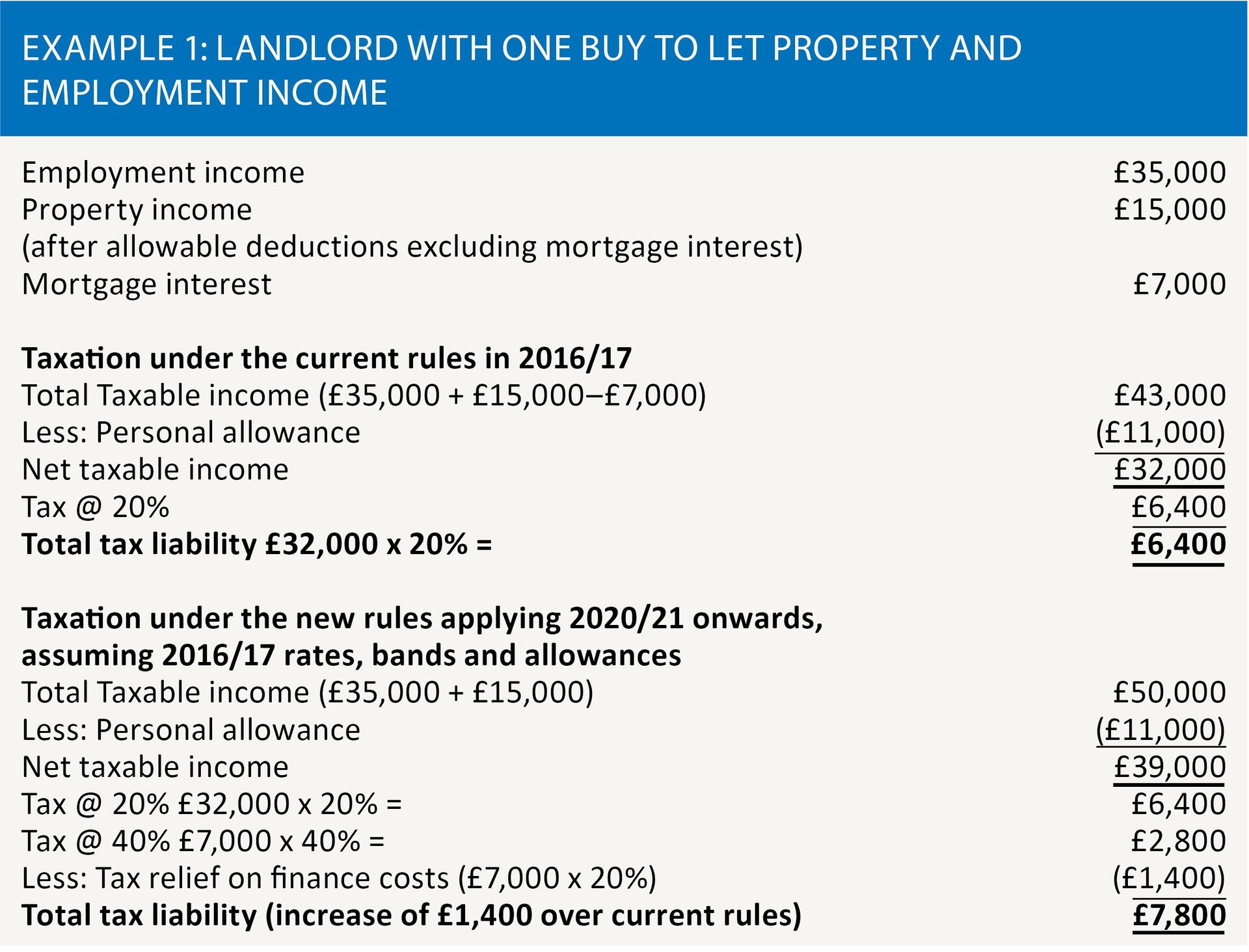

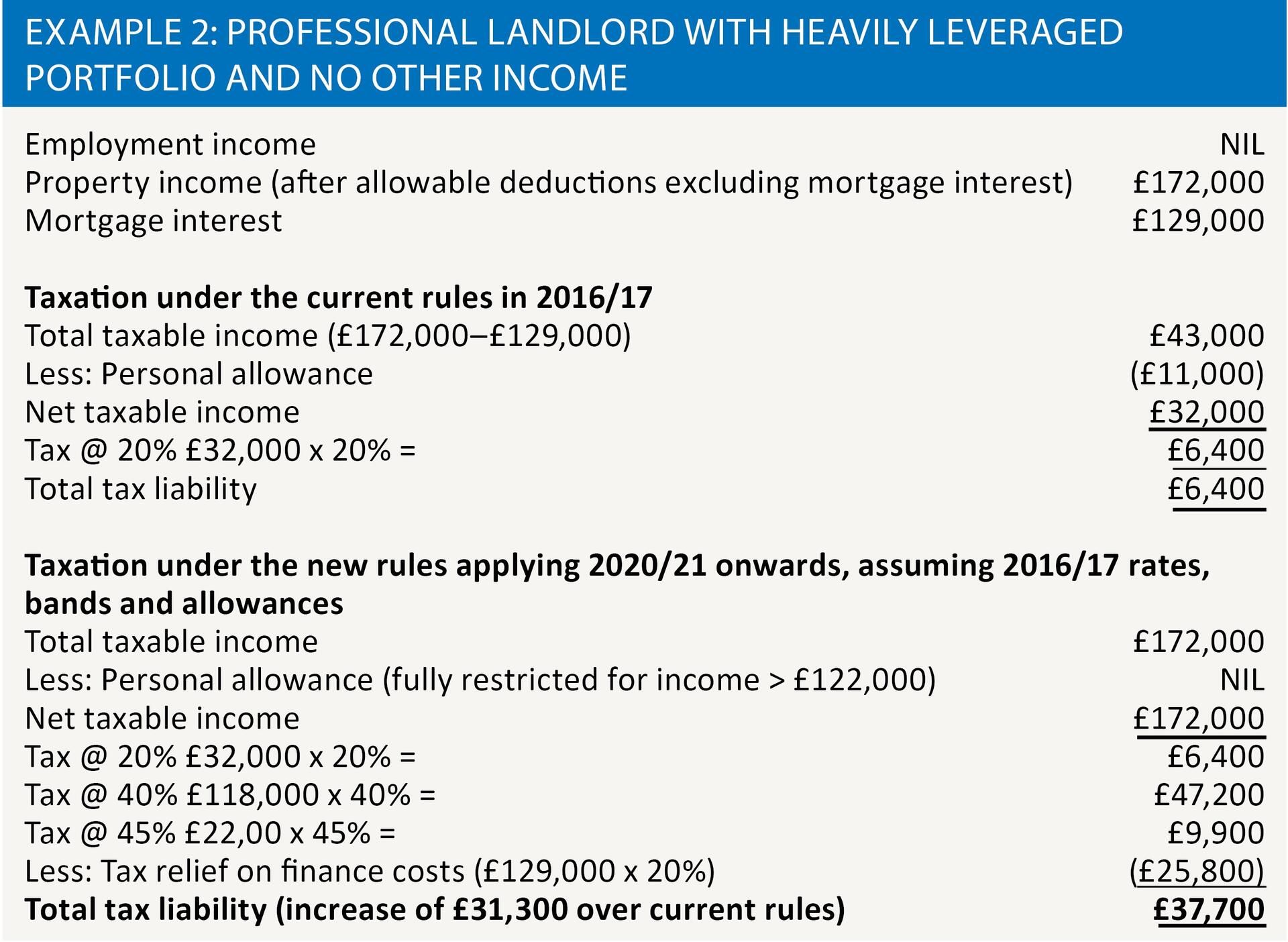

Clearly, most (not all, as those without mortgages are far less likely to be impacted) higher rate tax paying landlords will incur increased tax liabilities as a result but a potentially overlooked impact of the new rules is that they don’t only affect higher rate payers, even though this is how they were described when announced. Example 1 shows how it’s possible for a basic rate tax payer to be pushed into the higher rate as a result and Example 2 shows a particularly penal example of this, for a landlord with no other income and with a portfolio of heavily leveraged properties.

