Grappling with complexities

Share this article

Stuart Pibworth examines the UK rules to determine whether a non-UK tax resident company has a UK permanent establishment

Key Points

What is the issue?

The taxation of permanent establishments (PEs) has become an increasingly important topic for global business following the close domestic and international focus on this area in recent years. Where a company has a PE the tax implications should be considered along with the impact on business structuring and financial modelling.

What does it mean to me?

The UK rules to determine whether a non-UK tax resident company (Non-ResCo) has a UKPE are far from straightforward. However, it is important to understand and identify the circumstances in which Non-ResCo has a UKPE and the UK tax implications of having a UKPE. Although the OECD’s recommendations on Action 7 of the BEPS project may not directly impact on the UK taxation of PEs, advisers should be aware of these recommendations and the possible impact on UK tax resident companies and their overseas operations.

What can I take away?

Whether Non-ResCo has a UKPE is a factual question determined by applying the applicable rules (including anti-avoidance rules (such as the UK diverted profits tax) and the provisions of any double tax treaty) to the circumstances at hand.

Over recent years the taxation of permanent establishments (PEs) has been subject to close domestic and international attention and so become an increasingly important topic for global business. This heightened focus has necessitated global businesses (re)considering whether their operating structures give rise to PEs and any resulting tax implications.

This article provides a practical overview of the circumstances in which a non-UK tax resident company (Non-ResCo) has a PE in the UK (UKPE), the UK tax consequences of having a UKPE and the impact of Action 7 of the OECD BEPS project.

Taxation of UKPEs

Non-ResCo is subject to UK corporation tax (CT) if:

- it is trading (applying the ‘badges of trade’);

- in the UK (distinguishing trading ‘in’ the UK and trading ‘with’ the UK, the key question being ‘where do the operations take place from which the profits in substance arise?’);

- through a UKPE.

Subject to certain exceptions, Non-ResCo has a UKPE if:

- it has a fixed place of business (PoB) in the UK through which a business is wholly or partly carried on (the Fixed Business Test); or

- an agent acting on behalf of it has, and habitually exercises in the UK, authority to do business on behalf of Non-ResCo (the Agency Test).

Whilst each UKPE test refers to a business (being broader than a trade), the effect of limb (1) above is that Non-ResCo will only be subject to corporation tax (CT) if UKPE undertakes trading activities (although even if Non-ResCo does not have a UKPE, it may be subject to CT on profits from trading in and developing UK land ,and possibly, pending the outcome of the current government consultation, income (and certain gains) from UK land).

Fixed Business Test

In addition to the indicative list of place of businesses (PoBs) at CTA 2010, s 1141(2), HMRC guidance provides that the Fixed Business Test normally requires:

- a physical PoB (the Geographic Condition);

- a degree of permanence (the Time Condition); and

- a business carried on at the PoB by Non-ResCo’s personnel (the Personnel Condition).

Geographic condition

There must be a distinct PoB where the activity is undertaken whether or not that PoB is used exclusively for that activity. Some points to watch out for:

- plant and machinery (including automated equipment) may constitute a PoB if the activities are restricted to setting up, operating, controlling or maintaining it;

- a PoB does not need to be owned or rented by Non-ResCo provided that it is otherwise at the disposal of Non-ResCo (which may be indicated by Non-ResCo having business cards with the PoB stated as the address);

- regular visits to a customer’s office should not ordinarily give rise to a PoB;

- a PoB only requires a place (and not necessarily premises) if the activities are appreciably undertaken from that place (e.g. street vendors);

- where activities are undertaken in adjacent locations, a single PoB (not multiple PoBs) may exist where, given the nature of the business, the adjacent locations together constitute a coherent whole geographically and commercially (e.g. this may be relevant where there is a large construction site);

- a PoB may exist where one company has space (e.g. an office) in the premises of another company (including an affiliate).

