Tax in difficult times

Share this article

Robin Williamson considers tax and benefits on bereavement and disability and for carers

Key Points

What is the issue?

No welfare benefit has been immune from economies during the past seven years, and the cuts to bereavement benefits which came into effect in April this year can be particularly stringent in their effect on younger families

What does it mean to me?

Nobody enjoys immunity from the ups and downs of life and the personal tax adviser who has a working knowledge of state benefits payable when times take a turn for the worse, and their tax treatment, can offer his or her client a better service.

What can I take away?

The adviser who has this knowledge and can turn it into practical planning may be able to steer his or her client away from common pitfalls and towards maximising their income at a time when the client most needs to do so.

In my article, ‘Curiouser and Curiouser’ in the August 2017 issue of Tax Adviser, I began to investigate some of the curious interactions between the tax and social security systems, first outlining some general principles then concentrating particularly on the state retirement pension and other benefits payable in later life.

People are living longer than ever before, but even today some do not make it to retirement age. It is particularly sad when a parent dies, leaving the surviving parent alone with their children. If the deceased person made sufficient NI contributions, the survivor may be entitled to claim bereavement benefits – but no welfare benefit has been immune from economies during the past seven years, and the cuts to bereavement benefits which came into effect in April this year can be particularly stringent in their effect on younger families.

This article contains a summary of the bereavement benefits both before and since April 2017, including the tax, tax credits and universal credit (UC) interactions, then does the same for carer’s allowance and certain disability benefits.

Bereavement benefits

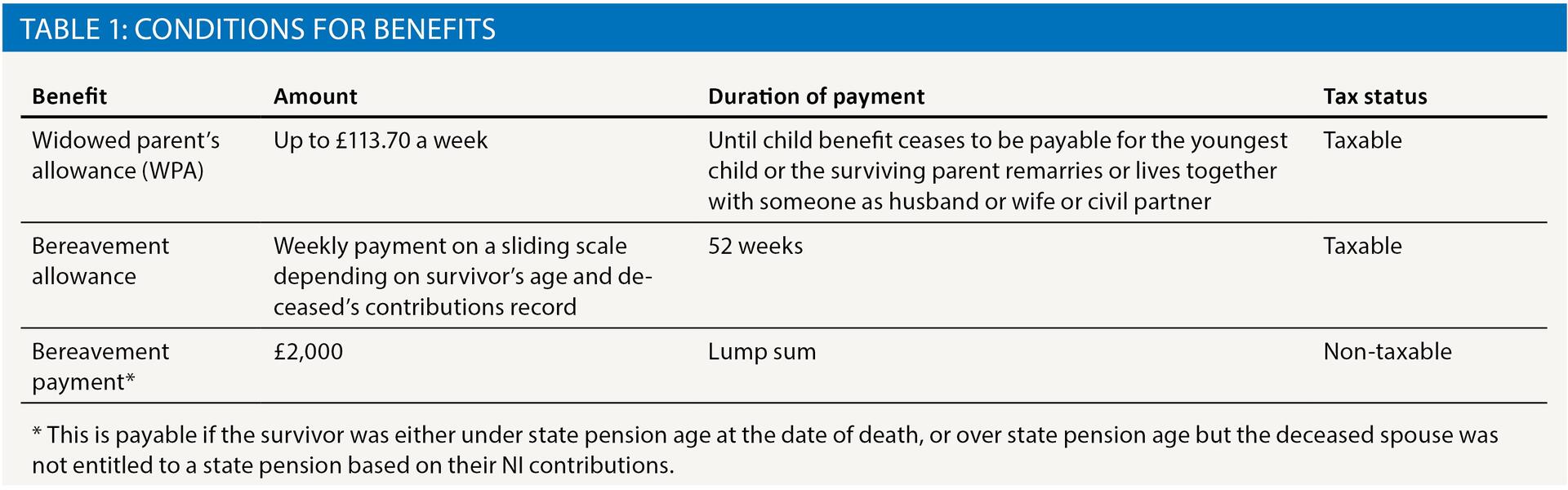

Certain benefits are payable to the survivor of a married couple or civil partners where the deceased spouse or partner has paid sufficient contributions or has died as a result of a work-related illness or accident. These bereavement benefits are not normally payable to individuals over state pension age, but such individuals may sometimes claim extra pension based on their deceased spouse’s NI contributions. The type of bereavement benefit that may be payable depends on whether the death occurred before, or on or after, 6 April 2017.

