Curiouser and Curiouser

Share this article

Robin Williamson considers the curious interactions between tax and social security benefits like the state retirement pension

Key Points

What is the issue?

The way in which social security benefits like the state retirement pension are taxed, and interactions within the social security system itself, is a highly complex subject in itself, and one in which neither HMRC nor the DWP has particular expertise.

What does it mean to me?

Many clients of tax advisers may be in receipt of certain benefits at certain times in their lives, such as tax credits when working or bringing up children, or the state pension when retired. The adviser who has a working knowledge of how they are taxed can offer these clients a better service.

What can I take away?

Apart from the basic rules there are specialist areas, such as the taxation of social security lump sums and the mechanics of simple assessment, with which advisers on personal taxation should become familiar.

Practitioners may occasionally be called upon to advise clients on how welfare benefits they receive are treated for tax purposes. Some might argue that social security is not within the province of a tax adviser, but those who wish to provide a complete service to their clients in respect of their financial affairs may wish to equip themselves at least with a basic knowledge. After all, anyone can experience a change in circumstances that might necessitate claiming a working-age benefit, and most people will claim retirement benefits such as the state retirement pension at some point in their lives (if they do not, their spouse or civil partner might need to claim bereavement benefits on their death before retirement age).

The task is a difficult one because taxation of social security benefits has its own form of complexity, occupying a sort of limbo between the functions of the Department for Work and Pensions (DWP) and HMRC, with neither department being fully conversant with the subject. The rules on how benefits, both taxable and non-taxable, interact with each other form another complicated labyrinth.

This and a subsequent article aim to set out some basic principles on how the tax and social security systems interact, before looking in more detail at some common benefits such as the state retirement pension and bereavement benefits, and to indicate possible sources of more information.

Broad principles

As a general rule, benefits that are based on national insurance contributions (NICs) are taxable, those that are income-based or means-tested are not. Also, as a rule of thumb, taxable benefits are counted as income for tax credits purposes, potentially reducing the recipient’s award, whereas non-taxable benefits are generally disregarded. There are a few exceptions to this general rule – for example, income-based jobseeker’s allowance is taxable but is disregarded for tax credits.

