Input tax challenges

Share this article

Neil Warren considers how much input tax can be claimed on some expenses where HMRC might argue that the cost partly or wholly relates to non-business or private use

Key Points

What is the issue?

Certain expenses incurred by a business might be considered by HMRC to be partly or wholly relevant to private or non-business purposes. The article considers how to make input tax judgments on some of these expenses, with references to HMRC guidance and past case law to assist the decision-making process.

What does it mean to me?

A split between business and non-business or private use of an expense can be carried out in any way that is fair and reasonable. In some cases, input tax can be wholly claimed on an expense but output tax might need to be paid on the onward supply of some goods or services to the beneficiary.

What can I take away?

A major challenge with claiming input tax is to always consider the ‘purpose’ of an expense, i.e. to ask if the business is spending its money wholly for business reasons or if there is actually a link to non-business motives. A business ‘benefit’ is not sufficient.

There are a number of expenses incurred by a business which can present a genuine input tax challenge for many advisers: can I claim all of the VAT being charged by the supplier, some of it or none at all? In this article, I will consider some of these tricky areas, and hopefully give a steer on the thinking to adopt in such cases, helped by HMRC guidance and past tribunal cases.

Employee perks and rewards

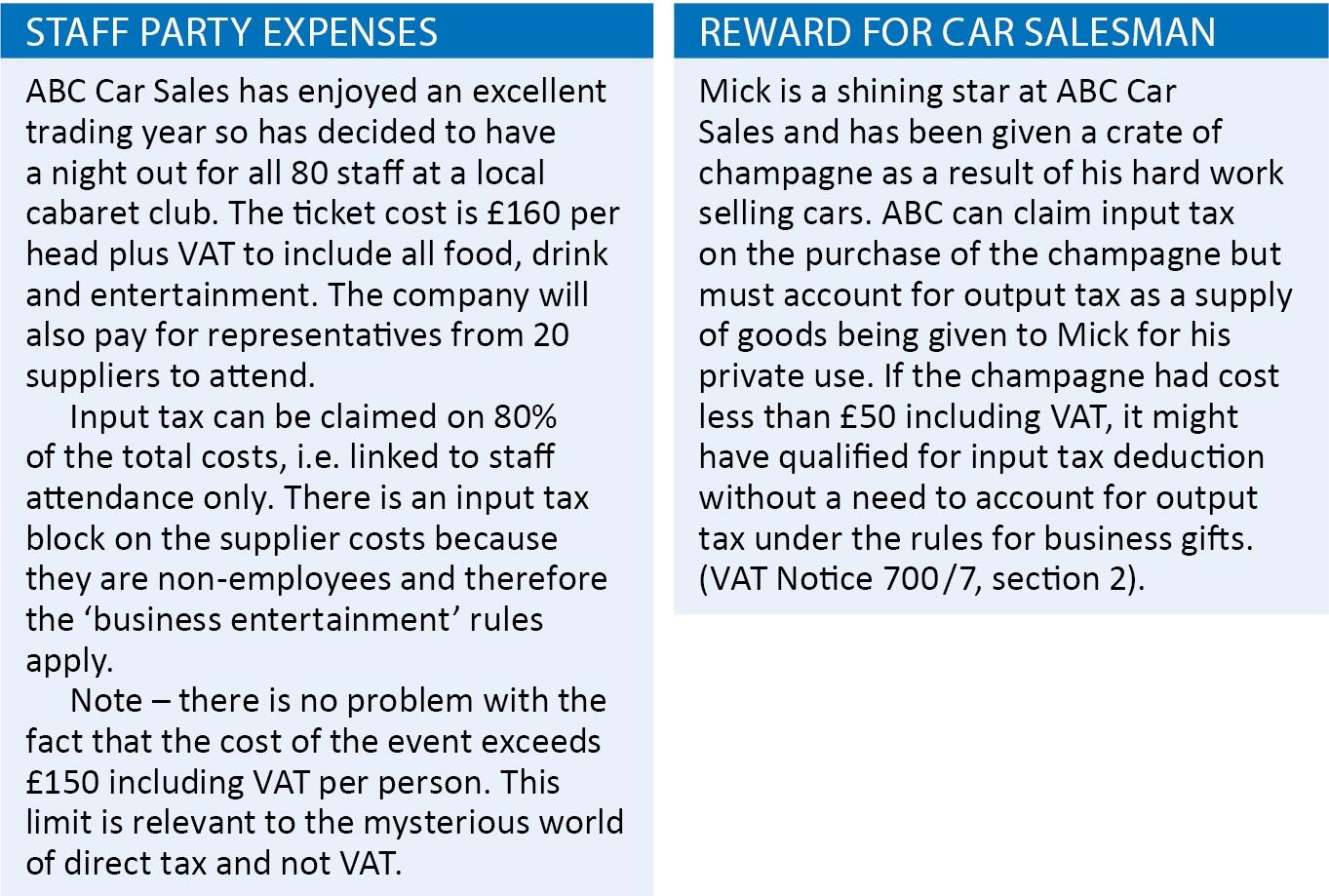

To quote the favourite catch phrase from the old TV programme The Two Ronnies, there is good and bad news here. Input tax can usually be claimed on goods or services bought by a business to reward staff because this is deemed to be a motivational expense designed to reward or encourage good performance. The business claiming input tax should obviously be fully taxable – restrictions linked to partial exemption need to be taken into account. But if the goods or services are allocated to a specific individual, rather than being for general staff use, then output tax will be payable to reflect private use by the employee (HMRC Input tax manual: VIT43700). This adjustment wipes out the input tax gain. See Reward for car salesman and Staff party expenses.