There could be other impacts for landlords: higher total taxable income (due to finance costs not being deducted) may lead to a high income child benefit charge, reduced tax credits, personal allowance restriction for incomes over £100,000, etc.

If looking for a silver lining then landlords may appreciate the reminder that certain finance costs can obtain relief at all, e.g. mortgage arrangement fees, early repayment fees and interest on a loan taken out to purchase furniture. A reminder that the capital repayment element of mortgage payments cannot obtain any relief may be helpful for some landlords. We have come across landlords who were unaware of one or both of these points.

Wear and tear

Landlords of furnished properties have also received further bad news in the loss of the wear and tear allowance. The flat 10% deduction from net rental income (not including any payments that are the responsibility of the tenant, e.g. council tax, but paid by the landlord) is no longer available with effect from 6 April 2016 and landlords can now only deduct only the actual costs incurred of replacing furnishings. Note that the initial cost of purchasing furnishings cannot be deducted.

SDLT and LBTT

Juliet Minford, in her article ‘An extra layer of complexity’ in the July edition of Tax Adviser, discussed the 3% surcharge now applicable to both SDLT and LBTT for purchases of additional residential properties. Clearly, this is a factor that may impact the decision of a landlord to expand their portfolio or for one to make an initial foray into the buy to let market, and such investors would be well advised to familiarise themselves with the points raised in Juliet’s article.

This article is not intended to cover old ground by repeating the aforementioned article, so we will instead attempt to draw out some of the key quirks that are perhaps surprising or inequitable in these new rules.

- A buy to let landlord living in rented accommodation or with parents and purchasing a new property as their main residence will have to pay the surcharge, but a buy to let landlord who is replacing their main residence will not.

- A parent helping a child to purchase their first home by way of a joint purchase will result in the surcharge being due on the entire transaction (not just the parent’s share) unless the parent (and their spouse or civil partner) owns no other residential properties. A gift of money for a deposit will not trigger the charge, though there could be IHT implications to consider.

- Annexes – colloquially, ‘granny flats’ – attached to one dwelling and which constitute a separate dwelling will now (since recent amendments to FB 2016) subject a transaction to the 3% SDLT surcharge only if the consideration apportioned to the annex is over a third of the total consideration for the transaction and also over £40K in its own right. The rules are slightly more complicated where there are three of more dwellings involved. This is a welcome relaxation to the original proposals but, at this time, LBTT has not applied a similar relaxation.

- Transfers of equity are particularly complicated. Although spouses and civil partners are treated as a single unit for SDLT purposes, cohabiting unmarried couples are not. If an unmarried couple occupy a property together which is owned solely by one of them, a subsequent transfer of equity into joint names will not be a problem if there are no other properties in the background, but what if the other partner still owns another property, perhaps having let this out when they moved in with their partner? In this instance, if the property is subject to a mortgage then a lender would normally insist on the new partner being added to the mortgage and there would then be deemed consideration equal to their half share of the mortgage balance. If the couple instead decide to sell their current home and enter into a new purchase jointly then the surcharge would still apply as one of them owns another property but is not disposing of their main residence, even though their main residence is being sold and hence being ‘replaced’. However, see below for a discussion on joint tenants and for LBTT consideration.

If the surcharge applies then it is in effect an additional 3% due on the entire consideration for the transaction, so this can be particularly costly.

Joint tenants: a way out?

We highlighted earlier the complications of a joint purchase or transfer of equity into joint names, where one of the purchasers has another property lurking in the background. In the case of a transfer of equity subject to a mortgage, the surcharge will be due if the mortgage balance is over £80,000 as the new party is effectively taking on debt above the £40,000 SDLT de-minimis; note that any actual money changing hands would also constitute consideration for the transfer. For an outright purchase, the entire transaction price (not just half) will instead be relevant. In either case, this is assuming a purchase as joint tenants, where both individuals equally own the entire property under law.

