IHT traps

Share this article

Jacquelyn Kimber examines the new rules for residential property and also points out some traps and anomalies in the Business Property Relief rules

Key Points

What is the issue?

Since 6 April 2017, inheritance tax has become relevant to owners of UK residential property, irrespective of domicile and residence. Outside the realm of residential property, this complex tax can produce some surprising results.

What does it mean to me?

Trustees of excluded property trusts are now within the scope of inheritance tax, and will need to contend with the relevant property rules for the first time. For businesses, there are some common scenarios which cause headaches for those wishing to pass on business assets.

What can I take away?

There is a real question mark over how the new residential property regime will work in practice, particularly for non-residents. On the business side, a review of shareholder or partnership agreements could avoid unexpected liabilities.

The Finance (No 2) Bill 2017 is currently passing through Parliament and is expected to receive Royal Assent in December. F(No2)B 2017 enacts provisions relating to inheritance tax (IHT) affecting any non-UK domiciled individual owning UK residential property through a non-UK company or partnership. The changes will particularly affect ‘excluded property’ trusts owning, directly or indirectly, residential property portfolios. All references are to IHTA 1984 unless otherwise stated.

These provisions were first published in December 2016 with the expectation that they would become law with effect from 6 April 2017 when the Finance Bill 2017 was meant to become the Finance Act 2017. However, large swathes of the original Bill were cut following the shortened parliamentary timetable necessitated by the general election. Many people, including some advisers, thought the residential property provisions would be gone for good, or at the very least, delayed. Given the strength of HMRC’s views that there should be a level playing field between UK and non-UK domiciliaries owning UK residential property, the only real question was whether the changes would be deferred until 6 April 2018. Clearly not.

First, a reminder of the basics: UK domiciled individuals are within the scope of IHT on their worldwide assets. Pre 6 April 2017, non-UK domiciliaries were within the charge to IHT only in respect of UK assets (unless they had become ‘deemed UK domiciled’ through the 17/20 rule in s 267). Foreign situs property held by a non-domiciliary is ‘excluded property’ (ss 6 and 48), and is therefore outside the scope of the charge. It was common practice for non-domiciled individuals to hold UK situs assets – usually property – through an offshore company, ie a foreign asset. The company was normally owned by an offshore trust (an ‘excluded property trust’). From 6 April 2017, there is no practical difference from an IHT perspective between holding UK residential property directly or through a company. The position is summarised in table 1.

The changes are contained in new Sch A1, to be inserted by F(No2)B 2017 cl 33 and Sch 10. They work by removing from the definition of excluded property any value attributable to UK residential property, whether that is directly held, or through a non-UK company/partnership. This article focusses on property held through a company, as that is the more common structure.

A charge under the new rules will occur on any of the normal IHT chargeable events, such as death, a lifetime transfer to a trust etc. As it is the shares in the offshore company which are removed from the definition of excluded property, the value to be charged to IHT is that of the shares to the extent it relates to UK residential property, and not the value of the underlying property itself. Using HMRC’s example: ‘…a non-dom is the sole shareholder of an overseas company whose sole assets consist of a UK residential property. The company has no liabilities. At the individual’s death, their estate will consist of the overseas shares which have an open market value of £950,000. At the same time, the UK property has an open market value of £1 million. In such a situation, the value of the estate is £950,000, and this is derived wholly from the UK residential property. This would mean that IHT would be charged on the entire estate which has an open market value of £950,000.’

The position will be more complex where the company also holds foreign assets (which will continue to be excluded property), or there is debt. In the case of foreign assets, an apportionment is required on a ‘just and reasonable basis’ of the value to be attributed to the company’s shares. Any valuation will also need to take into account other relevant factors, such as inherent liabilities (CGT, ATED) and discounts for minority interests.

