Debt due to the crown

Share this article

Neil Warren considers practical examples of how HMRC will deal with VAT incorrectly charged on sales invoices that is not declared on returns

Key Points

What is the issue?

VAT charged on a sale that is not taxable is not classed as output tax but would still be a debt to the crown. So HMRC will seek to recover this tax from the supplier. Protection is given to customers in many situations when they pay tax in good faith and claim input tax.

What does it mean to me?

In the case of a business buying property and being charged VAT on the sale, it is important to confirm that the seller has made an option to tax election with HMRC on the building, i.e., to confirm the sale is taxable rather than exempt.

What can I take away?

Advisers should be aware of ESC3.9 in VAT Notice 48 which gives protection to taxpayers who have paid wrongly charged VAT to suppliers and claimed input tax in good faith on their returns.

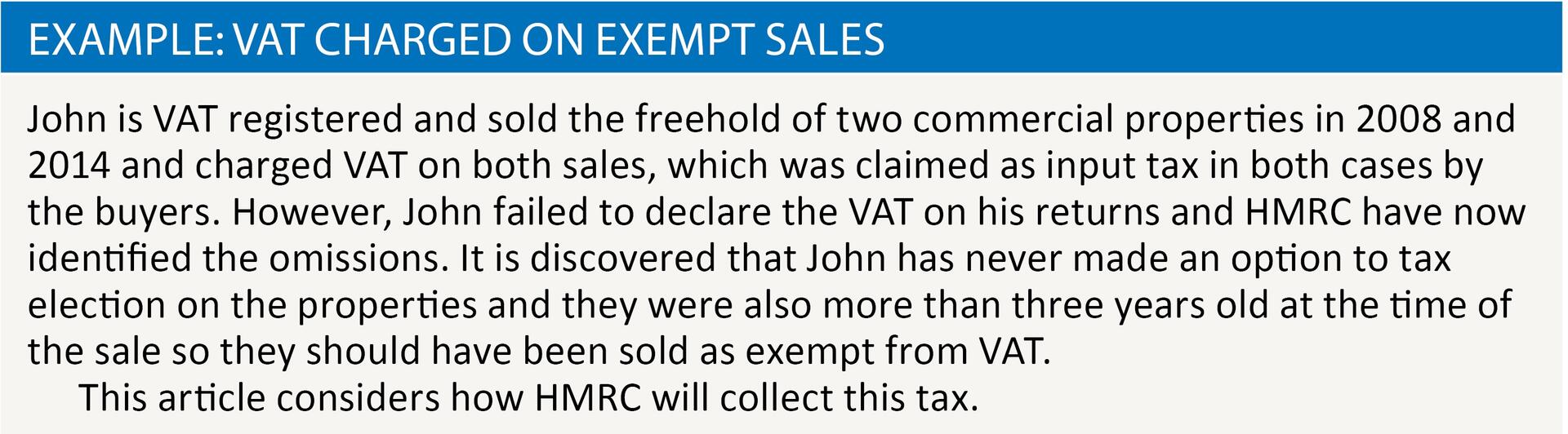

The VAT system only works properly if input tax claimed by one business has been declared as output tax by another. If this doesn’t happen, then HMRC will be out of pocket and will seek to take correction action. But what happens if a business incorrectly charges VAT on an invoice and never declares it on a return, such as adding 20% VAT to a property sale that should be exempt from VAT because the seller has never made an option to tax election? In this article, I will consider two practical situations that I have dealt with where this happened, which not only had implications for the seller but threatened the input tax claims made in good faith by the buyers as well.

Charging VAT on an exempt sale

The first situation is explained in the example. I have used the example of two property sales but it could have been any exempt supplies where 20% VAT (or 5%) was incorrectly charged by the seller. Now here is the twist to the tale: many readers will think that the seller has got a good result with the first property sale because it happened more than four years ago and is therefore out of time as far as an HMRC assessment is concerned. Any errors on VAT returns more than four years ago can only be adjusted if fraud is involved, in which case a 20-year time period will apply. But this is not correct:

- The business did not declare output tax on the two property sales on its VAT return. This is correct because the supplies in question were exempt from VAT so the VAT charged on the two invoices was not output tax. So there have been no errors on the VAT returns for the two sales in question.