Time condition

Whilst not defined, the requirement for the PoB to be ‘fixed’ implies that a UKPE may only exist if the PoB has a certain degree of permanence i.e. it is not purely temporary. Whether the requisite degree of permanence exists depends on the circumstances but may include factors such as whether Non-ResCo has a UK bank account, the duration of any tenancy and other commercial arrangements, and the business plan.

A PoB may constitute a UKPE even though it exists, in practice, only for a short time. However, subject to certain exceptions (e.g. recurrent activities or temporary interruptions), HMRC’s general rule is that a PoB may not constitute a UKPE if it exists for less than six months.

A UKPE begins to exist as soon as the real (i.e. non-preparatory) business activities commence through the PoB and cease when such activities cease.

Where a PoB was originally designed to be purely temporary but is actually maintained for such period that it is no longer considered temporary, it becomes a fixed PoB and retrospectively is treated as such from the date on which the originally intended temporary activities commenced.

Personnel condition

Personnel working in Non-ResCo’s business (e.g. employees or consultants) must actually work from the PoB. For example, if personnel simply visit the PoB they should not be regarded as working from there.

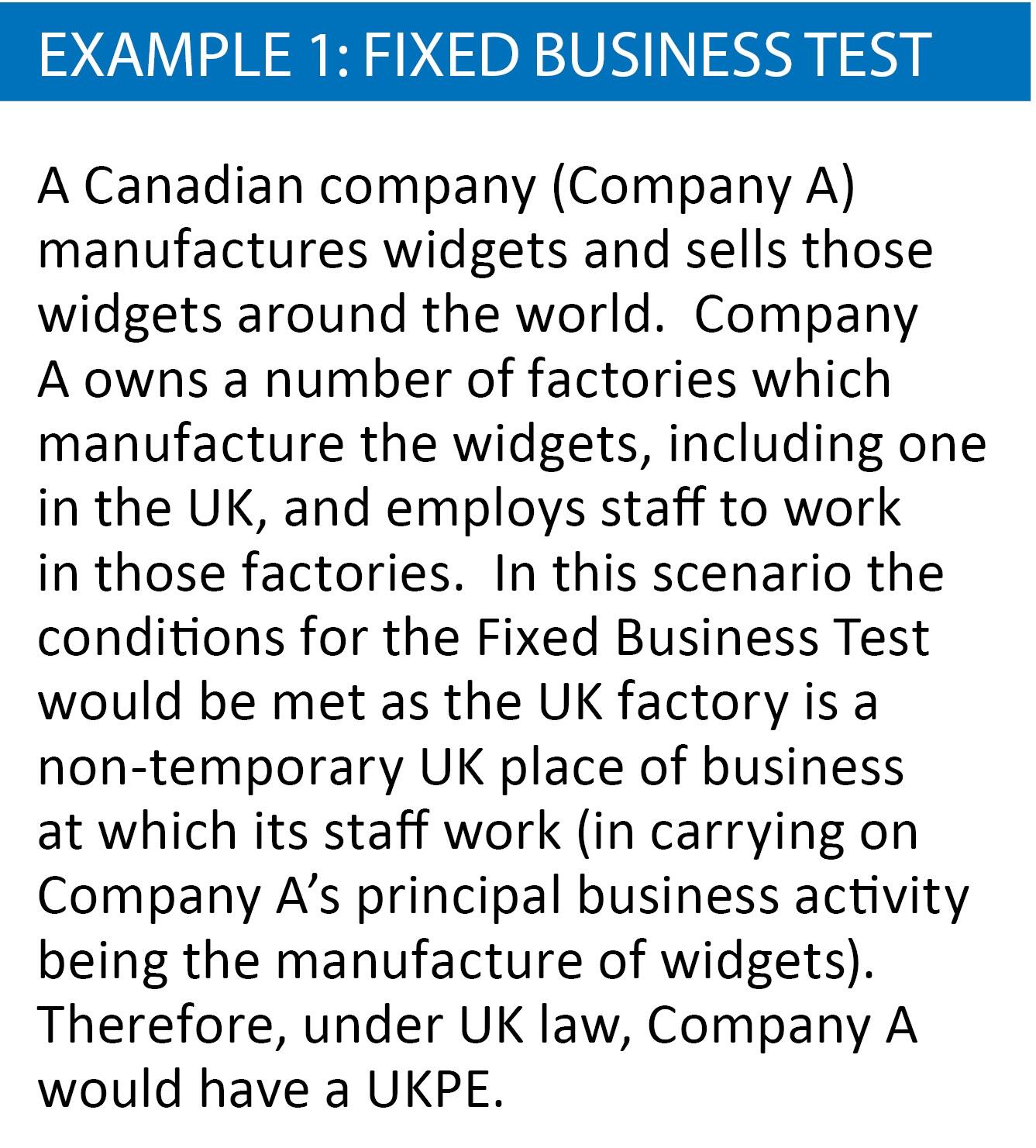

See example 1.

Agency Test

Whether an agency relationship exists is a legal question. Broadly, an agent is a person who represents the principal (i.e. Non-ResCo) in accordance with the terms of the agreement between them and, in so doing, may bring about a legal relationship between the principal and a third party (e.g. the conclusion of a contract on the principal’s behalf with a third party). In other words, an agency relationship exists where, effectively, acts of the agent are regarded as acts for or on behalf of Non-ResCo.

Accordingly, the terms of the agreement between the agent and Non-ResCo need to be carefully considered to determine, among others, whether the agent:

- has the ability to bind Non-ResCo in any way or exercise any discretion (including negotiations) on behalf of Non-ResCo;