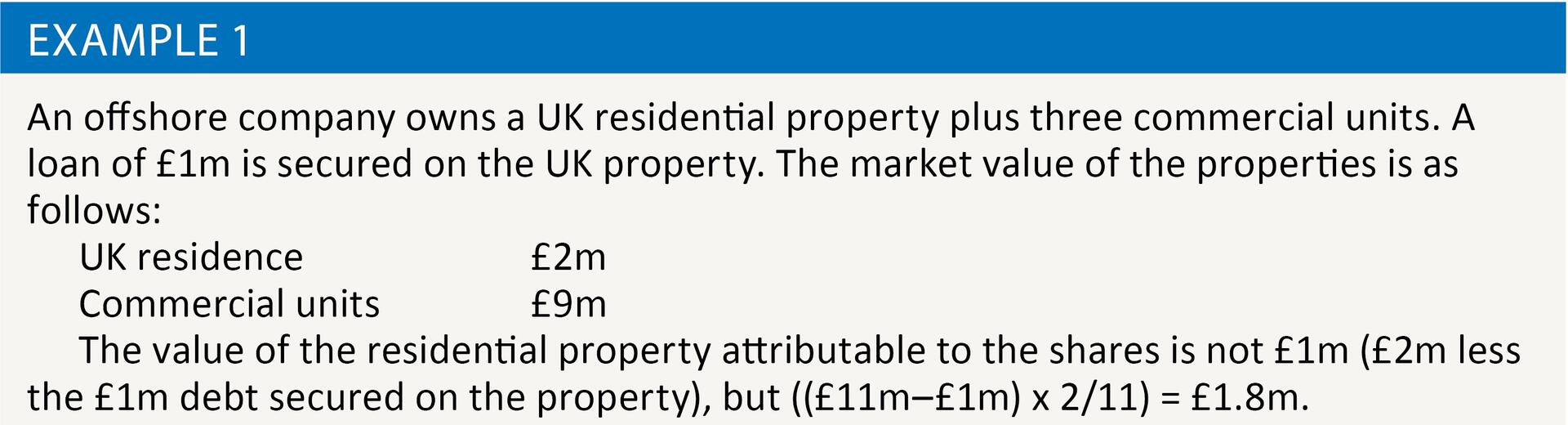

Debts of the offshore company are apportioned across all assets, even if a loan is secured on just the UK property. See example 1.

Sch A1 also catches the value of loans made to finance the acquisition, maintenance or enhancement of UK residential property, and security arrangements. Further, there is a two year time lag before the proceeds of a sale of (for example) a close company owning UK residential property, or the repayment of a debt, will be considered excluded property even if invested offshore.

Unlike the ATED rules, there is no escape from an IHT charge if the residential property is let on a commercial basis to third parties, or is used to provide employee accommodation. The scope of Sch A1 is broadly similar to the Non-Resident CGT introduced from 6 April 2015, and borrows key definitions such as ‘interest in UK land’ and ‘dwelling’ from those rules (TCGA 1992 Sch 1B). In practice, the majority of corporate structures will be caught unless the company is diversely held such that it is not a ‘close’ company (CTA 2010 s 439), or the interest falls within a 5% de minimis limit.

There are practical issues. If a non-domiciled individual ultimately owns foreign company shares deriving their value from UK residential property, an IHT charge arises on his death. But when an individual dies in a foreign country, it is unlikely that payment of UK IHT will be at the forefront of the personal representatives’ minds. The usual method of enforcement of IHT is that one cannot obtain a grant of probate or letters of administration without first paying the IHT for the estate. However, the property can be sold by the entity owning it without restriction, so unless there is some intricate tie up with the PSC register, international death records and the Land Registry, then how likely is it that HMRC will ever know? HMRC’s response is that a charge will be imposed on the UK residential property in their favour, however, that doesn’t entirely solve the information gap.

For trustees with offshore property companies, the changes are an unwelcome introduction to the IHT relevant property regime, particularly if the trust was settled in a year ending in 7 or 8. On the next tenth anniversary of the establishment of the trust, the trustees will be liable to a periodic charge in respect of their relevant property. Broadly, the rate of IHT is 6% (30% of the lifetime rate) multiplied by the value of the ‘no longer excluded property’, net of any allowable deduction for debt, multiplied by the number of quarters since 6 April 2017 divided by 40. HMRC are of the view that s 65(4) does not apply, so that the first quarter of the relevant property period is not excluded and the periodic charge clock started on 6 April 2017.

