All change

Share this article

The payment and administration of capital gains tax is changing from April 2020, writes Jacquelyn Kimber. Are you ready?

Key Points

What’s the issue?

The next round of changes to CGT are planned from April 2020. From 6 April 2020, where CGT is due on residential property disposals, a return will need to be filed, and the ‘notional CGT’ due must be paid within 30 days of the date of completion.

What can I take away?

The relevant legislation in TCGA 1992 Sch 2 deals with both UK resident individuals and non-resident persons, but there are differences between these two categories of taxpayer and it is helpful to consider them separately.

What does it mean to me?

To date, awareness amongst taxpayers appears to be low and undoubtedly some will be caught unawares.

The tax landscape for UK property has changed immeasurably over the last six years. First, in 2013 came the introduction of the annual tax on enveloped earnings (ATED) regime and ATED-related capital gains tax (CGT). This was followed by the extension of CGT to disposals of UK residential property by non-UK residents from 2015. Most recently was the extension of the non-UK resident CGT regime to all direct and indirect disposals of UK property, whether residential or commercial from April 2019, and the move back to non-resident companies being charged to corporation tax (not CGT) on property gains.

In this and a follow up article to be published in the February issue of Tax Adviser, we examine the next round of changes which are planned from April 2020. This article focuses on the technical nature of the changes (excluding rebasing for non-residents), and the next will look at some of the practical implications of the new regime.

A question of timing

The current self assessment system means that, depending on timing, CGT is due anywhere from 22 months to 10 months after the disposal. HMRC first announced in April 2015 that they intended to expedite payment of CGT in the case of disposals of residential property, and having delayed implementation once already, they are now pressing ahead with change.

From 6 April 2020, where CGT is due on a residential property disposal:

- a return will need to be filed (for the sake of brevity, I refer to this as a ‘UK land return’ although this is not the wording adopted in the legislation; and

- the ‘notional CGT’ due must be paid within 30 days of the date of completion (FA 2019 s 14 and Sch 2).

This is a major change to the administration of CGT for UK residents and some non-residents. Although the policy intention may be simple in outline, as ever the detailed position is much more complex.

The relevant legislation is in TCGA 1992 Sch 2. ‘Residential property’ is as defined in TCGA 1992 Sch 1B and therefore has the same definition as applied under the non-resident CGT regime. Where a property comprises residential and commercial parts, the gain arising must be apportioned on a just and reasonable basis. Only the residential element will be subject to the new reporting and payment requirements. There are other exclusions; for example, where the disposal is under a no gain/no loss transaction, or where the person making the disposal is a charity or pension fund (Sch 2 para 1(2)).

Schedule 2 deals with both UK resident individuals and non-resident persons, but there are differences between the two categories of taxpayer and it is helpful to consider them separately.