- can enter into contracts on behalf of Non-ResCo;

- has authority to act on behalf of Non-ResCo;

- has a clearly defined scope of operating activities.

However, whether an agency relationship exists turns on what actually happens rather than the provisions of the agreement i.e. if the agreement restricts the agent’s authority but, in practice, the agent binds Non-ResCo, there may be an agency relationship.

Notwithstanding the above, an agent should not constitute a UKPE of Non-ResCo if it is of an independent status acting in the ordinary course of its business (with special rules for brokers, investment managers and Lloyd’s agents).

Whether an agent is independent is tested by reference to the legal, financial and commercial relationship between the agent and Non-ResCo. Factors to consider include:

- the extent of the agent’s obligations vis-a-vis Non-ResCo;

- the number of unrelated principals for which the agent acts;

- the level of control exercised by Non-ResCo;

- whether the agent bears the entrepreneurial risk for the business it carries on for Non-ResCo;

- the degree of Non-ResCo’s reliance on the agent’s skill and knowledge;

- whether the agent requires Non-ResCo’s approval of the manner in which its business is conducted.

In short, the question is whether the relationship between the agent and Non-ResCo is the same as a relationship between independent businesses dealing with each other at arm’s length. If the agent acts for other independent unconnected businesses on the same terms as those under which it acts for Non-ResCo, the independence test may be met.

A parent-subsidiary relationship does not automatically result in the subsidiary being a dependent agent of the parent; the factors described above should be considered.

Whether an agent acts in the ordinary course of its business is determined by reference to what actually happens (and not the parties’ intentions), with factors including the number of unrelated principals for which the agent acts and the extent of business activities customarily undertaken by independent agents in that industry sector.