Before 6 April 2017

If the deceased spouse or civil partner died before 6 April 2017, the following are payable if the relevant conditions are met. See table 1.

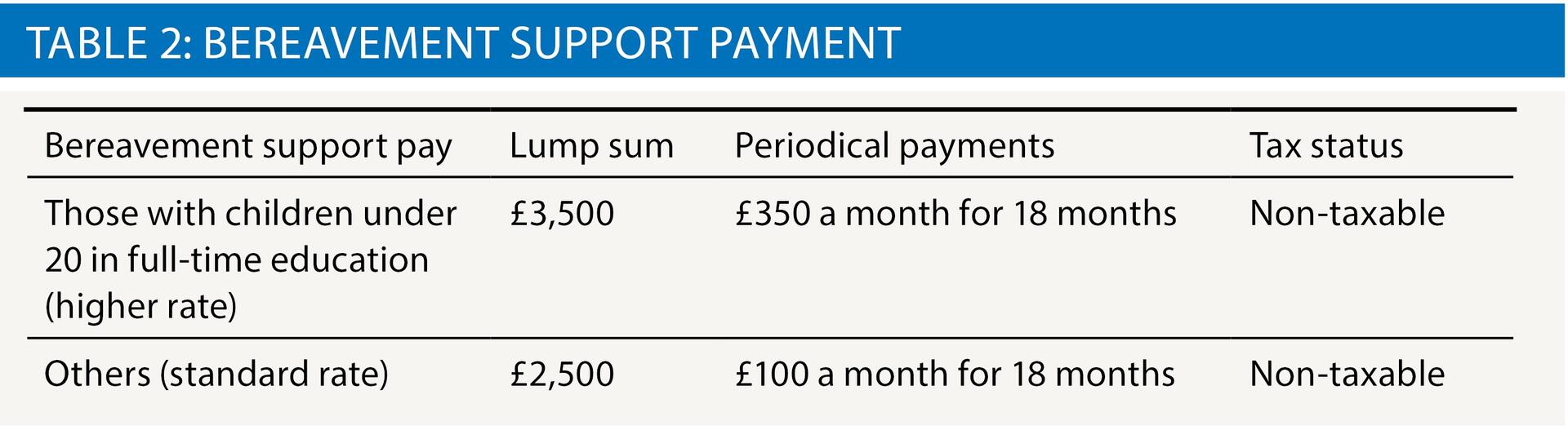

Deaths on or after 6 April 2017

The surviving spouse or civil partner of an individual who dies on or after 6 April 2017 may claim bereavement support payment (BSP). See table 2.

It will be noted that the lump sum payable under the BSP is more generous than under the bereavement payment, but that the periodical payment is significantly less so than under the WPA in terms of both amount and duration. It follows that younger families are likely to fare much worse under the new scheme, as they would have expected to receive the WPA until the surviving parent ceased to be eligible for child benefit for the youngest child. As part of the Childhood Bereavement Network coalition, LITRG advocated that the new benefit should be non-taxable – and so it is, both increasing the financial benefit and simplifying the fiscal treatment. Like the predecessor benefits BSP is dependent upon the NI contributions of the deceased spouse or civil partner; they must have paid contributions for at least 25 weeks, or died as a result of a work-related illness or an accident at work.

Tax credits and universal credit treatment

Bereavement allowance and WPA both count as income for tax credits purposes because they are taxable (though WPA counts as pension income and therefore attracts the £300 disregard available to Step One income in SI 2002/2006 reg 3(1)). They therefore reduce the tax credit award by up to 41p in the £ where the recipient has income higher than the appropriate income threshold (£6,420 if in receipt of both working and child tax credit, £16,105 if in receipt of child tax credit only).

