Errors and emissions

Share this article

Matt Parfitt considers the potential pitfalls of providing company cars and fuel

Key Points

What is the issue?

The company car benefit in kind (BIK) rules, as published in ITEPA 2003 Pt 3 Ch 6, are largely based on CO2 emissions and the rates are on an upward trend. There are various potential pitfalls for company cars and fuel and the recent VW emissions scandal and possible changes to emissions testing might have a large impact on employees’ BIKs.

What does it mean to me?

As an employee, it is important to consider the impact of CO2 and future rate rises when deciding whether to take a company car and which model. As an employer, there are some tricky areas and it is crucial to understand the tax implications of any offering. Advisers need to be prepared to look at both sides – there is a big opportunity to assist clients in this complicated and often emotive area

What can I take away?

There are some simple tax planning points, particularly on private fuel and cash allowances. Also consider car ownership schemes. If nothing else, understand the current regime, be aware of future changes to rates and the possible impact of the VW scandal

The company car rules determine the annual value of the benefit to be calculated as being the manufacturer’s vehicle list price (with some special rules for accessories) multiplied by a percentage based on the fuel type and published CO2 emissions. If private fuel is also provided, there is an additional annual BIK equal to a scale rate charge (currently £22,100) multiplied by the same percentage. There is no deduction available for any costs reimbursed by the employee unless they make good the entire cost of private fuel in a tax year.

A potential criticism of the rules is that the taxable value of a company car BIK does not match its economic value, so an employee could be taxed on an amount wildly different from what it costs the employer to provide the vehicle. This is mainly because of the role that CO2 emissions play in the calculation and is presumably an example of the government attempting to use the tax regime to influence behaviour by encouraging the use of greener cars, although this focuses purely on CO2 and ignores other emissions. In addition, the BIK is not reduced for older cars and this may discourage their use, potentially flooding the market with older, often higher-polluting vehicles.

Supporters of the rules might suggest they provide an incentive for employees and employers to choose greener company cars. However, the result is a distortion such that it could be cost-effective to choose a low-emission vehicle as a company car; but for higher-emission cars, it can be more cost effective for an employee to take a cash allowance – if offered by their employer – and buy or lease privately. In such a situation all the rules achieve is to discourage company cars over private arrangements.

Since vehicle tax is also calculated on emissions, it is arguably unfair to penalise employees with higher BIKs as well as the vehicle tax and corporation tax implications – restricted deductions for high-CO2 car lease costs, and capital allowances also being based on CO2 – because in reality the government is getting three slices of the pie. This may be especially true if employers calculate the whole-life cost of a vehicle – taking into account vehicle tax and corporation tax, as well as purchase or lease costs and maintenance – when deciding whether to offer it in the fleet and at what ‘price’ to employees.

Further, employees can be limited by their employer on the choice of vehicles available to them, although there has been a move towards greener fleets in recent years and this is itself perhaps good evidence of the BIK rules having their intended effect.

A warning on fuel

The high value and ‘all or nothing’ nature of the fuel BIK is highly punitive and not financially worthwhile, except for employees undertaking very high private mileage. It seems clear that the government does not like fuel to be an employee benefit and keeps hiking the scale rate charge ever higher each year. For all but the highest mileage drivers, private fuel is no longer a cost-effective benefit and employers offering this would be advised to rethink whether there is a better way to structure their offering, perhaps by removing private fuel and offering cash allowances.

It is also worth noting that, for business mileage undertaken in a company car, there are advisory fuel rates published quarterly by HMRC that determine the maximum employees can be reimbursed. These rates are intended to equate roughly to the actual cost of fuel per mile depending on the fuel type and engine size. Paying higher rates than this for business mileage would also be seen as giving rise to a fuel BIK.

Cash allowances and AMAPs

It is common for employers to offer a cash alternative for employees who do not wish to take up the option of a company car. These employees are often restricted as a matter of company policy to claiming lower business mileage rates in their own vehicles – such as the same advisory fuel rates as company car drivers.

However, legislation permits employees undertaking business mileage in their own car to claim approved mileage allowance payment (AMAP) rates – currently 45p a mile – free of tax and National Insurance (NI). This is intended to cover the cost of normal wear and tear of the vehicle as well as the cost of fuel. Employees who use their own car for business mileage and are reimbursed by their employer at lower than AMAP rates can claim tax (but not NI) relief on the difference between the two rates.

Employees taking a cash allowance pay tax and NI on this and their employer also pays NI, but if business mileage is reimbursed at lower than the AMAP rates these potential tax- and NI-free payments are not being fully used. Therefore, it would be more cost effective for both parties that the employer instead paid the full AMAP rates for mileage and lowers the cash allowance accordingly. This is a common planning point and one that also saves employees from having to claim tax relief on the difference between what they receive and the AMAP rates, but many employers surprisingly overlook it. Who knows how many employees know about this, let alone take the time to claim?