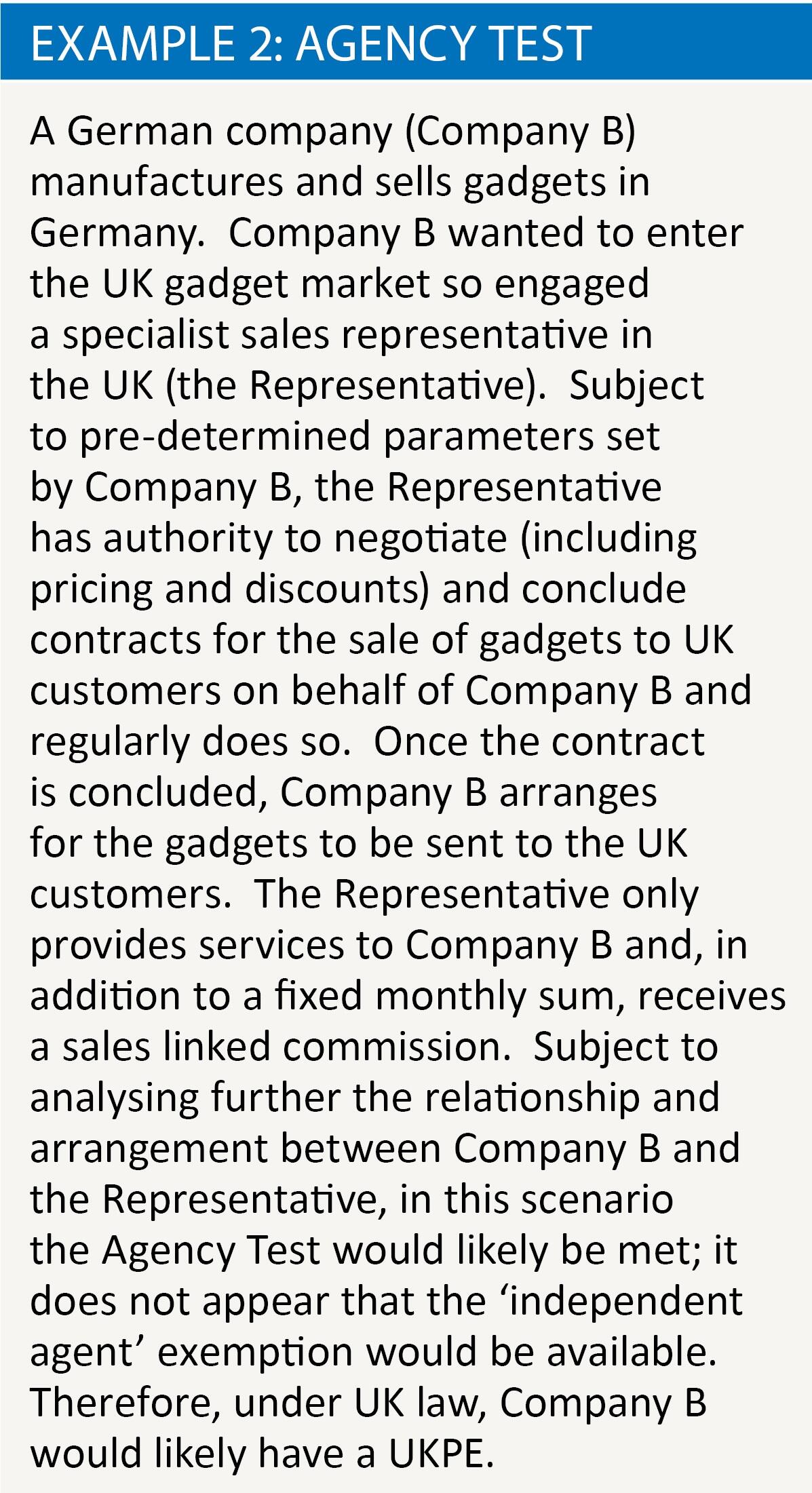

See example 2.

Preparatory or auxiliary activities

Non-ResCo does not have a UKPE under either test if the UK activities are, in relation to Non-ResCo’s business as a whole, of a preparatory or auxiliary character. CTA 2010, s 1143(3) contains a non-exhaustive list of such activities. Whether a particular activity is preparatory or auxiliary is a factual question including consideration of:

- the remoteness of the UK activities from the actual realisation of profits by Non-ResCo – the more remote the less likely that Non-ResCo will have a UKPE;

- whether the activity forms an essential and significant part of Non-ResCo as a whole – the more closely aligned the UK activities are to the general purpose of Non-ResCo, the more likely that a UKPE would exist.

