Growing investment

Share this article

Stuart Pibworth on how the new QPP Exemption will simplify processes and encourage debt investment into the UK

Key Points

What is the issue?

With effect from 1 January 2016, a new exemption from UK withholding tax on payments of yearly interest, known as the Qualifying Private Placement Exemption (QPP Exemption), was introduced to sit alongside the existing domestic exemptions

What does it mean to me?

The stated aim of the QPP Exemption as part of the consultation process was to develop the UK private placement market. However, there is nothing in the definition of a QPP for these purposes which requires there to be a ‘private placement’.

What can I take away?

The QPP Exemption should simplify the process for overseas lenders lending into the UK (in particular, by eliminating the administrative requirements associated with a claim for relief under a double taxation treaty) and so encourage debt investment into the UK.

Where a UK corporate debtor makes payments of yearly interest to, among others, non-UK creditors, the debtor will be required to withhold an amount representing UK income tax (currently at a rate of 20%) from that payment and account to HMRC for the same. Generally, this mechanic is referred to as a ‘withholding tax’. However, that debtor will not be required to withhold where a domestic exemption, EU directive or double taxation treaty applies to eliminate the UK withholding tax.

With effect from 1 January 2016, a new exemption from UK withholding tax on payments of yearly interest, known as the Qualifying Private Placement Exemption (QPP Exemption), was introduced to sit alongside the existing domestic exemptions. In March 2018, HMRC published its guidance (the Guidance) on the practical application of the QPP Exemption in its Savings and Investment Manual.

The QPP Exemption: the gateway conditions

The QPP Exemption is set out in section 888A, Income Tax Act (ITA) 2007 and the Qualifying Private Placement Regulations 2015 (SI 2015/2002) (the Regulations) and came into force on 1 January 2016.

The QPP Exemption applies to interest payments on a qualifying private placement (QPP) which is defined as a security which:

a. represents a loan relationship (as defined in CTA 2009 Part 5) to which a company is a party as debtor (so the QPP Exemption is not available where the debtor is not a company);

b. is not listed on a recognised stock exchange (as, in that case, ordinarily the Quoted Eurobond exemption should apply); and

c. meets additional conditions specified by Treasury regulations (currently being the Regulations).

Scope of the QPP Exemption

The stated aim of the QPP Exemption as part of the consultation process was to develop the UK private placement market. However, there is nothing in the definition of a QPP for these purposes which requires there to be a ‘private placement’ (as that expression is generally understood). Instead, the QPP Exemption requires a security which satisfies the relevant conditions, including a security which represents a loan relationship (ITA 2007 s 888A(6) confirms that loan relationship for these purposes has the same meaning as under the UK loan relationship rules which apply to a broad range of debt instruments). The broad scope of the QPP Exemption is recognised by HMRC in the Guidance.

What is a security?

‘Security’ is not specifically defined in the QPP Exemption. However, the Guidance notes that it encompasses a wide range of debt instruments that are capable of being transferable investments. The Guidance notes that:

- a ‘security’ does not require a lender to have rights over assets put up as security for the debt;

- there is no requirement for a security to take a particular form, it can take the form of a note or a loan; and

- consistent with the broad scope of the QPP Exemption, ‘loan-like agreements are not precluded from the exemption by the use of the term ‘security’ in the gateway condition’.

Whilst ‘security’ is not specifically defined, the Regulations provide that the definition of a ‘relevant security’ includes a security or a loan relationship. This lends further support to the view that the QPP Exemption should apply in respect of any debt arrangements provided that the relevant conditions are satisfied.

The QPP Exemption: Additional conditions

As noted above, for the QPP Exemption to apply the security must meet the additional conditions set out in the Regulations. These additional conditions will be satisfied where the security in question:

a. has a term not exceeding 50 years (Term Condition);

b. satisfies the minimum value requirement (Minimum Value Condition); and

c. is being entered into for genuine commercial reasons and not as part of a tax advantage scheme.