As a final comment, if a sporting or recreational facility is provided to all employees, e.g. the free use of a local gym which is paid for by the company under a corporate membership scheme, then input tax can be claimed by the company without any output tax being payable on the benefit provided. But there would be a problem if a specific employee was given free gym membership as part of his remuneration package. Output tax is now payable on the value of this facility provided to the individual, usually based on the cost price of the perk in question. (HMRC Input tax manual: VIT43950.)

Legal expenses

There is often a thin dividing line between legal fees that relate to the business, and those which are relevant to an individual director, employee or business owner. For example, legal fees might be incurred to defend an employee in a court case, and there is no doubt that an adverse result could impact on the trading reputation of the business. But as a general principle, input tax cannot usually be claimed on the costs of defending a criminal charge against an employee. To quote from HMRC input tax manual VIT13600: ‘Every case is unique and HMRC will need to think about all the details before reaching a conclusion.’

A well-quoted historical case that went in favour of the taxpayer many years ago related to P&O European Ferries (Dover) Ltd (VTD7846) where the tribunal ruled that input tax could be claimed when the company paid the legal costs of defending a charge of manslaughter against itself and seven employees following the Zeebrugge disaster: ‘The conviction of any of the employees would have caused severe damage to the public perception of the company’s business.’

But to balance the books, many other cases have been won by HMRC. Needless to say, HMRC tend to be quite strict in their interpretation of the ‘business purpose’ test which is crucial to any input tax claim. In reality, past case law has often given unpredictable outcomes, a bit like an inconsistent cricketer who gets one good score followed by a series of ducks. And in some cases, not even the judges can agree: in the case of Praesto Consulting UK Ltd [2017) UKUT 395, the Upper Tribunal supported HMRC’s decision to disallow input tax on costs linked to a legal case against an employee, which overturned an earlier decision in the First-Tier Tribunal. Enough said!