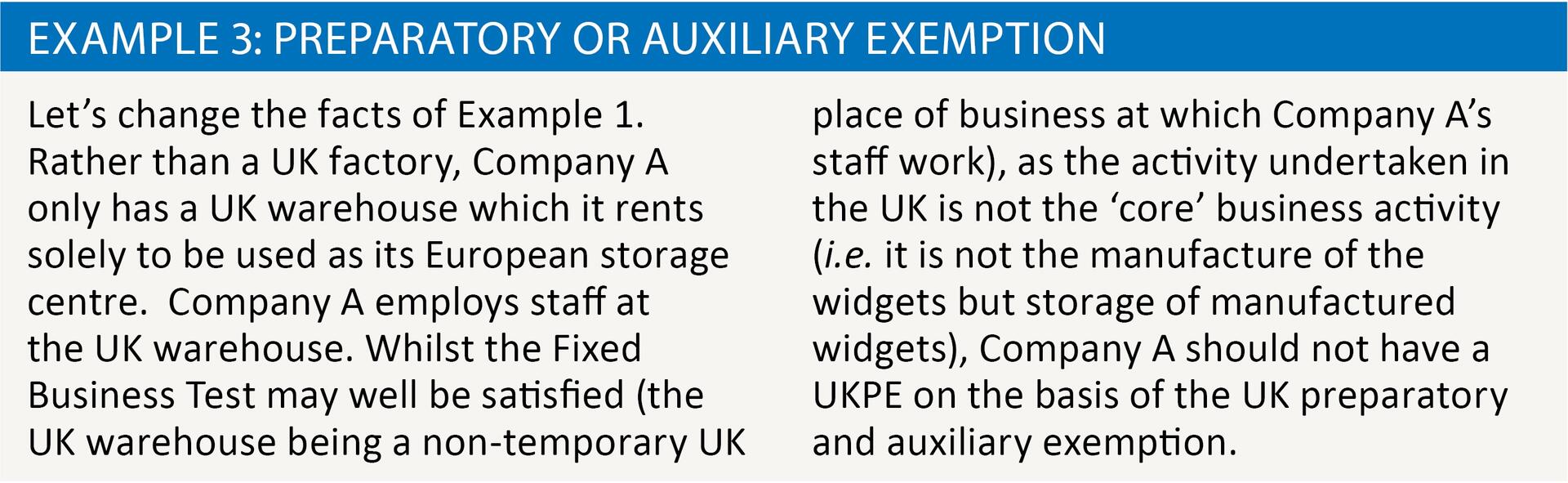

See example 3.

Practicalities

If Non-ResCo does not have a UKPE applying the rules described above, the applicability of any anti-avoidance provisions, including the diverted profits tax, should not be overlooked.

Where Non-ResCo has a UKPE, Non-ResCo should notify HMRC within three months of commencement of the UK activities giving rise to the UKPE.

In assessing, collecting and recovering CT payable by Non-ResCo UKPE would be treated as Non-ResCo’s UK representative. Consequently, (i) the obligations and liabilities of Non-ResCo (e.g. filing and payment obligations) are treated as if they were UKPE’s obligations and liabilities, and (ii) subject to limited exceptions, Non-ResCo is bound by UKPE’s acts and omissions in the discharge of those obligations and liabilities.

As a practical point, because UKPE is Non-ResCo’s UK representative a UTR should be allocated to it in that capacity (which should occur automatically where notification to establish a PoB is made to Companies House).

If Non-ResCo does not settle any part of its CT liability within six months of the due date for payment, within applicable time limits HMRC can serve a notice on a ‘related company’ of Non-ResCo (being certain group companies and consortium members) requiring it to pay all or part of the unpaid tax.

Profit attribution

Where Non-ResCo has a UKPE it will be subject to CT on the profits attributable to that UKPE including:

- trading income arising directly or indirectly through or from UKPE;

- income derived from property held by or for UKPE;

- certain chargeable gains of UKPE.

