Mind the gap

Share this article

Jacquelyn Kimber explores the 30 day reporti ng period to be implemented under the new capital gains tax regime

Key Points

What’s the issue?

From April 2020, the new capital gains tax regime will require a return to be made to HMRC within 30 days where there is any direct or indirect disposal of UK land by a non-resident, or a disposal of UK residential land by a UK resident resulting in a taxable gain, substantially increasing the number of UK land returns required to be filed.

What can I take away?

Raising awareness of the new reporting regime for UK resident taxpayers is clearly a priority. Part of the problem stems from the obligation to file a return falling in the gap between lawyers, estate agents and tax advisers.

What does it mean to me?

Calculating the capital gains tax payment should be straightforward for those with relatively stable sources of income – provided that the base cost is reasonably easy to ascertain. The position will be more complicated where income is erratic, where an event after the date of completion impacts overall income levels, where there is substantial enhancement expenditure, or where multiple disposals take place in

a tax year.

The new capital gains tax regime applying from April 2020 to property disposals brings with it a host of challenges, particularly for UK residents who have been used to reporting and paying capital gains tax as part of the self assessment tax system since 1997. Finance Act 2019 Sch 2 paras 1 and 2 require a return to be made to HMRC within 30 days where there is any direct or indirect disposal of UK land by a non-resident, or a disposal of UK residential land by a UK resident resulting in a gain. This article examines some of the practical challenges faced by UK resident taxpayers and their advisers.

The new UK land return is in addition to reporting a disposal on the normal Self Assessment tax return; it does not replace it.

For an overview of the new rules, see ‘All change!’ by Jacquelyn Kimber (Tax Adviser January 2020).

Reporting

The form of the return required to be submitted by UK residents under FA 2019 Sch 2 has not been released at the time of writing. FA 2019 Sch 2 para 16 merely contains the standard wording that the return must include a declaration by the person making it that the information is correct and complete to the best of the person’s knowledge, and contains information of a description specified by HMRC. HMRC will be testing the new system during February and March 2020.

The 30 day deadline

One of the biggest practical challenges of the non-resident capital gains tax (NRCGT) when it was introduced in April 2015 was making non-resident individuals, who perhaps have little or no nexus with the UK beyond the ownership of residential property, aware that they were required to file a return within 30 days of the disposal even if no tax liability arises. The number of late filing penalty and interest cases before the First-tier Tribunal in the four years since the NRCGT was introduced is testament to the challenges this presented.

The rules for UK residents from April 2020 offer some improvement, as a UK land return need not be filed unless capital gains tax is due. The obligation for non-UK residents to file a return where no liability arises is unchanged. In the majority of cases, it will be self-evident whether an individual is resident in the UK under the statutory residence test in FA 2013 Sch 45 (and any relevant double tax treaty). For others, such as those working abroad, the position may be much more complex and it will be necessary for the individual to determine their position before they can rely on the ‘no tax due’ exemption from filing a return. The position for trustees may be particularly problematic, as not only does the residence status of each individual trustee need to be determined, but the settlor’s domicile at the time the settlement was created may also be relevant (Income Tax Act 2007 s 474).

Raising awareness of the forthcoming new residential property gain reporting regime for UK resident taxpayers is clearly a priority. Again, using the NRCGT regime as an indicator, part of the problem stems from the obligation to file a return falling in the gap between lawyers, estate agents and tax advisers. Law firms do not generally get involved in their tax clients’ capital gains tax compliance obligations and dealing with tax matters will normally be excluded from their engagement letter. Similarly, tax compliance will normally be beyond the remit of an estate agent.

The obligation to file a return falls wholly on the taxpayer. Whilst tax advisers are (hopefully) doing everything they can to flag the forthcoming changes to their clients, experience suggests that clients are not always good at letting their adviser know they are about to sell an asset – and many taxpayers won’t have a tax adviser. Taxpayers tend to view their personal tax compliance obligations as an annual process, and by the time an adviser becomes aware of a residential property sale, the 30 day filing deadline may well have been missed. HMRC will no doubt direct taxpayers to its website for information; however, at the time of writing, the only information on gov.uk appears to be the July 2018 consultation response.

