The right route

Share this article

Stuart Pibworth provides guidance on warranties and covenants, and explains why it is important to be aware of the differences

Key Points

What is the issue?

For historic tax exposures, protection generally takes one of two forms: warranties and/or covenants. The scope and drafting of that protection will often turn on the tax due diligence undertaken and the relative bargaining strengths of the parties.

What does it mean to me?

In the heat of negotiations and the desire to ‘get the deal done’, sometimes the legal differences between, and effective protection provided by, warranties and covenants can be overlooked. Those differences were highlighted in the recent High Court decision in Oversea-Chinese Banking Corporation Ltd v ING Bank NV (the OCBC decision).

What can I take away?

Whether tax warranties offer sufficient protection for a purchaser on a share sale will depend on the circumstances. However, it is important that the differences between tax warranties and tax covenants, and the protection they provide, are understood and properly explained to both purchasers and sellers.

On share acquisitions, purchasers customarily seek protection in the share purchase agreement (SPA) for historic exposures (including tax exposures) of the company/group being acquired (target). For historic tax exposures, protection generally takes one of two forms: warranties and/or covenants. The scope and drafting of that protection will often turn on the tax due diligence undertaken and the relative bargaining strengths of the parties.

However, in the heat of negotiations and the desire to ‘get the deal done’, sometimes the legal differences between, and effective protection provided by, warranties and covenants can be overlooked. Those differences were highlighted in the recent High Court decision in Oversea-Chinese Banking Corporation Ltd v ING Bank NV (the OCBC decision).

Warranties

Warranties are statements of fact made by the sellers (or a subset of them) in the SPA or ancillary documentation regarding the position of the target as at the date of signing of the SPA (sometimes repeated at completion).

If it transpires that the warranty was incorrect, the seller will be in breach of contract and the purchaser will, prima facie, have a damages claim against the seller. However, to bring a claim against the seller the purchaser needs to demonstrate, broadly, that:

- it has suffered a reasonably foreseeable (and quantifiable) loss as a result of the breach;

- the seller had not disclosed the liability; and

- it has mitigated its loss.

Where the warranty has been breached (and the purchaser overcomes the hurdles outlined above), the purchaser is entitled to be put in the position it would have been in if the wrong (the breach) had not been committed and recover damages for the loss of bargain.

For breach of warranty on share sales, the longstanding principle is that the measure of damages is the difference between the true value of the shares and the value of the shares as warranted. In other words, what is the diminution of value of the shares arising from the breach of warranty?

Generally, a court could be expected to take the price paid for the target as evidence of the value of the shares as warranted. To show the impact of the breach on value, a comparison of that amount to the arm’s length amount that would have been paid had the true position been known is required. In turn, that requires expert input and consideration of the methodologies used by the purchaser in computing the purchase price for the shares.

Given these inherent complexities, the primary purpose of asking for tax warranties is often to gather information about the target, through the resulting disclosure exercise. If any exposures are identified, the purchaser could then look to obtain additional protection in respect of that liability through a tax covenant or, if the seller is not prepared to provide a tax covenant, a price reduction or seek insurance cover for the identified risk.

Tax covenant

A tax covenant is a contractual obligation on the seller to pay to the purchaser an amount equal to any tax-related liability within its scope. The tax covenant can either be general (covering all pre-completion tax liabilities of the target) or specific (covering certain identified historic tax exposures), and usually also includes protection against certain costs the purchaser may incur in bringing a claim.