Bereavement allowance and WPA also count as unearned income for universal credit (UC), and are therefore deducted from the UC award pound for pound. This leads to the bizarre result that a UC claimant can be worse off if they also claim bereavement allowance or WPA: they receive the bereavement benefit, 100% of the amount of that benefit is deducted from their UC award, and they pay tax at 20% on the benefit, with the result that they are worse off by 20% of the amount of the bereavement benefit than if they had not claimed it! If this interaction causes a drop in the claimant’s net employment income, their UC will increase slightly as a result, but not enough to compensate them in full. Fortunately most WPA or bereavement allowance recipients are in tax credits and will be unaffected by this anomaly so long as they remain there.

War widow’s or widower’s pension

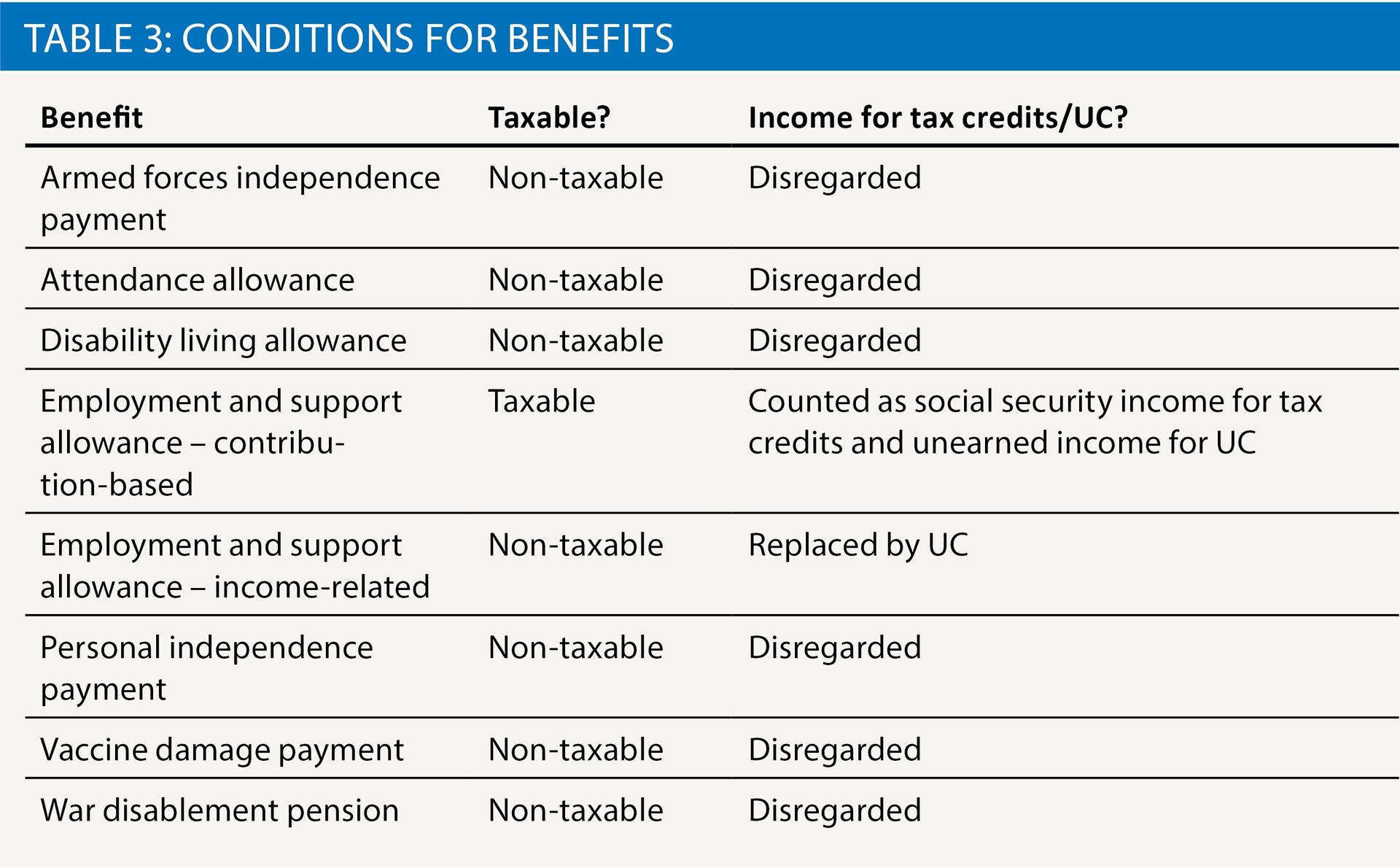

This is payable to claimants whose husband, wife or civil partner died as a result of their service in the armed forces. It is non-taxable and disregarded for both tax credits and UC.