For these purposes, the separate enterprise principle (the SEP) should be applied in attributing profits to UKPE. Under the SEP, the profits attributable to UKPE are those it would have made if it were a distinct and separate enterprise from Non-ResCo which: (i) engaged in the same (or similar) activities under the same (or similar) conditions as Non-ResCo; and (ii) deals with Non-ResCo wholly independently.

As the SEP effectively operates as a transfer pricing mechanic, HMRC notes that its transfer pricing practice should be considered when applying it. Given this, it will also be important to consider any impact the OECD’s transfer pricing guidelines and BEPS recommendations have on PE profit attribution.

In addition to the SEP, there are other rules that impact on the computation of UKPE profits (including restrictions on tax deductibility of certain costs). These should not be overlooked, in particular when considering how to finance UKPE.

Double tax treaties (DTTs)

Whether Non-ResCo has a UKPE is solely determined by UK law. If Non-ResCo does not have a UKPE under UK law, then a DTT cannot override UK law, deem a UKPE to exist and impose a CT charge.

However, a DTT may be relevant when Non-ResCo has a UKPE under UK law. Where a DTT containing a PE provision exists between the UK and the jurisdiction of tax residence of Non-ResCo, the DTT may allocate taxing rights as between the two jurisdictions (and so avoid double taxation) or override the UK domestic position (and so limit the CT charge). For example, in the fund context, where a UK investment manager is treated as the fund’s agent (UKPE) under UK law (i.e. the UK exemption for investment managers is not available), if the ‘agent of independent status’ exemption in a DTT applies the UK investment manager would not be treated as a UKPE of the fund.