Even where taxpayers are aware of their obligations, there are other practical issues such as the need to obtain valuations; for example, a probate value where property has been inherited. Where the disposal (or acquisition) of property is by way of gift other than on death, a valuation at the date of gift will similarly be required. In a perfect world, advisers will have accurate and readily accessible information on their clients’ acquisitions of property, but for many the reality is likely to be a little different. Whilst there is nothing to prevent a ‘reasonable estimate’ being used to calculate the capital gains tax payment on account, any understatement of the taxpayer’s liability will lead to interest charges and possible penalties if the return contains careless errors.

Calculation assumptions

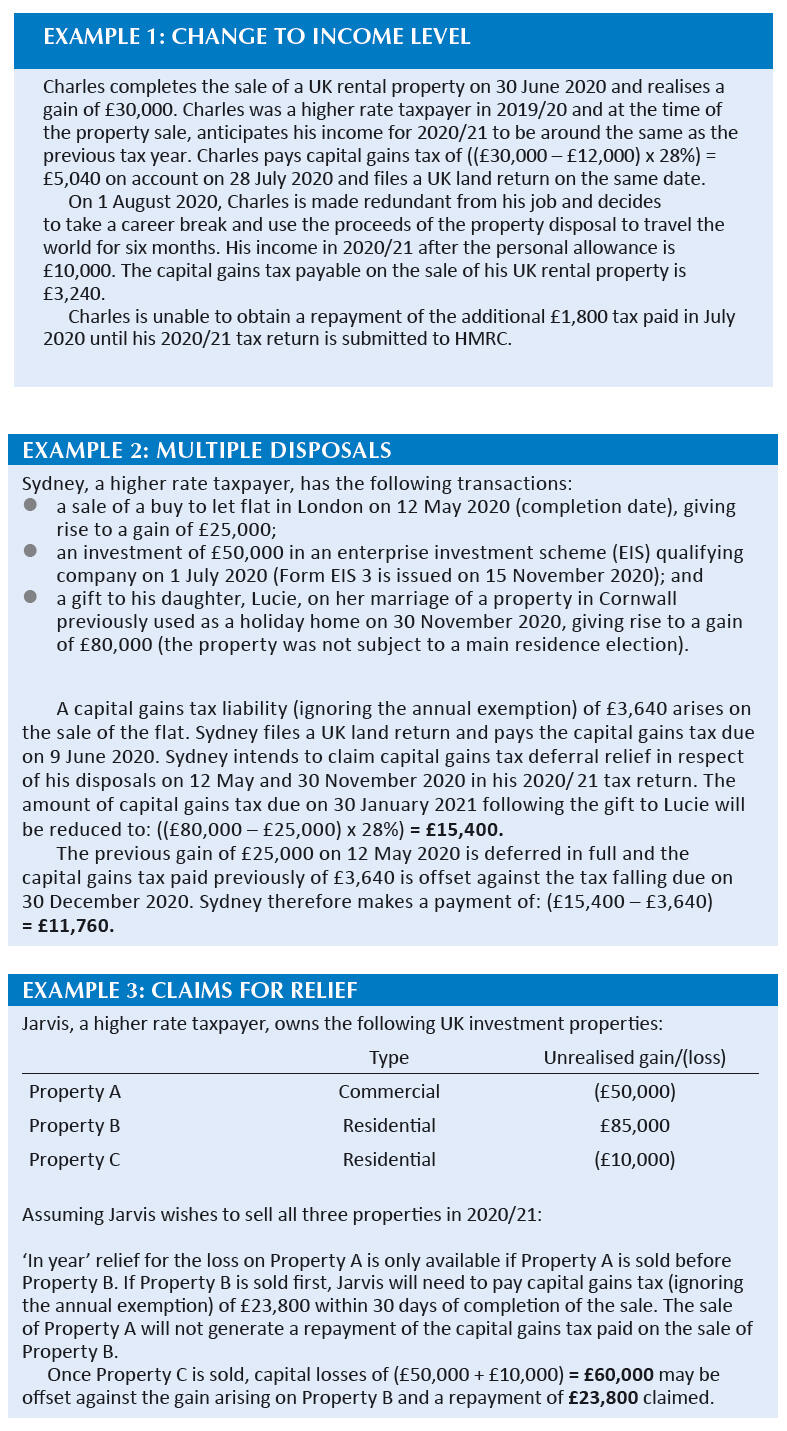

FA 2019 Sch 2 para 4 requires the taxpayer to assume that the tax year ends on the day on which a residential property disposal is made and assess his liability to capital gains tax in the UK accordingly. For those with relatively stable sources of income, it should be straightforward to estimate whether any part of the gain falls within the basic rate band (and therefore subject to capital gains tax at 18% rather than 28%). The position will be more complicated where income is erratic, or an event occurs after the date of completion which impacts overall income levels, such as redundancy (see Example 1).