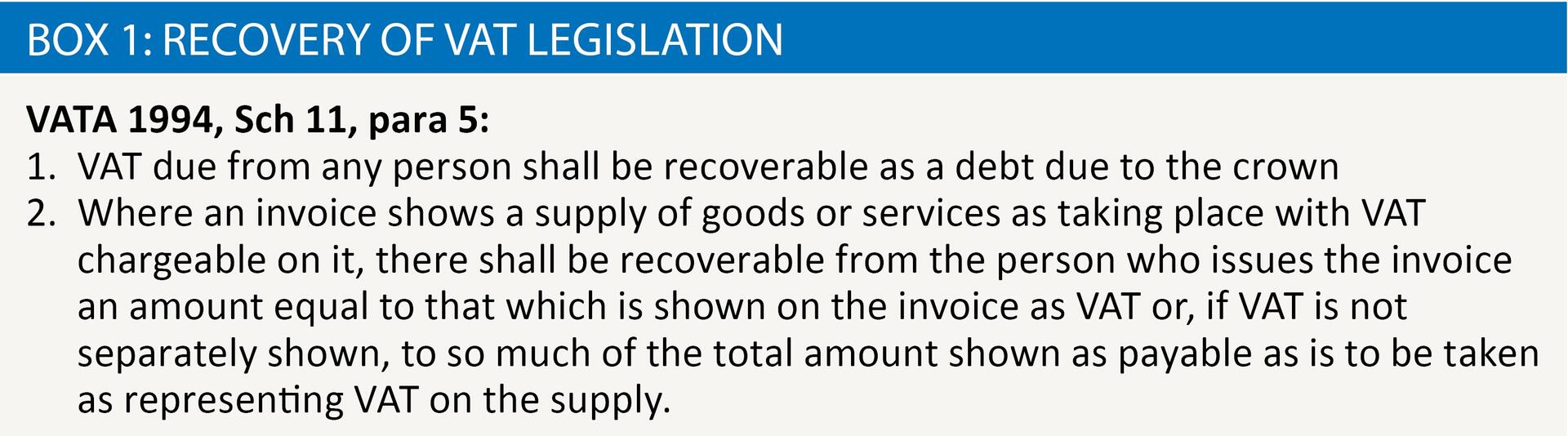

- However, the business has charged VAT on two sales invoices, and this tax becomes classed as ‘a debt due to the crown’. The relevant legislation is no longer s73, VATA1994 (which gives an officer the power to use his ‘best judgment’ and raise an assessment to correct errors on VAT returns submitted by a business) but para (5), Sch 11, VATA1994. See box 1.

An important fact about Sch 11 assessments is that they are not time barred. So the four-year time cap is a red herring, and HMRC now have the power to assess ‘a debt due to the crown’ on both of the property sales considered in my example.

To give further analysis, HMRC’s key guidance is the VAT manual titled “Assessments and Error Corrections”–and then section VAEC9500 headed ‘Demand for VAT: contents’ and sub section VAEC9600. The guidance confirms the approach that officers should adopt where VAT has been incorrectly charged on a supply and excluded from a VAT return i.e., the relevance of Sch 11 explained above.

VAT charged by an unregistered business

My second true story relates to a business that had been registered for VAT for many years but then failed to tell HMRC about its change of address. So to cut a long story short, HMRC classified the business as a ‘missing trader’ because correspondence was being returned from the old address and eventually cancelled its VAT registration. The business owner (a sole trader computer consultant) continued to charge VAT to his customers, quoting his old VAT number on his sales invoices but not paying the VAT to HMRC because he was obviously deregistered and not completing returns. In his defence, he was not spending the VAT money on an expensive lifestyle of champagne and caviar but keeping it in a separate business bank account, with the intention of ‘sorting it out when I have more time’. Unfortunately, HMRC discovered the problem before he disclosed it!

So what is the situation here? The VAT charged on these sales is again classed as ‘a debt due to the crown’ (para 5(3), Sch 11, VATA1994) and as explained earlier, there is no four-year time limit as far as collecting past arrears is concerned.