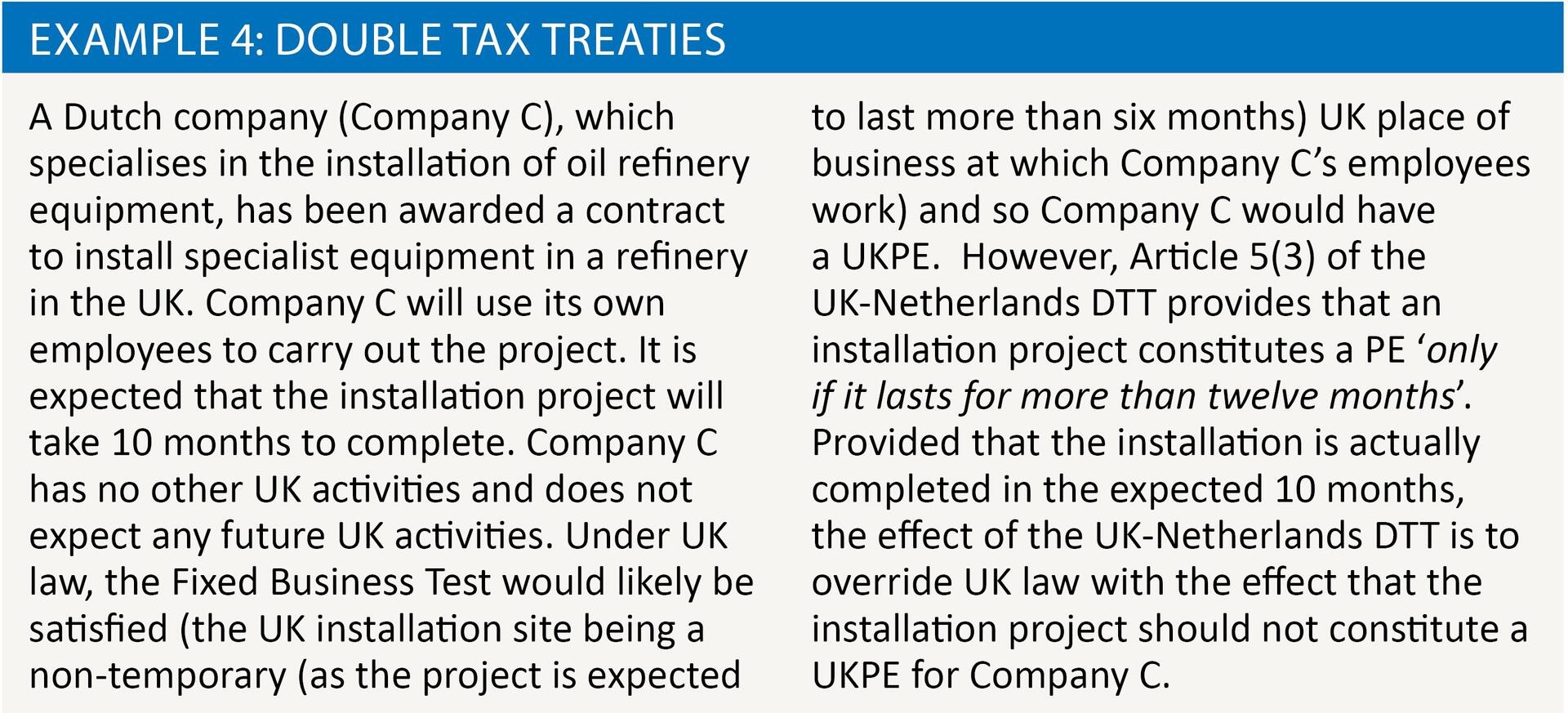

The effect of any DTT depends on the provisions of that DTT and also requires consideration of anti-avoidance rules and any anti-abuse provision(s) in the DTT (e.g. a limitation of benefits (LOB) or principal purpose test (PPT) provision). See example 4.

BEPS Action 7

BEPS Action 7 addresses certain strategies to avoid having a PE under the provisions of existing DTTs. The particular concerns are:

- commissionaire (and other similar) arrangements;

- the use of the preparatory or auxiliary exclusion to core business activities;

- other strategies to avoid artificially having a PE, including the fragmentation of activities into several small operations.

To address these the OECD recommended the following amendments to its Model Tax Convention:

- expanding the PE definition to cover both persons who habitually conclude contracts and persons who habitually play the principal role leading to the agreement of terms that are routinely concluded by way of contract without material modification;

- clarifying that each of the activities listed in the PE exemption provision must be of a preparatory or auxillary nature;

- introducing an anti-fragmentation rule requiring activities of closely related enterprises in the same jurisdiction to be aggregated in determining whether the overall activities carried on in that jurisdiction are preparatory or auxiliary;

- clarifying that an agent should not be treated as independent where it acts exclusively (or almost exclusively) for one or more enterprises to which it is closely related.

Subject to reservation, the OECD Action 7 recommendations are included as part of the OECD Multilateral Convention, which was signed in June 2017. It is understood that the UK will not implement these changes (save the anti-fragmentation rule and ‘closely related’ definition) and, separately, will not amend the UK domestic PE definition to reflect Action 7. Accordingly, at this stage, from a UK perspective, the UK rules described above will continue to apply without modification.

However, whilst this may be the case for Non-ResCos and their UK activities, the position may be different for UK tax resident companies (UKCos) and their overseas activities. Whether such UKCos have overseas PEs (OPEs) will be a question for the relevant local law and any DTT. Accordingly, UKCos with global operations will need to be mindful of Action 7 and the impact this may have on their overseas operations. To the extent that UKCo has an OPE relief from double taxation may be available under the UK’s system of unilateral relief, the provisions of an applicable DTT or by making an OPE election.

Final remarks

In a post-BEPS environment, businesses are having to grapple with the complexities inherent in the taxation of PEs and apply the rules to their operating structures. In practice, this can be far from straightforward. Given the fast-evolving nature of this area, businesses should continue to monitor developments in this field, being mindful of their potential effect on business structuring, tax implications and impact on financial modelling.