The dividend illusion

Share this article

Jacqui Kimber examines the consequences of the new dividend allowance introduced in April

Key Points

What is the issue?

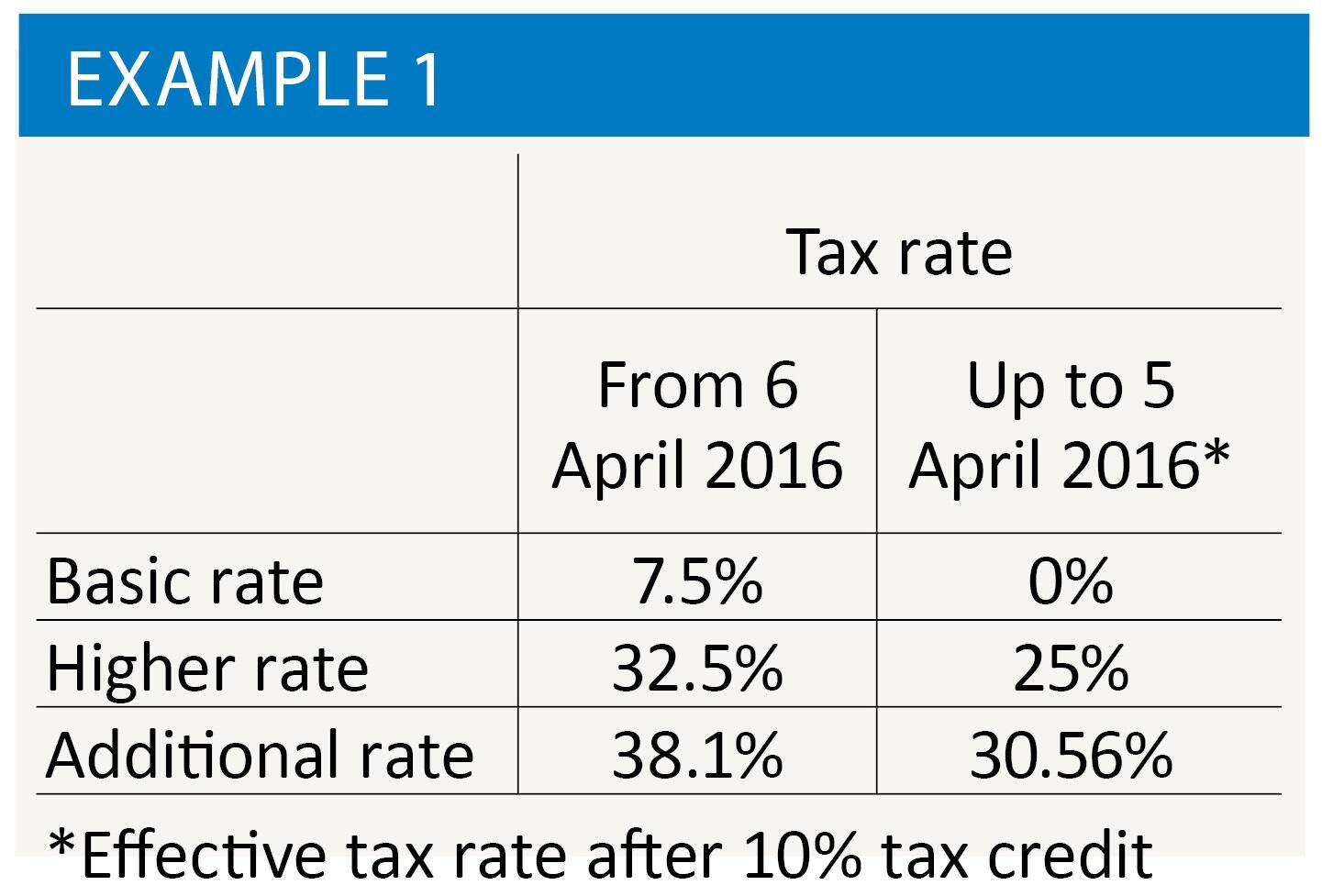

The landscape of taxation of dividends in the hands of individuals changed fundamentally on 6 April 2016.

What does it mean to me?

Although seemingly straightforward, the changes have caused some practical issues to emerge.

What can I take away?

Despite its name, the dividend allowance is not an allowance at all, and is rather a 0% rate of tax that applies to the first £5,000 of dividend income received by an individual taxpayer each year.

The landscape of taxation of dividends in the hands of individuals changed fundamentally on 6 April 2016. The headline changes include the abolition of the notional 10% tax credit attached to most dividends and the introduction of a £5,000 ‘dividend allowance’. Dividends continue to be treated as the top slice of income, and there is no distinction between those from UK companies and those received from overseas (unless they are relevant foreign income for remittance basis users).

Although seemingly straightforward, the changes have caused some practical issues to emerge. Billed as a measure to ‘simplify’ the taxation of dividends, the abolition of the 10% tax credit has some unexpected consequences. For example, a taxpayer with non-dividend income of £10,000 and dividend income of £20,000 would have suffered no income tax in 2015/16 because non-dividend income would have been covered by the personal allowance and the notional 10% tax credit would have fully met his liability on dividend income within the basic rate band. In 2016/17, assuming the same income figures, again the personal allowance would cover the non-dividend income and £1,000 of the dividends. The dividend allowance is applied against the first £5,000 of the remaining £19,000 of dividend income, leaving £14,000 of dividends to be taxed at 7.5%, giving a liability of £1,050. The taxpayer is therefore left £1,050 out of pocket. In addition, he will have to notify HMRC of his obligation to complete a self-assessment tax return for 2016/17 by 5 October 2017, whereas previously it is likely that no return would have been required. Payments on account may also be required.

