The feeling’s mutual?

Share this article

Michael Steed examines the concept of mutuality of obligation and assesses its significance as we head for the new off-payroll working rules in the private sector, currently scheduled for April 2021

Key Points

What is the issue?

Mutuality of obligation (MOO) is a signifi cant feature of the broad ‘employed vs self-employed’ landscape (including IR35). Case law continues to develop in this area and criticism of HMRC’s CEST tool keeps this in the public eye.

What does it mean for me?

MOO is present in both tax and employment law cases and HMRC has a very different emphasis on its significance compared to the tribunals and higher courts.

What can I take away?

HMRC continues to defend a monocular construction of MOO that does not lie comfortably with leading case law. With off-payroll working rules currently scheduled in the private sector from April 2021, we need to be clear about the significance of MOO in future determinations of employment status.

It was the decision in Professional Game Match Officials Limited (PGMOL) [2020] UKUT 147 (TCC) on employment vs self-employment for football referees that once again brought the issue of mutuality of obligation (MOO) to the forefront. The phrase mutuality of obligation has been in use for years; but what does it mean and how (if at all) has its significance changed over the years?

I am not going to use this article to discuss employment law issues, except to the extent that they help us understand the tax issues. Rather it will address MOO as a concept, just as relevant in employment law cases as it is in tax cases (see for example Clark v Oxfordshire Health Authority [1998] IRLR 125).

The concept of mutuality of obligation

At its simplest, MOO is about the legal obligations that make up a contract. Both parties in a contract will have some obligations towards each other; and in a work-related contract, this will be the work/pay bargain.

Without some minimum degree of mutual obligation, you cannot have a contract. I will refer to this as ‘general MOO’.

However, it also has a more specific meaning. In tax cases (and employment law cases), it means a core component that must be present in order to create a contract of service (employment), as opposed to a contract for services (self-employment). I shall refer to this as ‘specific MOO’.

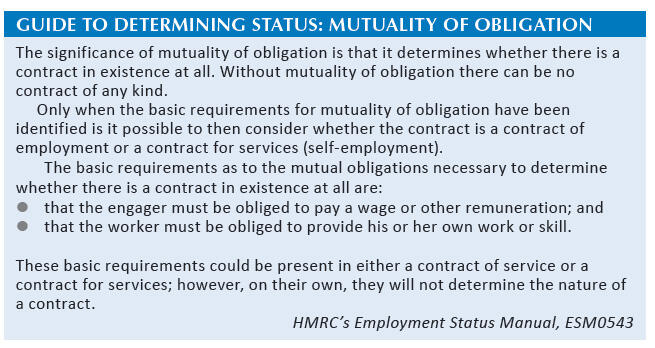

The position is complicated by HMRC using MOO as only relevant in determining whether a contract is in existence at all. This is set out in the box on the right, ‘Guide to determining status: mutuality of obligation’.

This is significant, as it appears to limit HMRC’s vision in respect of understanding MOO. This arguably becomes apparent when we look at the Check Employment Status for Tax (CEST) tool below.

In my view, it’s absolutely clear that MOO has a dual meaning and is used in two different but linked ways. In PGMOL, the Upper Tribunal said (para 100):

‘Mutuality of obligation is not only relevant to determining whether there was a contract at all, but is a critical element in delineating a contract of service from a contract for services.’

Just to be clear, this is just as much an issue in employment law cases too (see James v Greenwich London Borough Council [2008] EWCA Civ 35).

The MacKenna tests

Having said that MOO has both a general and a specific element, the core MacKenna tests in Ready Mixed Concrete (South East) Ltd [1968] QB 497 (RMC) are widely quoted in tribunals and higher cases as being a metric for employment (i.e. specific MOO). This states that a contract of service (i.e. employment) exists if three conditions are fulfilled:

- The servant agrees that, in consideration of a wage or other remuneration, he will provide his own work and skill in the performance of some service for his master.

- He agrees, expressly or impliedly, that in the performance of that service he will be subject to the other’s control in a sufficient degree to make that other master.

- The other provisions of the contract are consistent with its being a contract of service.

The Upper Tribunal (following common practice in tribunals) in the PGMOL case, referred to the first element as the ‘mutuality of obligation’ requirement and the second element as the ‘control’ requirement. (As a personal comment, I’m always struck by the old-fashioned language employed by Judge MacKenna, even though this was written in 1968.)

I take the ‘own work and skill’ requirement in point 1 as covering the ‘substitution’ issue as well (not dealt with here in the interest of space). I am not going to deal with the ‘control’ issue either, for the same reason.

The significance of the PGMOL decision

In my view, this decision is important because it highlights the difference in approach to MOO taken by the Upper Tribunal to that taken by HMRC. This is especially so, in respect of the criticism of the CEST tool, by contractors and others, and the comments on the tool by the House of Lords (see below).