The road ahead

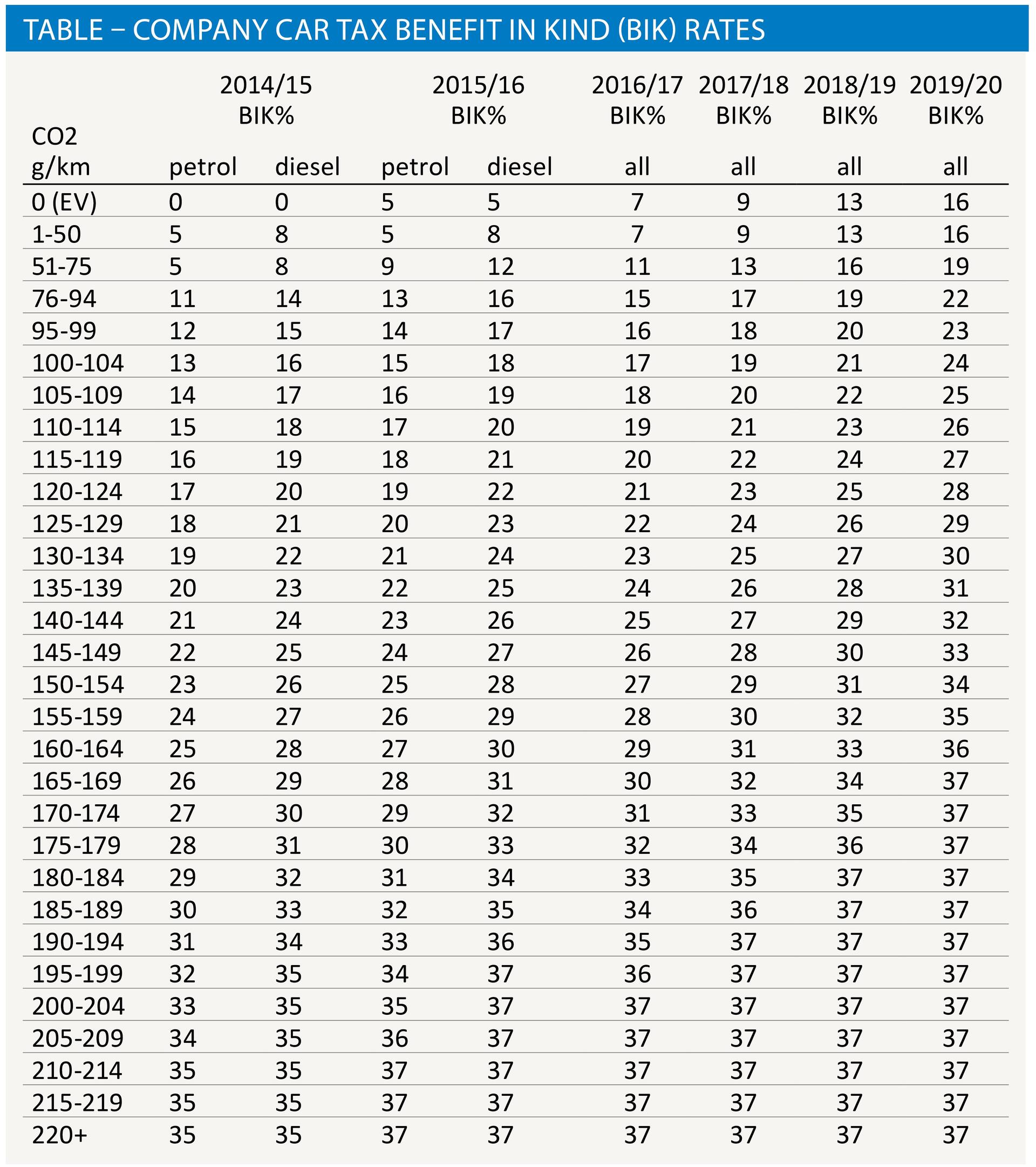

In recent years, the percentages applicable to CO2 bands have been raised significantly and this trend is expected to continue, with preliminary rates until 2019/20 already confirmed. Although this encourages the choice of greener vehicles, it is continually making company cars a less attractive benefit unless manufacturers can keep up and improve the efficiency of engines at the same rate.

The strange part is that zero-emission vehicles, which had a 0% charge until 2015/16, and others with particularly low CO2 are suffering significant rises in the BIK percentages and at much higher rates than the higher CO2 bands. This is counter-intuitive because it is decreasing the incentive for cleaner cars. With percentages rising quickly, it seems either the government is trying to discourage the use of company cars for no obvious reason, or is trying to cash in by raising revenue from what is a popular benefit, but which may not be in future if this trend continues.

Diesel cars currently come with a 3% supplement to the BIK percentage over petrol cars. This was set to no longer be the case from 2016/17 but, in the Autumn Statement, George Osborne announced that this would be retained until April 2021.

The percentages applicable to each CO2 band and how these are expected to rise are illustrated in the Table.

Car ownership schemes

A car ownership scheme is an alternative way for an employer to structure its arrangement such that the vehicles are not considered company cars and BIK would not apply. This would normally involve a car being provided through a credit sale agreement, transferring ownership of it to the employee, with a corresponding cash allowance paid to them to keep it cost-neutral.

HMRC accepts these types of schemes under particular conditions, although they can be administratively complicated. However, with rising company car BIKs, these may become more common if they are seen as a cost-effective alternative.

Volkswagen scandal

We have already heard that the 3% diesel BIK surcharge is to be extended, in light of the VW emissions rigging scandal and the negative publicity that diesel engines have received as a result.

‘Emissions-gate’ may yet prove to be further relevant, especially in light of the revelation that CO2 emissions were understated as well as nitrogen oxide levels. Might this lead to retrospective higher BIKs for employees driving these models, who may have chosen them in good faith based on their expected costs and tax consequences? One would expect VW to foot the bill if so.

There is talk of more reliable ‘real world’ emissions testing being introduced, perhaps from September 2017, and it will be intriguing to see how this affects BIKs and whether it merits a rethink over the CO2 bands. There may even be potential for a move away from a tax regime based purely on CO2, which could further shape the future for company car schemes.