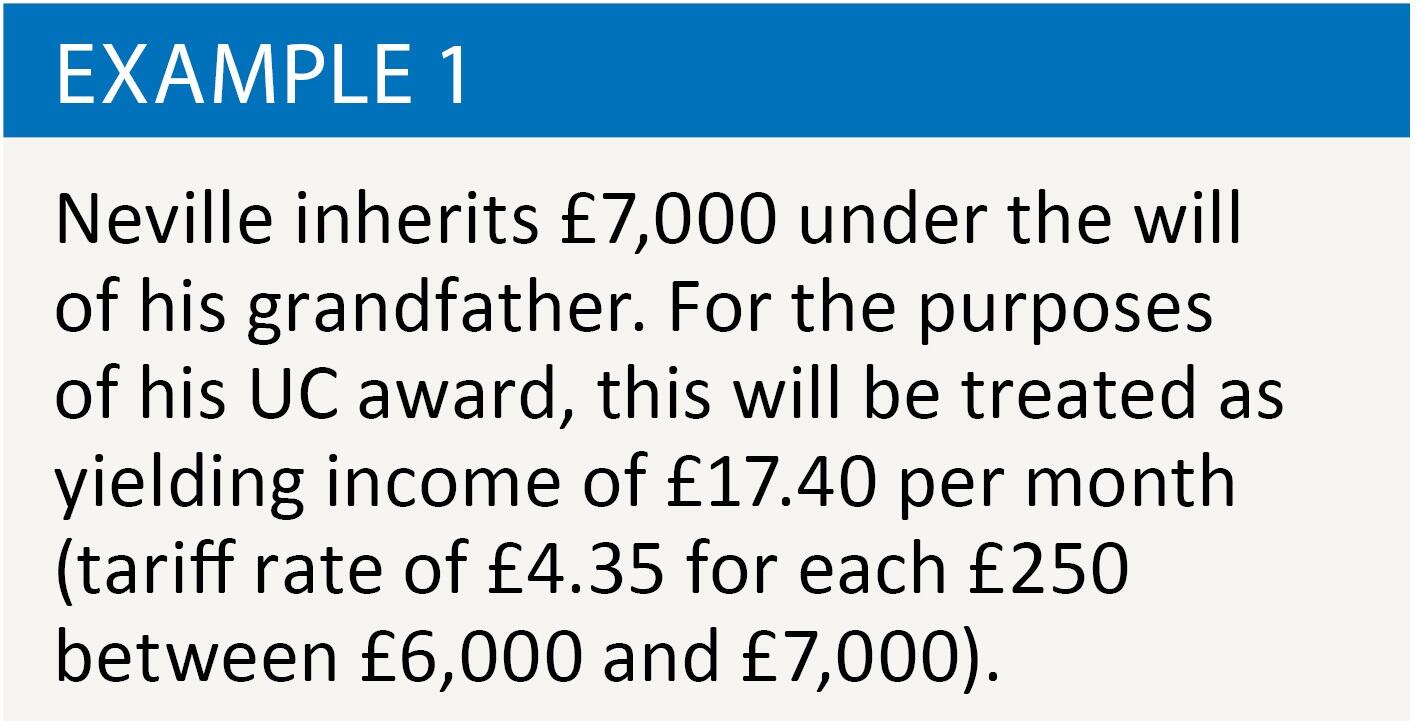

As tax credits are gradually being phased out in favour of universal credit (UC), different rules will apply as most benefits are treated either as capital or as unearned income for UC purposes. If capital, the amount received is added to other capital and if the total comes to more than £16,000, there is no entitlement to UC; if between £6,000 and £16,000, £4.35 is added to monthly income for each £250 or part thereof in excess of £6,000. Capital below £6,000 is disregarded. See example 1.

If the benefit payment is treated as unearned income, it will reduce the UC award pound for pound.

Some benefits – such as free school meals, free prescriptions, etc – are receivable ‘in kind’ and are known as ‘passported benefits’ because mainstream benefits payable in cash act as passports to them. For example, receipt of state pension credit entitles the recipient to a range of passported benefits, including certain types of help with housing costs and council tax, free NHS dental treatment, help with the cost of glasses or travel to hospital and cold weather payment.

Most means-tested benefits (but not tax credits) are calculated on the basis of a person’s net income after tax. Consequently, if a person’s net income rises – for example because their personal allowance is increased – their entitlement to means-tested benefits goes down. Take UC, for example. If a claimant’s net income is increased by £100 because the personal allowance goes up by £500, thus notionally saving them £500 x 20% = £100 in tax, their UC award will be reduced by 63p for each £1 of the increase. The claimant’s actual gain from the increase in the personal allowance will therefore be £37, not £100.

It is of course possible for an increase in income to make a benefit claimant worse off. For example, a single individual whose weekly net income is £158 can claim guarantee pension credit which will top up their income to £159.35 a week and give them access to the range of passported benefits discussed above, but if that individual’s income goes up to £161 per week they would lose both their guarantee pension credit and some of the passported benefits that went with it (assuming for this purpose that the claimant is not entitled to the savings element of state pension credit).

There is a brief commentary on various social security benefits on the LITRG website setting out whether they are taxable or non-taxable and how they are treated for tax credits and universal credit purposes. The legislation that prescribes the tax status of social security benefits is in ITEPA 2003 Pt 10, with a table of taxable benefits at s 660 and exempt benefits at s 677.

Tax credits and universal credit

Working tax credit (WTC), child tax credit, child benefit and UC are all non-taxable. Extensive material on these benefits, mainly for advisers, is to be found at www.revenuebenefits.org.uk.

A point to note is that while tax credits are still payable in many areas, universal credit is gradually being introduced postcode-by-postcode. There is a tool on the revenuebenefits site which enables one to check whether a particular postcode area is one in which universal credit is being rolled out.

While there is no upper age limit on who may claim WTC, the upper age limit for UC in full service areas is the age at which one may claim state pension credit. In the case of a joint claim by a couple one of whom is below and one above that age, currently they may choose whether to claim UC or state pension credit. In the future, mixed age couples will have to claim UC. This means that under UC there is no in-work benefit that those past retirement age can claim.

State retirement pension/state pension credit

The state retirement pension (SRP) is taxable. Although it comes as a surprise to some recipients, in this respect it follows the pattern of other contribution-based benefits (SRP is dependent on the recipient having paid or been credited with NI contributions for at least 10 years, while maximum SRP is payable to those with a contribution record of at least 35 years).

State pension credit is a means-tested benefit which tops a single person’s income up to a minimum of £159.35 a week, or £243.25 for a couple, and is non-taxable. It may include a savings credit element which is payable to those who attained state pension age before 6 April 2016 and who had income higher than the basic SRP. The savings element yields £13.20 extra a week for a single person, £14.90 for a couple.

PAYE on the state pension

While the SRP is taxable, the method by which it is taxed is complex and, like many complex things in taxation, can go wrong. This stems from the fact that the payer, the Department for Work and Pensions (DWP), unlike other pension payers, does not operate PAYE on the SRP. Nor, despite the best efforts of both LITRG and the Office of Tax Simplification, do they provide an end-of-year certificate such as a P60. HMRC therefore must do their best to collect the tax due on the SRP either through an existing PAYE code, or through self-assessment, or by simple assessment (on which see more below).