PGMOL was an HMRC appeal to the Upper Tribunal from a First-tier Tribunal decision that a group of freelance football referees were self-employed and not employed by PGMOL. In this case, there was an overarching contract between the two parties and specific contracts for each game.

The Upper Tribunal found for PGMOL again and held that it had no reason to disturb the First-tier Tribunal’s decision either on misdirections in law grounds, or a perverse finding of fact on the underlying principal of Edwards v Bairstow [1956] AC 14. It’s hard not to conclude that HMRC was pretty comprehensively drubbed in the Upper Tribunal, with few of HMRC’s arguments finding favour with the judges.

This is, however, clearly a very sensitive issue with HMRC, as it has subsequently appealed the decision.

To my eye, the key point about the PGMOL case is the repeat of HMRC’s contention that MOO is relevant only to the questions of whether there is a contract at all; and, if there is a contract, whether it contains an obligation to provide services personally and obligations which are in some way ‘work related’.

HMRC said that MOO is not relevant to the question of whether such contract is one of employment or a contract for services.

It is significant that the Upper Tribunal in PGMOL rejected this narrow construction of MOO (para 100):

‘As we have already concluded, however, mutuality of obligation is not only relevant to determining whether there was a contract at all, but is a critical element in delineating a contract of service from a contract for services.’

The impact of CEST

The CEST tool has been around for a while now and is in about its fourth incarnation; its development has been messy. Do you remember the IR35 ‘Business Entity Tests’ tools that were introduced by HMRC in 2012 and quietly dropped in 2015 as they just added to the confusion?

What CEST is supposed to do – and arguably does in about 80% of contractor cases, according to the House of Lords Report (see below) – is to give certainty about a contractor’s tax status. A taxpayer should be able to depend on the output, provided that the questions have been answered accurately.

However, that means that up to 20% of contractors will not get a result from the tool. In a population of around 230,000 contractors in the UK, a significant number will not get an answer and will have to determine their status by other methods.

There has been a significant groundswell of criticism of CEST, most noticeably and predictably from contractor representative bodies and websites. Probably the most consistent criticism is that the tool does not properly address the MOO issue.

In December 2019, HMRC, clearly stung by the adverse comment on MOO and its apparent lack of appearance in the CEST tool, published its response through the IR35 Forum, saying:

‘CEST does not explicitly look at MOO, it is designed to determine whether an existing or future contract will be one of employment or self-employment. It is assumed that a person using CEST will have already established MOO, which is necessary for a contract to exist, otherwise there would be no need to be using CEST to determine the status of the existing or hypothetical contract.

‘We will consider a range of factors to establish whether a contract is an employment contract or a contract for services. This is distinct from consideration of mutuality of obligation, which will already have been established. For the avoidance of doubt the CEST online tool assumes that a contract exists or is being considered. We do not anticipate the tool being used outside of these circumstances.’ (italics mine)

It’s hard not to conclude that HMRC’s monocular vision on MOO is being reinforced here and is out of step with the Upper Tribunal and higher courts.

The House of Lords’ response

The House of Lords Economic Affairs, Finance Bill Sub-Committee published a report in April 2020 called ‘Off-payroll working – treating people fairly’. Its remit was to examine the off-payroll working rules and to determine, among other things, whether it was fit for purpose in the private sector from April 2021. The House of Lords committee concluded that IR35 is a flawed system (para 30):

‘They separate employment status for tax purposes from employment status under employment law. This distinction is unacceptable, not least because it fails to acknowledge that contractors bear all the risk for providing the workforce flexibility from which both parties benefit.’

The committee also concluded that extending the off-payroll working rules to the private sector without a proper evaluation of the effect of these rules in the public sector was wrong. It had reservations about the CEST tool too – and took evidence from many witnesses that CEST did not, in its view, fully reflect the case law. This is notwithstanding that the Financial Secretary to the Treasury wrote that CEST had been ‘rigorously tested against established case law and settled cases’ to ensure that it gave accurate results (para 73).

The other main criticism of CEST from the witnesses was that CEST did not address MOO or if it did, it did so no more than obliquely, perhaps in the business on own account (financial risks) questions (see also Market Investigations Ltd v Minister for Social Security [1969] 2 QB 173 and Hall (HM Inspector of Taxes) v Lorimer [1993] BTC 473). HMRC argued before the committee that CEST did address MOO but acknowledged that others disagreed.

Conclusion

So, where are we now? We ostensibly have a flawed system (IR35) and a tool in CEST that falls short of what is required. Yet unless the situation changes due to Covid-19, we are heading for off-payroll working in the private sector in April 2021.

What we actually need is certainty and easily understood rules that properly accord with case law. A bridge too far?