However, what about a purchase as tenants in common, where a property is split into distinct parts and each party purchases a different part? If either party’s share were worth under £40,000 and it were that party who owned another residential property then one might expect the surcharge to not apply. However, the legislation refers to the consideration for the transaction being £40,000 or more so it follows that the surcharge will apply to the entire transaction.

It’s less clear for transfers of equity subject to a mortgage. Lenders would normally insist on both/all parties becoming jointly and severally liable for the mortgage, rather than it being split according to the value of each’s share, but if a lender were to agree, for example, a 90:10 split of a mortgage debt to match a 90:10 joint tenant split of a property then the debt taken on in consideration by the minor part-owner would only be the 10% of the mortgage. We are not aware of any lenders currently allowing this arrangement, however, but maybe this will change in the future.

Devolution or convolution?

LBTT is the devolved Scottish equivalent of SDLT. SDLT and LBTT are not aligned and so it is important to understand the differences that could be relevant depending on which side of the border a property is located. Other than differences to the rates and bands, these include (but are not limited to) the following:

- The treatment of annexes, as discussed earlier;

- Cohabiting partners are treated as a single unit for the purposes of LBTT, but not for SDLT;

- The timeframe for a refund of the surcharge if a main residence is sold after the purchase of a new one is 36 months for SDLT but only 18 months for LBTT;

It will also be interesting to see what approach is taken in Wales when the devolved Land Transaction Tax comes into effect, expected April 2018.

Whether a similar surcharge will be introduced and how this will operate is currently unknown but could add a further layer of complexity.

The impending ‘Brexit’ following the recent EU referendum may also be relevant as this could lead to an independent Scotland (and possibly Wales and/or Northern Ireland); there is even talk of an independent London being a possibility. As a consequence, rules on land taxation and also income tax may diverge further, although it is far too early to speculate on what will actually happen.

Incorporation

With companies being able to obtain a deduction for mortgage interest costs then could incorporation be the magic bullet? The tax issues related to incorporation and the ongoing taxation of companies are too numerous and complex to address in this article but if considering incorporation then it’s worth bearing exactly this in mind – it’s complex.

Corporation Tax (CT) is dropping to lower than even the basic rate of income tax, and there is no restriction on the deduction of finance costs, but profits still need to be extracted and taxed as income, a matter complicated by changes to dividend taxation. Corporates also pay CT on chargeable gains at different rate to CGT for individuals, will get indexation for inflation but no annual exemption or PPR and letting reliefs.

Other issues like incorporation and disincorporation may also need to be considered.

Add to these the administration challenges and the fact that SDLT/LBTT will be due on the market value of property on initial gift into a company by a connected party and one may decide it’s not worth considering further.

Partnerships and LLPs are another option and there has been talk of using these as an intermediate step before incorporation in order to avoid the connected party market value SDLT charge on property transfer. Any such planning would need to be mindful of the SDLT anti avoidance provisions and, in the case of LBTT, the Scottish General Anti Avoidance Rule.

Parting words – first time buyers and renters?

There has been talk of landlords putting up rents in order to offset the cost of the tax changes and it remains to be seen whether this will happen or if the economics of supply and demand prevents this. Although the government has introduced these tax changes in an attempt to rebalance the housing market more in favour of first-time buyers, it is perhaps yet possible that these same persons find it harder to get onto the housing ladder in the first place if renting becomes a more expensive option; lower income families without any aspiration to own their own homes could also be worse off.

In summary, landlords may not have seen the end of tax changes targeted at them but, with so many quirks in the rules, it’s not just landlords who need to be wary of these. It may also be interesting to see any new case law applicable in these areas.

Further information

Read Juliet Minford’s article on the extra layer of complexity introduced by the extra 3% SDLT/LBTT.