Term Condition

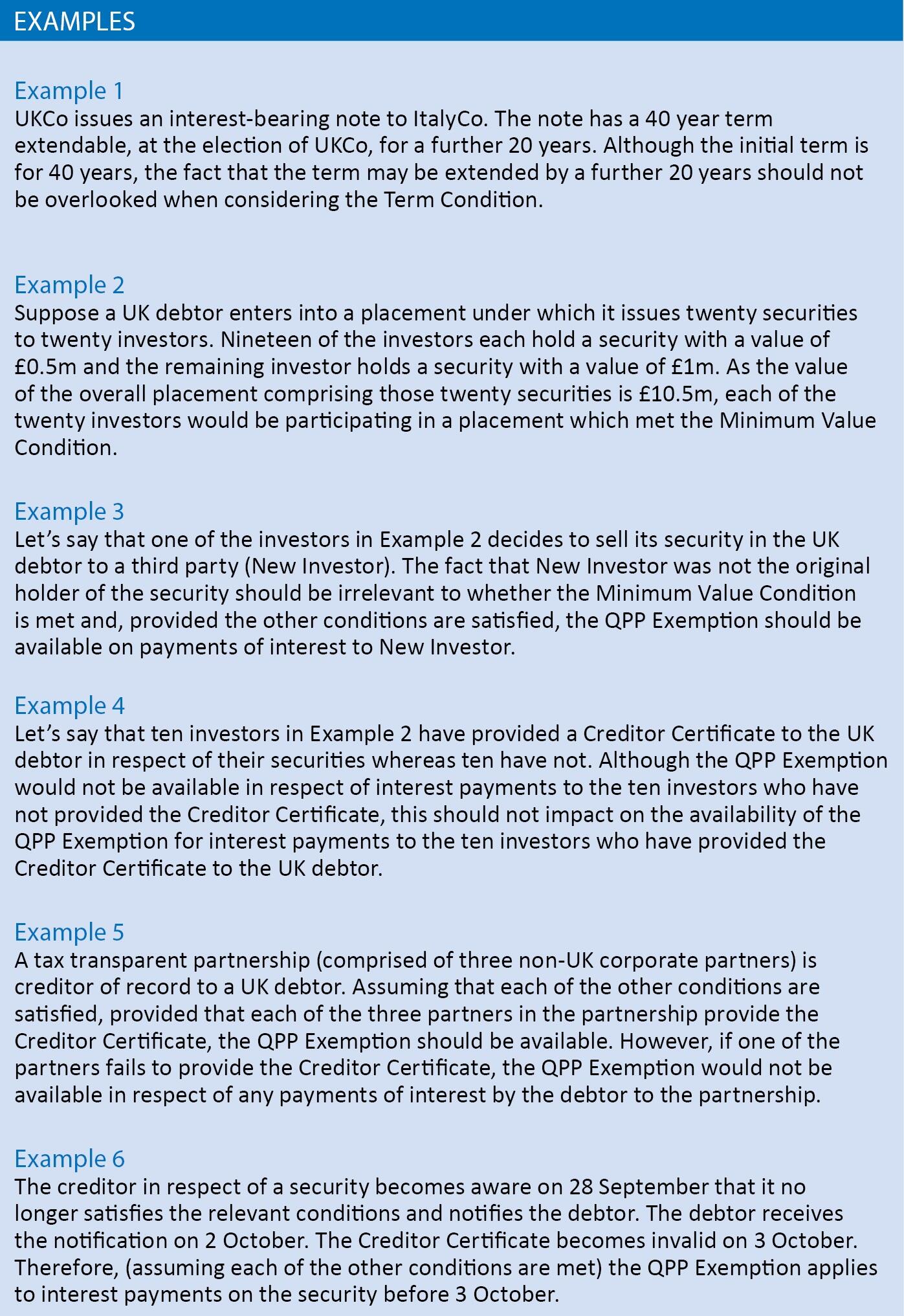

The term of the security cannot exceed 50 years. Therefore, clearly, perpetual debt instruments cannot qualify for the QPP Exemption. However, care should also be taken where a security has an initial term of less than 50 years but which may be extended beyond 50 years (see example 1).

Minimum Value Condition

The security must:

- have a minimum value of £10m; or

- where a placement consists of multiple securities of the same debtor, form part of a placement which has a minimum value of £10m (see example 2).

The Guidance confirms that the £10m value means the Sterling value when the security in question was entered into and not at any other time (so repayments over the term of the security which may reduce the value below the £10m threshold should be disregarded). In other words, the Minimum Value Condition is a one-off condition determined at the date the security was entered into. Therefore, provided the other conditions are met, the transfer of a security by an original creditor should not impact whether the Minimum Value Condition is met and so the transferee should, assuming it meets the applicable conditions, be eligible to be paid interest free of UK withholding tax (see example 3).

Practical issues may arise when applying the Minimum Value Condition where the amount is drawn down under the security in tranches. The Guidance notes that:

- where the initial amount advanced is £10m or more, further amounts will be considered part of the original QPP, and within the scope of the QPP Exemption, even if the subsequent drawn down is less than £10m;

- where the initial amount advanced is less than £10m but future drawdowns may bring the value of the security above £10m in total, the Minimum Value Condition will only be met where any future amounts, bringing the overall amount advanced to £10m or more, are non-contingent. In other words, those drawdowns must be non-discretionary under the terms of the original documentation. Where the future amounts that may be drawn down are at the discretion of the debtor or creditor, they will be disregarded for the purposes of the Minimum Value Condition.