Tax on the SRP is generally accounted for through PAYE by reducing the pensioner’s tax-free amount by the amount of the SRP. In some cases this gives rise to the dreaded ‘K-code’ where the SRP exceeds the balance of allowances available and the excess is treated, for PAYE purposes, as taxable extra income.

The main problem with PAYE is that the SRP generally starts to be payable part way through a tax year, but HMRC include a full year’s state pension in the code, requiring the employer or pension-payer to use a week 1/month 1 code unless the taxpayer intervenes to ask for the actual amount of the SRP receivable to appear in the code. Less frequently, the automatic process whereby the DWP notify HMRC of the SRP about five weeks before it becomes payable may not work and HMRC are wholly dependent on the taxpayer to notify them. If there are several sources of income, for example an SRP plus one or two occupational or personal pensions, there may be confusion as to which source the personal allowance should be deducted from, and it is not uncommon for the allowance to be deducted twice or not at all. It will be seen how easily an underpayment or overpayment may arise, and it is generally a wise precaution for the pensioner or their adviser to keep in close touch with HMRC, particularly in the early years of receiving the SRP, to ensure that such mistakes do not arise.

ESC A19

As one would expect, if an adviser is involved the PAYE coding generally collects the right amount of tax on the SRP. Things more often go wrong if an unrepresented pensioner, baffled by the obscurity of the coding system, simply disengages and hopes that everything will work out correctly. If an underpayment arises year after year, and the taxpayer can successfully argue (a) that HMRC failed to make timely use of information they had about the taxpayer and (b) that it was reasonable for the taxpayer to believe that their affairs were in order, HMRC should agree to write off any arrears of tax that accrued in a tax year ending more than 12 months earlier. Many tax advisers have mounted successful A19 challenges when consulted for the first time by a pensioner with an underpayment of tax and the charity Tax Help for Older People has built up considerable expertise in the topic. A series of guides and precedents is available on the LITRG website.

Simple assessment

Sometimes there are insufficient sources of other PAYE income for the SRP to be fully taxed via the code. Until recently, the only way to collect the tax due on the SRP in such cases was through self-assessment. This was a cumbersome and expensive way for HMRC to collect what were often very small amounts of tax.

Accordingly, FA 2016, section 167 and Sch 23 introduced an administrative procedure called ‘simple assessment’ for which the legislation is now contained in TMA 1970, sections 28H et seq. It is HMRC’s intention that this procedure should obviate the need for people who owe some tax on their SRP to file a self-assessment return where there is insufficient PAYE income for the tax on the SRP to be collected through PAYE.

Under simple assessment, HMRC will use information in their possession to issue an assessment of income tax and capital gains tax (or balance thereof) payable by the individual for the relevant tax year. A notice of simple assessment must be served under TMA 1970, section 30A and must contain details of the income and gains, and any relief or allowance, taken into account, how much tax is payable, and by when.

The tax chargeable by a simple assessment, or the balance of any tax so chargeable that has not already been deducted under PAYE or paid on account, must be paid to HMRC by the following 31 January, or – where the simple assessment is issued after 31 October – three months after issue.

Where a person is in receipt of a notice of simple assessment, they are not obliged to notify chargeability under TMA 1970, section 7. But if a person has already sent in a return for the year in question, or has received a notice under TMA 1970, section 8 to deliver one, they cannot also benefit from a simple assessment – unless they have also received a notice under TMA 1970, section 8B withdrawing the section 8 notice, and nothing prevents HMRC from giving notice of simple assessment at the same time as a section 8B notice.

There are provisions enabling the taxpayer to ‘query’ a simple assessment within 60 days after the notice is issued (TMA 1970, section 31AA), and a formal right of appeal if dissatisfied with HMRC’s response to the query (TMA 1970, section 31(1)(d), (3A) and (4A)).

Deferred pension – the taxation of social security pension lump sums

If a person decides not to claim their SRP when they first become entitled (for example, they may wish to continue working for a year or two), SSCBA 1992, section 55 and Sch 5 provide for the pension to be increased each year that it is deferred.