Exit charges under s 65 will also apply, although there is no charge where property ceases to be non-excluded property (for example, at the expiry of the two year ‘tail’ following a disposal of residential property (s 65(7C), (7D) as amended).

IHT arising under Sch A1 should be eligible for the instalment option (s 227) even if the property is owned by a company (note though that the overseas company will need to have share capital, so take care with US LLCs or similar vehicles).

There are no plans to add loans to the list of property eligible for payment by instalments in s 227, so IHT will be due within six months of the 10 year anniversary date. Whilst it seems harsh that related party loans are treated less favourably than the residential property itself for the purposes of IHT, this is in line with the position of UK domiciled individuals and trusts which were settled by a UK domiciled person, who are similarly not entitled to the instalment option on related party debt. For those hoping to make use of double tax treaties, unless the other country levies a similar tax on the value of the UK residential property at a rate other than 0%, treaty relief won’t apply. The UK has limited IHT double tax treaties, and although much planning has historically taken place using the UK:India IHT DTT, as India abolished estate duty some time ago, it offers no protection from UK IHT in this case.

HMRC maintain that there are no plans to introduce measures facilitating the de-enveloping of residential property structures. If ‘de-enveloping’ is being contemplated, there is a clear incentive to do this sooner rather than later, to minimise both capital gains and IHT charges. In any case, a review of the available options, together with wills and trust deeds is probably due.

Business Property Relief

Ensuring a business is able to continue as smoothly as possible following the death of a shareholder or partner requires careful thought. In many cases, the deceased’s family will have no interest in becoming involved in the business and the natural successors are fellow shareholders or partners. Further, the Partnership Act 1890 s 33(1) provides for a partner’s death to dissolve the partnership unless there are provisions to the contrary in the partnership agreement. The sensible commercial solution is to ensure that there is a written agreement in place securing that the deceased’s share passes to the continuing owners. The problem here is s 113 which states that property subject to a binding contract for sale at the time of a transfer of value is not relevant business property and does not therefore qualify for Business Property Relief (BPR) under s 105. Many pre-emption rights included in (for example) a company’s articles may be effective in securing the right commercial result, but could be fatal to a BPR claim.

Statement of Practice 12/80 sets out HMRC’s view that a right in a company’s articles to buy out the shares of a deceased shareholder means that the deceased has lost beneficial ownership of the shares, and therefore BPR is not available. The same analysis applies to rights under a partnership agreement. For this reason, it is standard planning to arrange for cross options to be granted, under which the surviving shareholders or partners have the option to buy and the deceased shareholder or partner’s personal representatives have the option to sell within a stated period after the individual’s death. Although an option is a contract for sale, HMRC have confirmed their view that the contract is conditional upon exercise by the option holder, and until that happens, the deceased shareholder has retained ownership of the shares (Spiro v Glencrown Properties Ltd [1991] 1 All ER 680). Given the potential amounts at stake, it is worth a thorough check of the articles or partnership agreement to ensure that the arrangement has been properly structured.