UK residents

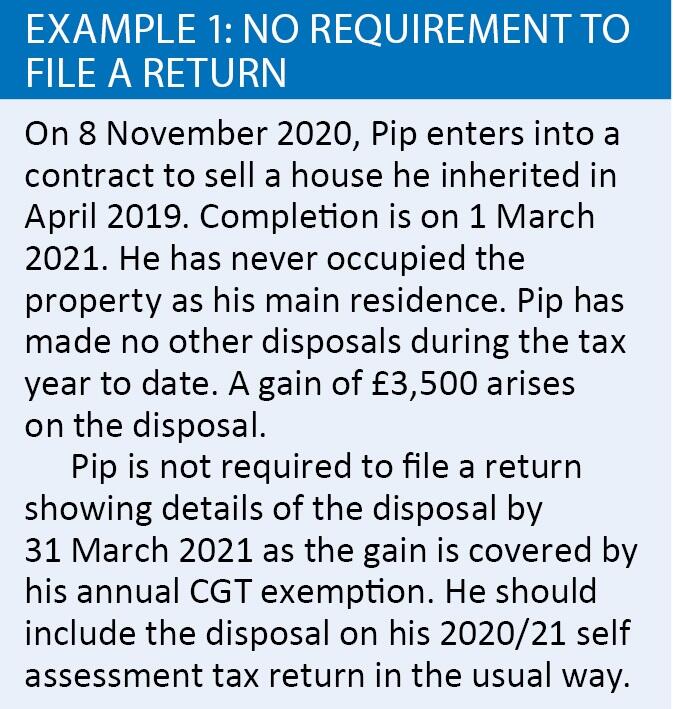

For UK resident individuals and trustees (the changes don’t apply to UK companies), a UK land return will need to be filed with HMRC where a disposal of residential property gives rise to a chargeable gain or an allowable loss (Sch 2 para 4). Where a gain is fully covered by a relief (such as private residence relief), there will be no requirement to file a UK land return. A return will also not be required where the gain is covered by the annual exemption, or a brought forward capital loss. Where there is no requirement to file a return, there is similarly no requirement to make a payment on account of CGT. (See Example 1.)

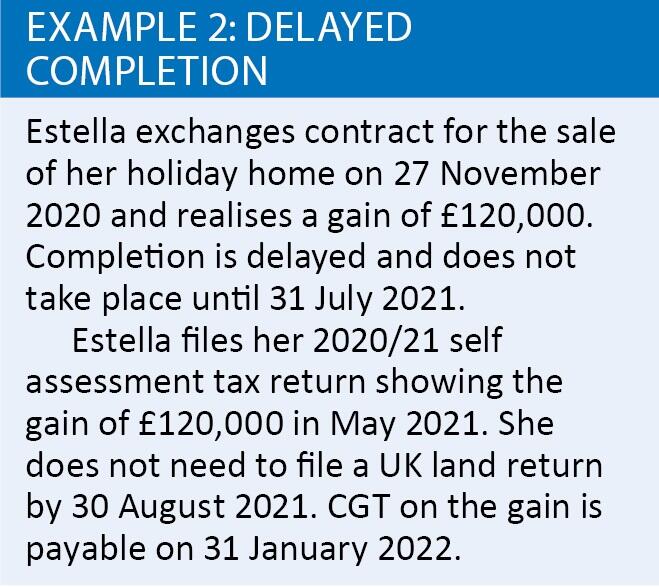

In any other case, the UK resident individual must complete a return, and pay any CGT due within 30 days of the completion date of the disposal. In the uncommon event that two disposals complete on the same day, a single return is required (Sch 2 para 3). No UK land return is required where the filing date for that return is after the individual’s self assessment tax return has been or is due to be submitted (Sch 2 para 5). This will be relatively rare, but is feasible where there is a long delay between contracts being exchanged and the disposal being completed. (See Example 2.)

The UK land return requires the taxpayer to make ‘reasonable estimates’ of the tax payable on the disposal as if the tax year ended on the date of disposal (Sch 2 paras 7 and 14). The taxpayer will therefore need to estimate his/her income for the year so that the correct CGT rate of 18% or 28% may be applied, and also take into account any disposals of UK residential property which have already taken place. Gains on other assets are ignored in calculating the notional CGT due. Where an estimate changes, a further return may be filed correcting the estimate and, if appropriate, generating a repayment of tax (Sch 2 para 15).

Where a UK land return is submitted, there is no separate requirement for the taxpayer to notify HRMC of his chargeability to CGT (Sch 2 para 18).

Losses

A UK land return is not required where the disposal gives rise to a capital loss. However, if a return would have been required if a gain had arisen, the individual may make a return and make a repayment claim in respect of any notional CGT already paid in the tax year on an earlier disposal of UK land (Sch 2 para 9).