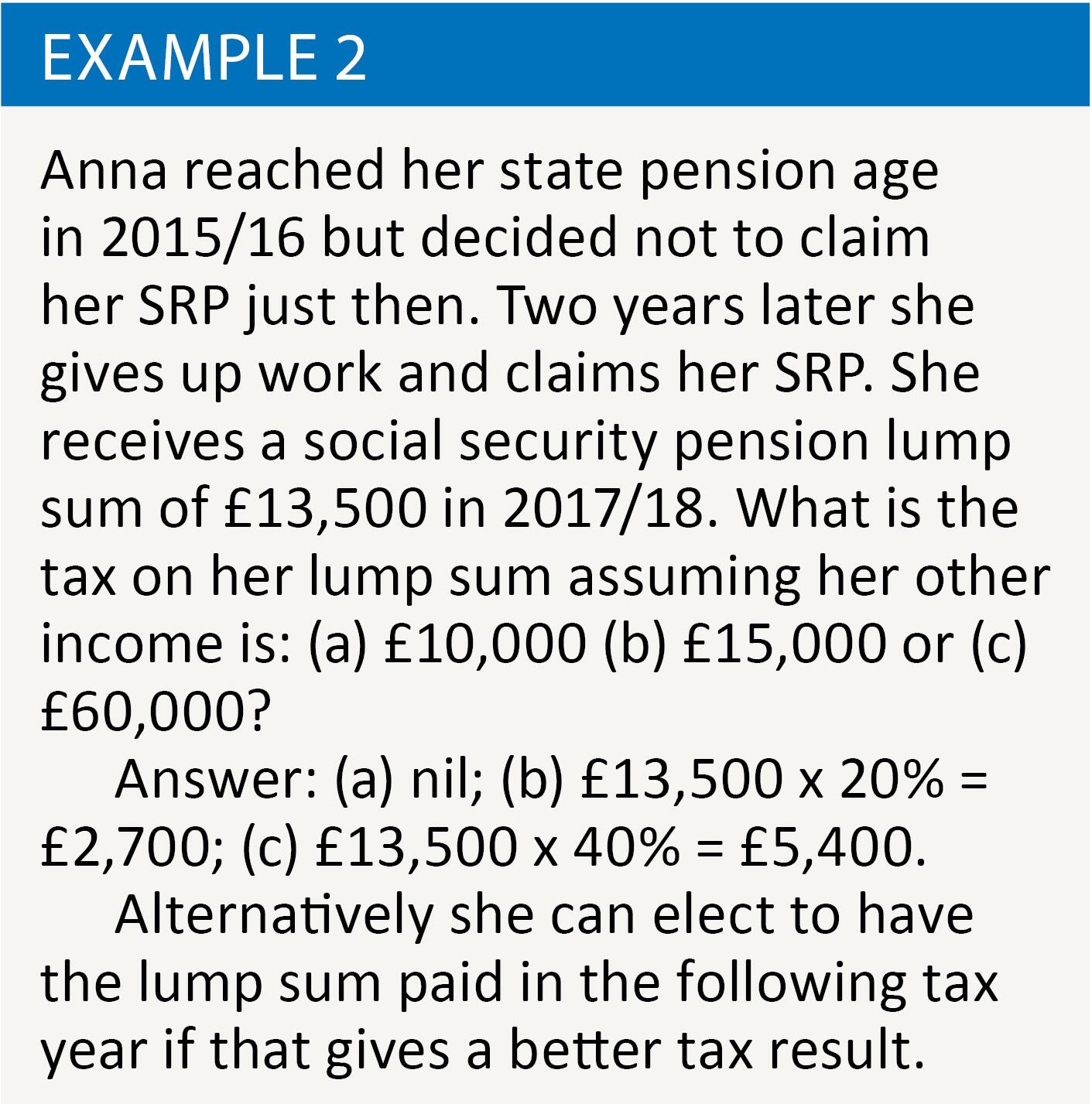

LITRG is often asked how a social security lump sum, or the payment of an accumulated state pension after a period of deferment, is taxed. F(2)A 2005, sections 7-9 provide quite simply that the lump sum is treated as income but is not counted when determining the tax rate to be applied to the lump sum. So if a person’s income apart from the pension lump sum (‘other income’) is totally covered by their personal allowances, the pension lump sum is taxed at a nil rate. If their other income less allowances is below the basic rate limit, the pension lump sum is taxed at the basic rate, at the higher rate if other income is between the basic rate limit and the higher rate limit, and at the additional rate if other income exceeds the higher rate limit.

The pension lump sum is taxed in the year of assessment in which it becomes payable after the period of deferment, but if the taxpayer dies without claiming the SRP, in the tax year of death. See example 2.

Tax credits treatment of state retirement pension

The SRP is counted as tax credits income in the tax year when it accrues (Tax Credits (Definition and Calculation of Income Regulations 2002/2006, reg. 5(1)(a)) but the first £300 may be disregarded (SI 2002/2006, reg 3(1), Step 1).

As for the social security pension lump sum, SI 2002/2006, reg 16(1) treats a claimant as having any income that ‘would become available to [him/her] upon the making of an application for that income’, but reg 16(3) excludes any state retirement pension payment of which has been deferred. Thus, state pension income is not treated as income for tax credits purposes during the period of deferral (although it may be for other benefits including UC) but only when paid (SI 2002/2006, reg 5(1)(n)).