Customers claiming input tax

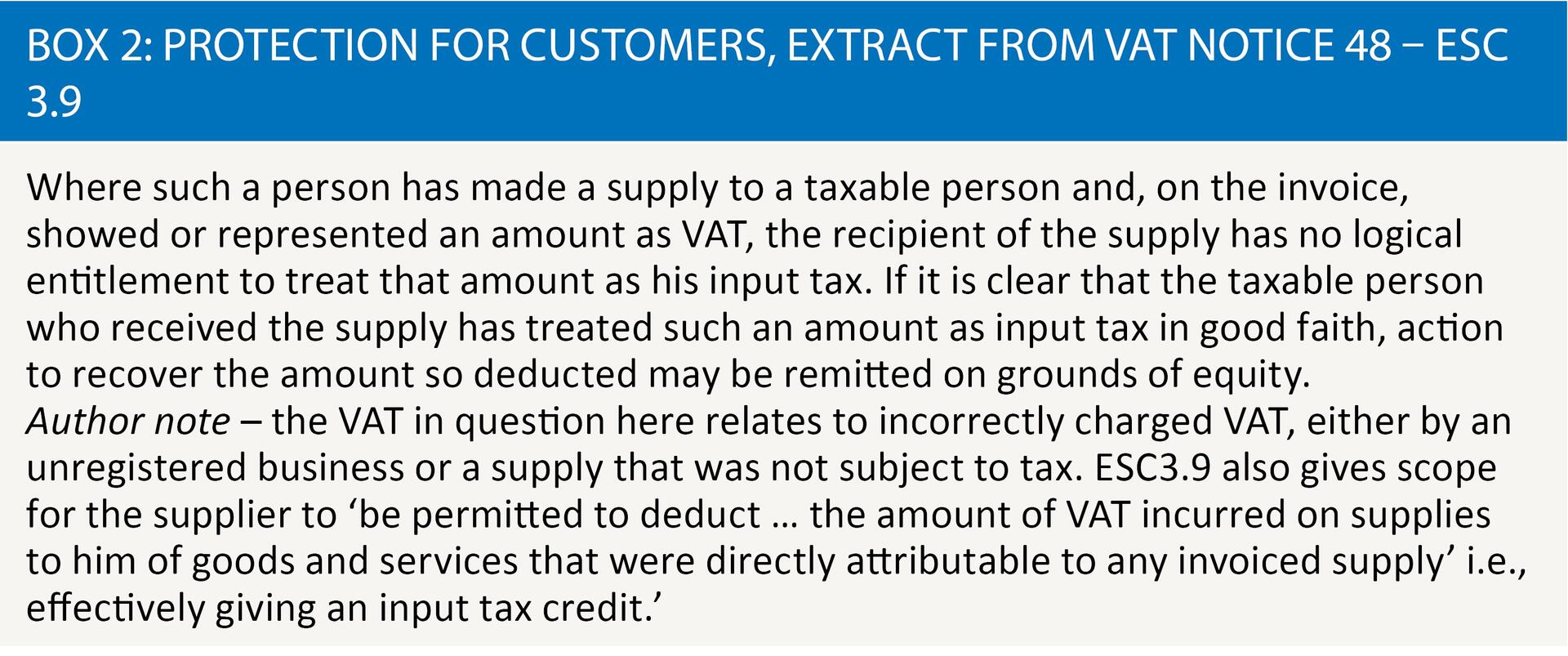

In both scenarios, customers have claimed input tax on supplies that were not subject to VAT. The property sales were exempt and the consultant was not VAT registered at the time of issuing invoices. So a strict application of s24, VATA1994 means that HMRC have the power to disallow input tax (subject to the usual four year assessment period) because it is not correctly charged VAT. The customer must then seek a VAT credit from the seller, which could be a massive challenge if the seller has emigrated to Spain or liquidated his business.

However, the good news is that an Extra Statutory Concession (ESC) gives some protection to customers who have claimed input tax in good faith. The various ESCs in the tax world are included in Notice 48 and I have reproduced the relevant extract from ESC3.9 – see box 2 Many ESCs are now obsolete but ESC3.9 is still relevant.

Conclusion

I always feel sympathy for innocent business owners who get tangled up in a VAT mess created by other parties. I am thinking here of business customers who pay VAT in good faith to suppliers and are then faced with a potential input tax disallowance by HMRC because of supplier mistakes or dodgy actions. Hopefully the actions of HMRC will always target the business that has created the problem i.e., as reflected by ESC 3.9.

From a practical aspect, there are a number of important learning points:

- A business moving premises should always notify HMRC of its change of address. This will avoid the ‘missing trader’ outcome that caused so many problems for the computer consultant.

- Solicitors and advisers acting for clients who are buying property where the seller wants to charge VAT on the sale should always be certain that a valid option to tax election has been made by the seller i.e., to confirm that the sale is taxable rather than exempt.

- Many customers operate self-billing, particularly in the construction industry, where they effectively issue tax invoices on behalf of suppliers. It is important to regularly confirm that suppliers have not deregistered and become an ‘unauthorised person’ receiving VAT money that is never declared on a return. This problem was relevant in the VAT tribunal case of road transport firm Taygroup Ltd (TC336). The decision went against the taxpayer as HMRC disallowed input tax claims of £214,447 in relation to payments made to subcontractors who had deregistered.

- To check the validity of a supplier’s VAT number – see www.tinyurl.com/VAT-checker. I have just used this link myself and the good news is that both of my companies are still VAT registered – I am not a missing trader!