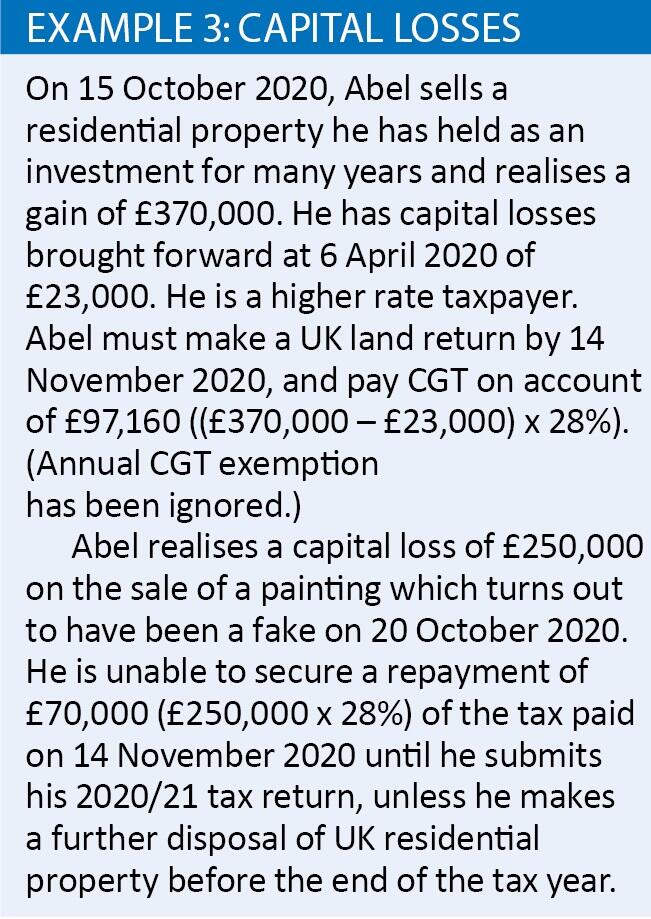

Realised capital losses, whether on UK residential property or other assets and whether brought forward or realised earlier in the tax year, may be taken into account when computing the notional CGT due. However, a loss arising later in the same tax year on another asset can only be taken into account in the individual’s self assessment tax return for the year, unless there is another UK residential property disposal which takes place after the loss has arisen. It is this aspect of the rules which creates the most distortions and potentially leads to the greatest unfairness in cash flow for the taxpayer. (See Example 3.)

The timing of disposals is therefore crucial. These rules seem unnecessarily harsh and HMRC’s response that any overpayment will carry repayment supplement somewhat inadequate, particularly where the disposal is by way of gift and there are no cash proceeds from which to pay the tax.

Claims and elections

In computing the notional CGT due, claims and elections are taken into account where it is reasonable to suppose that these will be made or given (Sch 2 para 14) but this does not remove the requirement to formally make the claim or election in a tax return, etc.

Reliefs (such as CGT deferral relief under EIS or SEIS) may be claimed in computing the notional CGT due where the conditions for the relief are met at the time payment is required. Otherwise, an amendment to the return will need to be made when the relevant conditions are met. Relief will, of course, also need to be claimed in the individual’s self assessment tax return, if one is required to be filed.

Non UK residents

Non-UK resident individuals, trustees and companies have been liable for CGT on disposals of UK residential property since April 2015. The non-resident is required to file a return and pay any CGT due within 30 days of completion, unless the disposal is by a taxpayer already within the scope of self assessment (for example, a non-resident landlord) or is subject to ATED charges.

From 6 April 2019, the scope of the non-resident CGT rules is expanded to apply to any disposal of UK land by a non-resident person, whether residential or commercial, and irrespective of whether the disposal is a direct disposal of UK land or an ‘indirect’ disposal of a ‘property rich entity’, i.e. one deriving 75% or more of its value from UK land (defined in TCGA 1992 Sch 1A). Certain exemptions, such as that for disposals by ‘non-close’ overseas companies, were also removed. But whilst the scope of the charge has changed, the exception from the requirement to file a return within 30 days and pay the CGT due in respect of residential property disposals remained for taxpayers within self assessment or liable to ATED charges. This exception will be removed from April 2020 and the position aligned with that applying to UK resident individuals, but with UK land returns and CGT payment being required for any direct disposal of UK land or indirect disposal of land-rich assets.