Carer’s allowance

Carer’s allowance is payable at a rate of £62.70 a week to people who provide care for at least 35 hours a week. The person cared for must receive either the daily living component of personal independence payment (PIP), or disability living allowance care component at the middle or highest rate, or attendance allowance or armed forces independence payment.

Carer’s allowance is taxable and is counted in full as social security income for the purposes of tax credits. It is treated as unearned income for universal credit, so it is deducted from the UC award pound for pound. However, UC claimants may be entitled to an additional element in their award if they have regular and substantial caring responsibilities, which means they must fulfil the same conditions as would give them an entitlement to carer’s allowance, including providing care for at least 35 hours a week – but there is no requirement actually to claim carer’s allowance.

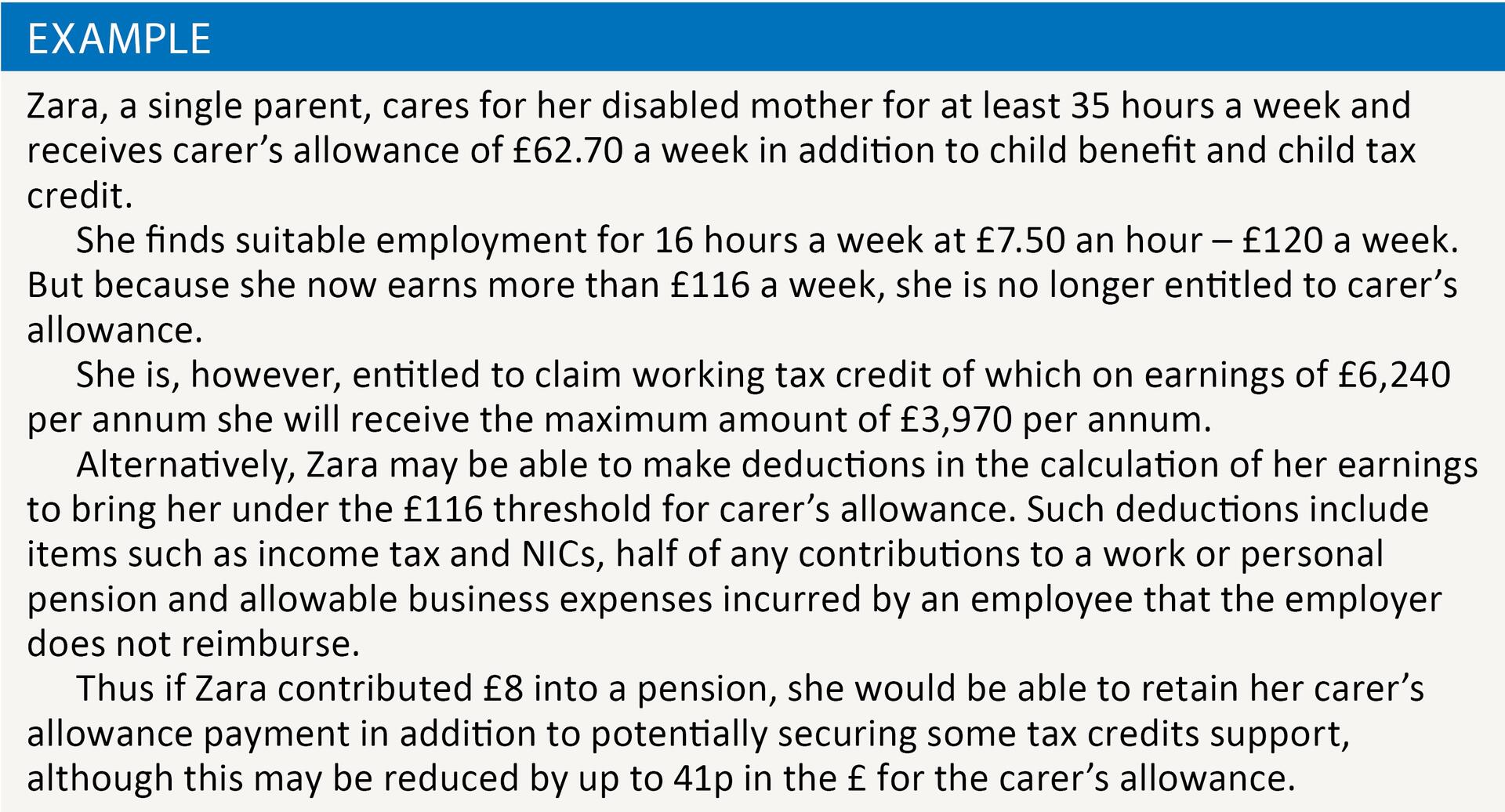

Carer’s allowance is not payable to anyone who has net earnings above a threshold of £116 a week. So if you are 25 or over, and are paid the national living wage of £7.50 an hour, you will cease to be eligible for carer’s allowance if you work 16 or more hours a week – but therein lies a catch, because 16 hours a week is normally the minimum anyone must be working in order to qualify for working tax credit. Depending on the claimant’s circumstances it may be beneficial to allow the carer’s allowance to lapse in order to secure the opportunity for higher earnings and possibly tax credits in addition (see example).

The earnings restriction does not apply where the claimant is receiving the carer element of universal credit.

Recipients of carer’s allowance may also receive national insurance credits, council tax reduction, income support, income-based employment and support allowance or pension credit in appropriate cases.

Disability benefits

ESA and PIP

The main working-age disability benefits now are employment and support allowance and personal independence payment:

- employment and support allowance (ESA) which exists in two forms – contribution-based and income-related – and is payable at different rates depending on whether the claimant is in the ‘work-related activity group’ (in which claimants are obliged to attend work-related interviews) or ‘support group’ (which is for claimants whose illness or disability severely limits what work they can do), and