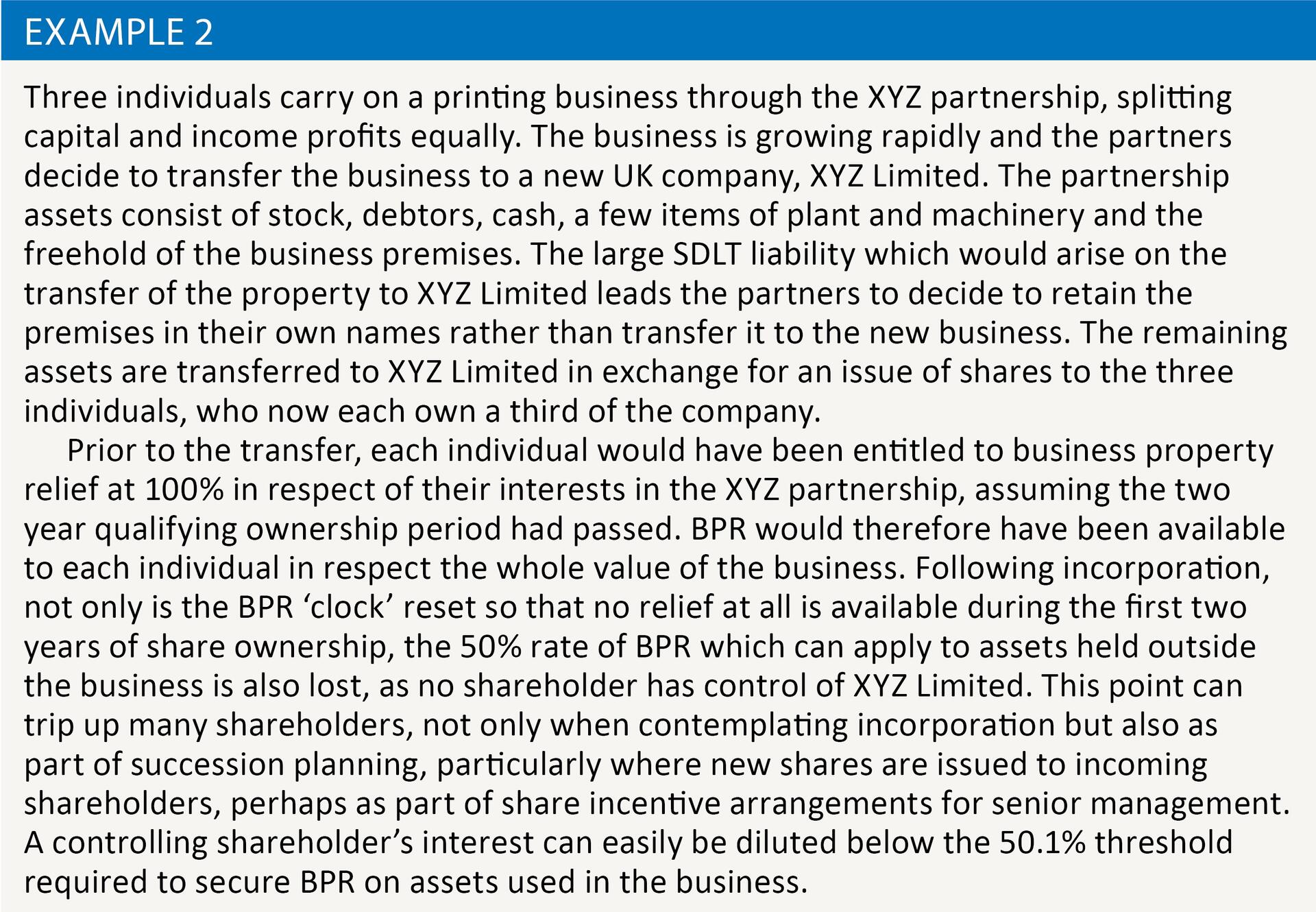

Another pitfall is the treatment of assets held outside a business, typically property. See example 2.

The IHT legislation is also anomalous in treating partnership interests as what I shall hesitantly refer to as ‘opaque’ for the purposes of BPR. On death, the property comprised in the deceased partner’s estate is the chose in action representing the partnership interest itself, and not the underlying partnership assets. This can catch out taxpayers and advisers alike, so familiar are we to the concept of partnerships as ‘transparent’ (again, the term is used as convenient shorthand). The trap is that shares in unquoted trading company (say) which would qualify for BPR if held directly by an individual will lose the relief if held through a partnership.

This treatment also (in HMRC’s view – see IHTM 25094) extends to LLPs, notwithstanding the wording of IHTA 1984 s 267A which states that for IHT purposes ‘property to which a limited liability partnership is entitled, or which it occupies or uses, shall be treated as property to which its members are entitled, or which they occupy or use, as partners…’. HMRC’s logic here is that the LLP’s holding of shares represents an investment activity and hence the prohibition at s 105(3) applies. Although HMRC’s view is questionable, especially in the light of the decision in HMRC v Nelson Dance Family Settlement Trustees [2009] STC 802 where it was held that the value transferred was attributable to the value of relevant business property, no change of view is likely without further litigation. Advisers should therefore be alert to the issue and look to restructure to avoid unexpected IHT bills.