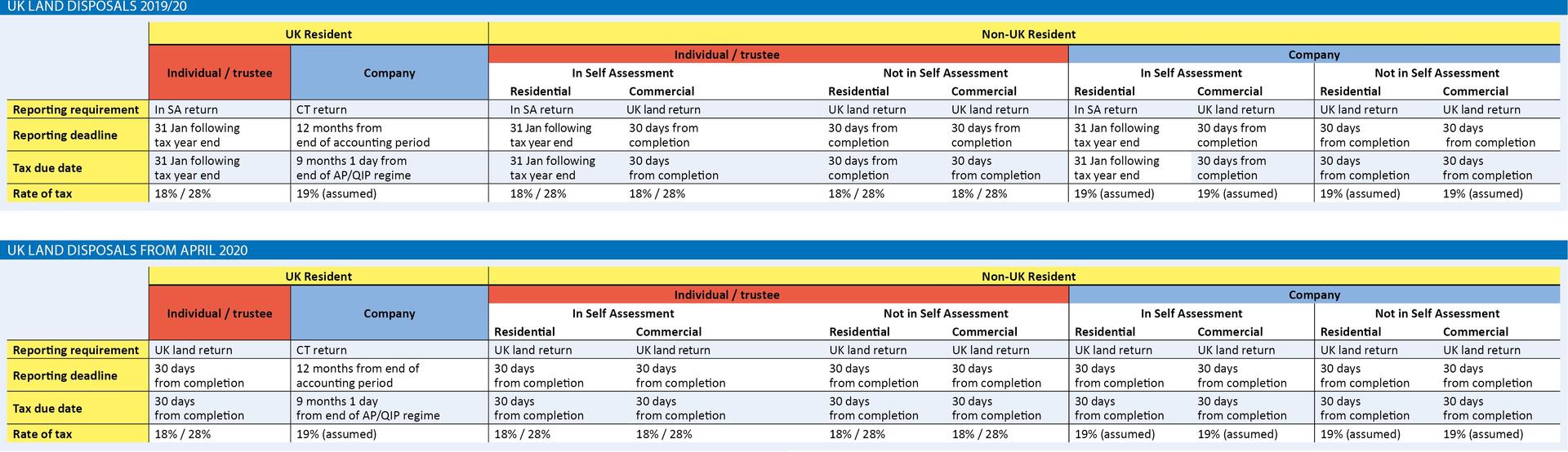

Unlike the position for UK residents, there is also no let out from the reporting requirements where no gain arises on the disposal or the gain is covered by reliefs or exemptions. This has been one of the more controversial aspects of the non-resident CGT regime and frequently gives rise to the imposition of late filing penalties, despite there being no tax liability. It is difficult to discern HMRC’s rationale for insisting upon returns where no tax is due but they appear immovable. A summary of the filing requirements for UK residents and non-residents for residential and commercial property is shown in the table below.

From April 2019, non-resident companies have been required to register for corporation tax within three months of a disposal of UK land. For a one-off disposal, this will mean filing a corporation tax return for an accounting period of a single day. Corporation tax is payable within normal corporation tax time limits, generally nine months and one day from the end of the accounting period, although the quarterly instalment payment (QIP) regime may also apply.

Compliance

Broadly, a UK land return will be subject to the same provisions regarding amendments, enquiries, amendments during an enquiry and determinations as apply to a self assessment tax return (Sch 2 paras 19 to 22). An amendment to a UK land return relating to a disposal included in a tax return may only be made up to the earlier of the filing date for the tax return and the date it is filed. If no tax return is due to be filed, a UK land return may be amended up to one year after the 31 January following the tax year.

Conclusion

HMRC said in their consultation response of July 2018 that they are committed to raising awareness of the impending changes to the CGT reporting regime. In the author’s experience to date, awareness amongst taxpayers appears to be low and undoubtedly some will be caught unawares.