Creditor certificate

In addition to the conditions above:

a. the creditor and debtor must not be connected as defined in section 993, ITA 2007 (with the result that the QPP Exemption will not generally be available for intra-group debt arrangements); and

b. at the time of each interest payment, the debtor must hold a valid creditor certificate (Creditor Certificate) for each creditor stating that such creditor is:

(a) beneficially entitled to the interest payable to it on the relevant security (for genuine commercial reasons and not as part of a tax advantage scheme); and

(b) resident in a ‘qualifying territory’ (being, broadly, the UK or any jurisdiction with which the UK has a double taxation treaty containing a non-discrimination clause (see INTM412090), although note that there is no requirement for that treaty to reduce withholding tax on interest to nil).

The debtor

For the purposes of the QPP Exemption, the debtor is the company that stands in the position of debtor in respect of the relevant security. Where there is a chain of companies, the Guidance confirms that the debtor is the company that has borrowed the money on its own account (and not any intermediary company in the chain).

The QPP Exemption only applies where the debtor is a company so it would not be available where the debtor is, for example, a partnership or limited liability partnership.

The creditor

The creditor is the person who is beneficially entitled to the interest on the relevant security.

Where there are a number of intermediaries in a chain, it is necessary to consider who, ultimately, has the beneficial entitlement to the interest and the debtor must hold a Creditor Certificate in respect of that person. Where there is a chain of entities determining who is beneficially entitled to the payment may not be straightforward; the Guidance notes that the principles set out in the Court of Appeal decision in Indofood should be applied in making any such determination.

Where the creditor of record is an entity that is transparent for tax purposes, it will be necessary to ‘look through’ that transparent entity to determine who is beneficially entitled to the interest. For instance, this is likely to be relevant in the context of partnerships where it will likely be necessary to ‘look through’ the partnership to its partners.

Multiple creditors

In practice, a placement may be made up of more than one security. For an individual security to qualify for the QPP Exemption, the debtor needs a Creditor Certificate for each creditor in respect of that security, but not necessarily for each creditor participating in the placement as a whole (see example 4).

If the debtor holds Creditor Certificates from all creditors in relation to a particular security (and the other conditions are met), the QPP Exemption should apply on interest payments on that security even though the wider placement includes securities for which Creditor Certificates are not held (see example 5).

To reduce the administrative burden, the Regulations provide that the Creditor Certificate may be provided ‘by or on behalf of’ the creditor. As such, taking the example of a partnership, the Guidance confirms that the Creditor Certificate may be provided by a general partner on behalf of those partners in the partnership that benefit from the QPP Exemption.

Form of Creditor Certificate

There is no prescribed form of Creditor Certificate (although it must be in writing). This flexibility means that the parties are free to decide themselves how to document this. For instance, the Creditor Certificate may be provided in a standalone document or included as part of the transaction documentation.

Withdrawal and cancellation of Creditor Certificates

As soon as practicable after the creditor becomes aware that it no longer meets the relevant conditions, the creditor (or a person on its behalf) is required to notify the debtor of such and that the relevant Creditor Certificate is no longer valid. The debtor may want to put the creditor under an obligation to make such notification in the transaction documentation. In those circumstances, the relevant Creditor Certificate will no longer be valid on and from the day after the date on which notification is received by the debtor, at which point the security ceases to be a relevant security and the QPP Exemption will no longer be available (see example 6).

The Regulations allow HMRC to require the debtor to produce a Creditor Certificate within a specified period (normally 28 days). If the Creditor Certificate is not produced, or if HMRC has a reasonable belief that the Creditor Certificate is inaccurate, HMRC can determine that the Creditor Certificate should be cancelled. In those circumstances, subject to the availability of any other domestic exemption or relief under an EU directive or applicable double treaty, UK income tax must be deducted from any interest payment by the debtor on and from the date the debtor receives notification of the cancellation of the Creditor Certificate. A creditor may want to place the debtor under an obligation to notify it following cancellation of the certificate in the transaction documentation.

Final remarks

The QPP Exemption is an important complement to the existing exemptions from UK withholding tax on interest. The QPP Exemption should simplify the process for overseas lenders lending into the UK (in particular, by eliminating the administrative requirements associated with a claim for relief under a double taxation treaty) and so encourage debt investment into the UK.