Further problems arise if the taxpayer is philanthropically minded and makes generous gift aid payments each year of, say, £8,000.

Gift aid relief requires the donor to have paid income tax equal to the basic rate treated as paid on a donation – in other words, £2,000 in the case of a donation of £8,000 net. In 2015/16, despite having no income tax liability, the taxpayer’s obligation to account for basic rate tax deducted from the gift aid payment is discharged through the tax notional credits attaching to the dividends. The removal of these credits from 6 April will require the taxpayer to make up the shortfall of £950 in tax paid (£2,000 less £1,050). The taxpayer therefore has a choice: to maintain the level of donations made and accept the additional tax liability, or reduce the gift aid donation to correspond with the tax payable on dividend income (£5,250 gross). Charities will also need to revisit their guidance to donors to draw attention to the potential problem.

Dividend allowance

Despite its name, the dividend allowance is not an allowance at all, and is rather a 0% rate of tax that applies to the first £5,000 of dividend income received by an individual taxpayer each year. This has several consequences. First, if one is of a cynical turn, setting the allowance as a nil rate of tax could pave the way for the rate to be increased easily in future finance acts. Second, the dividend allowance does not reduce an individual’s taxable income for the purposes of various thresholds such as the high income child benefit charge (£50,000), withdrawal of the personal allowance (£100,000), and tapering of pension tax relief (£110,000). Finally, the dividend allowance is deducted from the first £5,000 of dividend income, even if this may not be to the taxpayer’s advantage. This is illustrated by Example 6 in HMRC’s guidance on the new dividend allowance:

‘I have a non-dividend income of £40,000, and receive dividends of £9,000 outside of an ISA

Of the £40,000 non-dividend income, £11,000 is covered by the Personal Allowance, leaving £29,000 to be taxed at basic rate.

This leaves £3,000 of income that can be earned within the basic rate limit before the higher rate threshold is crossed. The Dividend Allowance covers this £3,000 first, leaving £2,000 of Allowance to use in the higher rate band. All of this £5,000 dividend income is therefore covered by the Allowance and is not subject to tax.

The remaining £4,000 of dividends are all taxed at higher rate (32.5%).’

In this example, tax payable on the dividend income is (£4,000 x 32.5%) £1,300. Clearly, if the allowance is applied to the top part of the dividend income, only £1,000 of dividends would be taxed at the higher rate of 32.5% and £3,000 would fall within the basic rate band and be taxed at 7.5%. This gives a total liability of (£3,000 x 7.5% plus £1,000 x 32.5%) £550, saving the taxpayer £750.

The good news is that all taxpayers, even those on the additional rate of 45%, receive a £5,000 dividend allowance each year. Although the allowance is unlikely to have much of an impact on those with significant income levels, it is worth considering putting modest amounts of dividend income into the hands of spouses and children even if they are higher or additional rate taxpayers.

Interaction with personal savings allowance

The personal savings allowance permits savings income of up to £1,000 a year to be received tax-free by a basic rate taxpayer. For higher rate taxpayers, the amount that can be received tax-free is £500. Individuals paying tax at the additional rate do not receive a personal savings allowance. Savings income comprises interest on bank and building society accounts, but also interest on government bonds and interest distributions from authorised unit trusts. Foreign interest is also covered unless it is relevant foreign income for remittance basis purposes.

As has already been seen in relation to the dividend allowance, the personal savings allowance is not an exemption from tax, and savings income still counts towards an individual’s total taxable income. So it is necessary to look at total income, including savings and dividends within the dividend allowance, to determine how much savings income, if any, attracts the personal savings allowance.

For basic or higher rate taxpayers whose entire savings income is below the personal savings allowance, the position is relatively straightforward and no tax is payable on it. Around the margins of the tax bands, however, the position becomes more complex and it is possible for a taxpayer to be worse off than if a slightly lower amount of interest had been received. Say a taxpayer receives a salary of £40,000, dividends of £2,500 and £600 of savings income, giving a total income of £43,100. Since this is above the higher rate threshold (£43,000 for 2016/17), the personal savings allowance is reduced to £500, albeit no higher rate tax is actually payable. In extreme cases, an additional £1 of savings income can cost £500 of personal savings allowance.

HMRC states in its guidance that it expects most adjustments to be made through individuals’ tax codes based on information received from banks. Taxpayers would be advised to check their tax codes carefully to ensure any adjustments are reflected correctly.

Income splitting

The dividend allowance and personal savings allowance are not transferable between married couples or civil partners and, as already mentioned, a basic planning strategy would be to ensure that each individual makes full use of their allowances each year. Similarly, interest-bearing savings accounts or bonds can be split to maximise the £1,000 savings allowance. Care needs to be taken if shares in the family business are to be transferred between spouses to avoid falling foul of the settlements legislation in ITTOIA 2005 s 624. However, it should be possible in most cases to arrange shareholdings between married couples or civil partners so that each has a £5,000 dividend allowance.

Family business owners may also wish to consider making gifts of shares to children over 18 to use the personal allowance and dividend allowance, particularly as a means of funding further education. The employment related securities rules should not apply in these circumstances because of the specific carve-out for transfer or issues of shares when the right or opportunity is made available by an individual in the normal course of his or her domestic, family or personal relationships (ITEPA 2003 s 421B(3)). However, HMRC’s manuals point to the possibility of the employment related securities rules applying if, as a question of fact, it is the employment rather than the family relationship that is the rationale for the gift.