Amendments to a UK land return are permitted (FA 2019 Sch 2 para 19) and the same time limits apply as for a self assessment tax return. However, an amendment is permitted ‘only so far as the return … could, when originally delivered, have included the amendment by reference to things already done’.

In Example 1, at the time Charles delivered his UK land return, he did not know he was about to be made redundant: his redundancy was not a ‘thing already done’, nor was it (presumably) anticipated. It therefore appears that he is unable to obtain a repayment of the tax paid until the UK land return is superseded by his 2020/ 21 self assessment tax return. Further guidance on this point from HMRC would be welcome.

Multiple disposals

Where there is more than one residential property disposal in a tax year, the amount of capital gains tax due on each subsequent disposal is calculated taking into account the tax paid previously.

Claims for relief

Claims for relief may be included in calculating the notional capital gains tax payable on a UK residential property disposal, provided the conditions for relief are met at the time the claim is made. In Example 2, Sydney is able to take his claim to capital gains tax deferral relief into account, as he has been issued with form EIS 3 before the tax liability on the Cornish property arose. Prospective claims for relief are not permitted; therefore, it would have been insufficient if Sydney merely had every intention of making a qualifying EIS investment at a future date.

The most common example of relief which is likely to be claimed is private residence relief under TCGA 1992 s 222. Where private residence relief applies for the entire period of ownership, then no UK land return will need to be filed. However, with the changes to lettings relief and the restriction of the final qualifying ownership period to nine months in the majority of cases, the situations where full private residence relief applies are likely to reduce.

The position will need to be checked in each case within the 30 day period in which a UK land return must be filed and no doubt there will be some unexpected liabilities and filing obligations.

Losses

As outlined in the January article, the rules on the offset of losses are one of the more contentious aspects of the April 2020 changes. To summarise:

- Losses brought forward at the start of the tax year (from any source) may be offset against a capital gain arising on the disposal of UK residential property.

- A loss arising on a disposal of UK residential property in the same tax year does not need to be reported on a UK land return, but a return may be filed in order to generate a repayment of tax paid on a residential property gain earlier in the same tax year.

- A loss arising on the disposal of any other asset after a residential property gain has arisen in the tax year will be offset (and a repayment of tax generated) in the taxpayer’s self assessment tax return for the year.

HMRC’s view is that any tax overpaid will attract a repayment supplement; however, this is unlikely to cut much mustard with taxpayers who are left waiting for substantial refunds by these rules (see Example 3: Capital losses in the January article).

In many cases, taxpayers will have limited ability to influence the timing of the completion of property disposals, as this will be subject to external factors. However, there are planning opportunities: if it is known that a disposal at a loss will take place in the tax year, then consideration can be given to ensuring that disposals take place in the most advantageous order.

Options

Under TCGA 1992 s 28, the disposal date for capital gains purposes is the date a binding unconditional contract for sale is entered into. Where the disposal of an asset is subject to an option, the date of disposal of that asset is generally the date the option is exercised and not the date the option is granted. The grant of the option itself is a disposal for capital gains tax purposes (namely of the option), but the subsequent exercise of the option does not constitute a separate disposal and the grant of the option and disposal of the asset are treated as a single transaction occurring on the date of the later transaction (TCGA 1992 s 144(2)).

FA 2019 Sch 2 para 13 makes clear that despite the ‘single transaction’ fiction created by s 144(2), a person granting an option over UK residential property remains subject to an obligation to file a UK land return and pay capital gains tax in relation to the grant of the option.

Conclusion

The new regime will be a challenge for taxpayers and advisers alike. There are some practical steps which advisers can take in terms of communicating the new rules to clients, as well as trying to bring records of residential property capital gains tax base costs up to date in readiness for the need to act swiftly once a property is disposed of. However, the difficulties in joining up the roles of estate agents, lawyers and tax professionals are very real as has already been demonstrated in the NRCGT regime.

The number of transactions subject to NRCGT was relatively small. The widening of the scope of residential property reporting regime to UK residents will substantially increase the number of UK land returns required to be filed. One hopes we do not also see a large increase in the number of late filing and late payment penalties being issued by HMRC.