- personal independence payment (PIP) which consists of the daily living component (standard and enhanced rates) and mobility component (standard and enhanced rates). PIP helps with the extra costs incurred as a result of long-term ill health or disability and broadly replaces disability living allowance for working age claimants.

Tax

Contribution-based ESA is taxable – income-related ESA and PIP are non-taxable. Contribution-based ESA is based, as the name suggests, on NI contributions and is paid for a limited period of one year if the claimant is in the work-related activity group. Historically ESA replaced incapacity benefit which was itself taxable unless the recipient had previously been in receipt of invalidity benefit since before April 1995.

Tax credits

The tax credits treatment follows the income tax treatment, so contribution-based ESA is counted in full as social security income in assessing tax credits entitlement, while income-related ESA and PIP are disregarded. In addition, anyone receiving income-related ESA is entitled to receive a maximum award of tax credits (ie without any tapered withdrawal of benefit).

Receipt of PIP might also be a factor qualifying a claimant for the disability elements of working tax credit and the disabled child element of child tax credit.

Universal credit

Contribution-based ESA is counted as income for universal credit purposes, but it is treated as unearned income so reduces the UC award pound for pound. But the UC award may be increased by an additional element reflecting limited capability for work and work-related activity (the LCWWRA element). UC replaces income-related ESA.

PIP is not treated as income for UC.

Disability living allowance

Disability living allowance (DLA) behaves in a similar way to PIP in relation to tax credits and universal credit in that it is not taxable and is not counted as income for tax credits or UC, but can be a factor giving rise to entitlement to various disability elements in tax credits.

As DLA has been gradually phased out in favour of PIP for working-age people since 2013, there will be few now between the ages of 16 and 64 who are still receiving it, but it is still payable to disabled children under the age of 16 and to people of 65 and over who were receiving it when of working age. See details of the types of benefits, whether that benefit is taxable, and how income for tax credits or UC affects that benefit as set out in table 3.