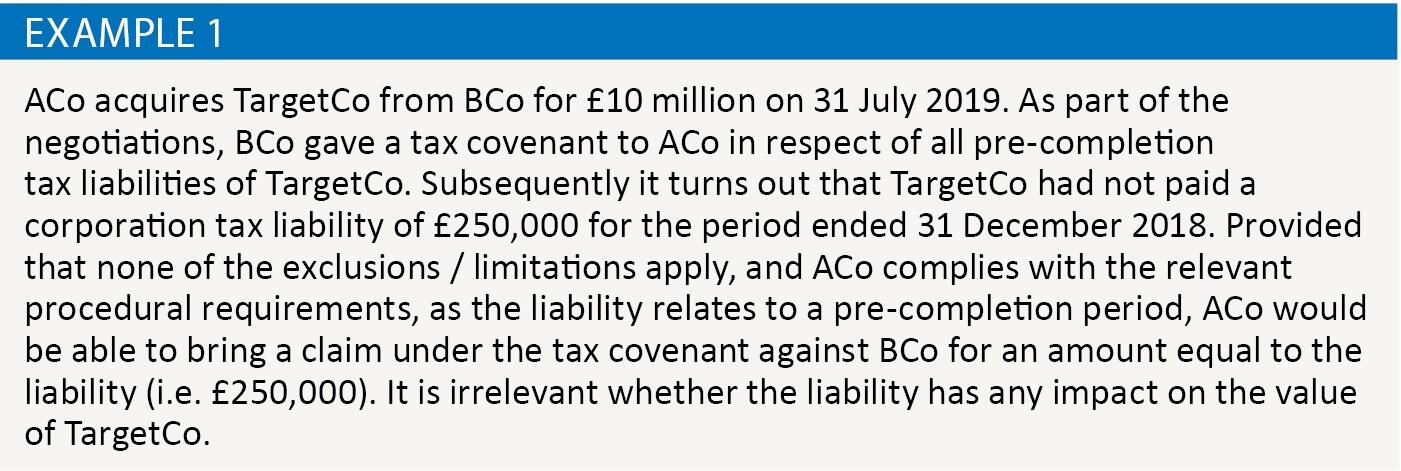

The key difference from a tax warranty is that the purchaser does not need to prove a loss in the general sense. Instead, provided that the liability falls within the scope of the covenant (and is not restricted by any contractual exclusions or limitations), the seller is required to pay to the buyer on a pound-for-pound basis an amount equal to the liability (see Example 1). It is irrelevant whether the liability has any impact on the value of shares. In other words, even if the value of the shares remains unchanged, the purchaser will still be able to claim against the seller.

Image

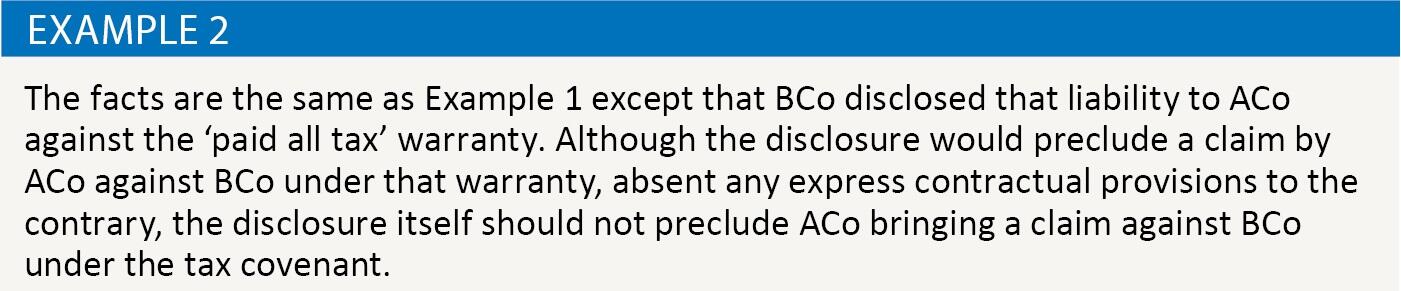

It is also irrelevant whether the purchaser:

- had knowledge of the liability or the liability was disclosed (see Example 2); or

- mitigated its loss.

Therefore, from a practical and evidentiary perspective, it is usually easier for a purchaser to bring a claim under a tax covenant than for breach of a tax warranty. However, sellers may resist giving a tax covenant on the basis that they want a ‘clean break’, rather than subject themselves to the sword of Damocles until the tax covenant expires (which is sometimes as much as seven years from sale, or longer). For certain sellers (such as private equity houses), it is simply not practical (and often impossible) to give these covenants.

OCBC decision

The OCBC decision concerned an alleged breach of warranty in a SPA. The facts are relatively straightforward:

- The purchaser agreed to purchase the target for USD$1.466bn.

- Under the SPA, the seller warranted that the target’s accounts for the period ended 31 December 2008 (the Accounts) gave a ‘true and fair’ view of the target as at that date (the Warranty).

- The purchaser alleged that the seller failed properly to record in the Accounts a liability in respect of certain equity derivative transactions amounting to USD$14.5 million (the Liability) and so breached the Warranty.

The purchaser argued that if there were no breach of the Warranty, the Accounts would have disclosed the Liability and the purchaser would have obtained an indemnity from the seller in respect of the Liability and so been able to recover USD$14.5 million from the seller under that indemnity. In advancing this position, the purchaser submitted that diminution in value is not the only measure of damages for breach of warranty in a share sale and sought to apply the principles relating to damages on sale of goods under the Sale of Goods Act 1979 by analogy to support its position.

The seller advanced the well-established principle described above that, in the case of a breach of warranty in a share sale, the purchaser is only entitled to recover the difference between the true value of the shares and the value of the shares as warranted (i.e. diminution in value).

In her judgment, Moulder J reiterated the well-established principle that, for breach of contract, the claimant is entitled to be put in the position that it would have been in if the wrong had not been committed and to recover damages for the loss of bargain. It was further noted that, in this case, no diminution in value of the shares was alleged by the purchaser resulting from the Liability.

Addressing the purchaser’s argument, Moulder J concluded that neither the authorities nor textbooks supported the purchaser’s position that the measure of damages for breach of warranty of quality on a share sale could be a hypothetical indemnity and the amount which could have been claimed under that hypothetical indemnity.

Moulder J went on to note that although it may be necessary to adjust the valuation methodology to determine the loss of bargain, neither the authorities nor the textbooks support an entirely different measure of damages for breach of warranty on a share sale other than the diminution of value of the asset (being the target).

On this basis, Moulder J rejected the purchaser’s argument.

Final remarks

Although the OCBC decision concerned an accounts warranty, the principle should equally apply to the measure of damages for breach of tax warranties. Whether tax warranties offer sufficient protection for a purchaser on a share sale will depend on the circumstances. However, it is important that the differences between tax warranties and tax covenants, and the protection they provide, are understood and properly explained to both purchasers and sellers.