Mobile phones

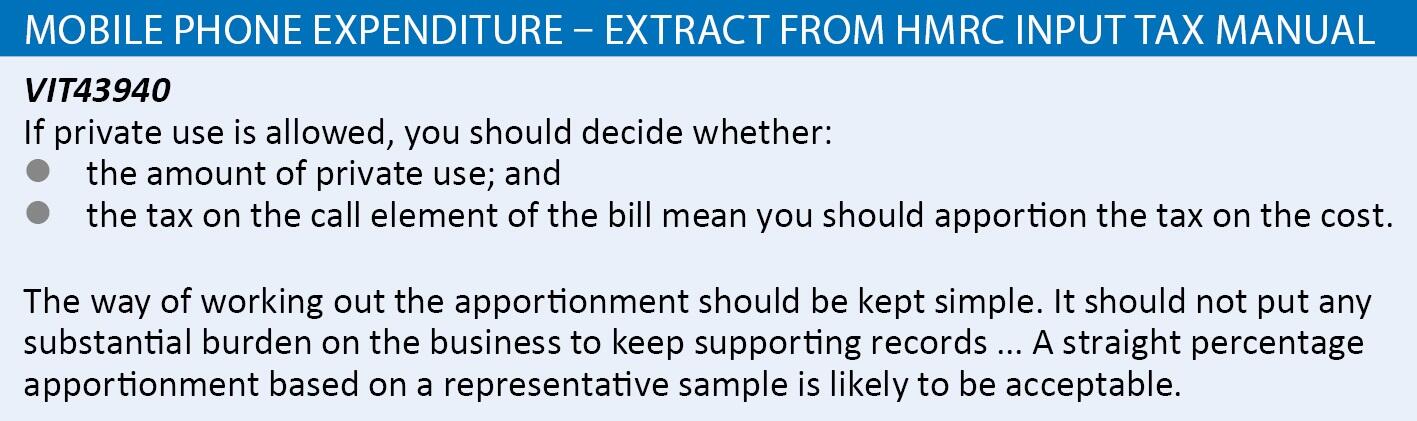

It is probably fair to say that most businesses claim all VAT incurred on mobile phone expenses they pay for, even if the phone is linked to an individual employee, and there is no company policy to restrict the employee from using the phone for his private calls and social media activities. In other situations, employers will have a policy which does not allow private use of the phone, and it is expected that the employee will have his own phone for personal use. But what is the correct VAT treatment?

The good news is that all input tax can be claimed on line rental costs (if appropriate) with no charge to output tax as long as the phone has some business use. But if the company’s policy does not prevent private use by the employee in question, then HMRC will expect an apportionment on call costs unless the private use is ‘incidental’ – see Mobile phone expenditure – extract from HMRC Input tax manual. If employees are charged for private calls through eg a salary deduction, then input tax can be fully claimed on the phone costs and output tax will be payable on the employee contributions.

Sponsorship

As you read the ‘sponsorship’ heading, you might be thinking of a common question asked by some clients, who have a personal interest in either motor racing, horse racing or boating activities: “My company has bought a racing car, which will have the company name and logo boldly printed on the side of the car. Can we claim input tax on the buying and running costs of the vehicle as an advertising expense?” asks an optimistic director.

The starting point is to remember that a business can claim input tax on any legitimate costs that promotes its business or provides facilities to all staff, e.g. the gym facility I referred to earlier. But the reality of spending on boats, cars and horses is that it is often linked to a private interest of the business owner or, in some cases, a relative. It all comes down to the question of whether the ‘purpose’ of the expense is to advertise the business or because it assists a personal hobby or activity of an individual. And there is a big difference between a ‘business benefit’ and a ‘business purpose’ – it is the latter phrase that is relevant for input tax purposes (VATA 1994 s 24).

Practical example

I recently dealt with a query from an accountant linked to the costs of a horse box. His client had claimed 100% input tax on the cost of the box, on the basis that it publicised the business website address and main trading activity on both sides, and it had a lot of exposure on motorways as the box was transported to and from various events throughout the year. It was even painted in the company’s favoured colours.

A determined HMRC officer initially sought to disallow all of the input tax on the basis that the expense was wholly linked to the director’s spouse and her participation in show jumping events. But then he relaxed his stance and agreed to allow a 20% claim to recognise a partial business purpose. I thought that 20% was very fair because it is unlikely that a business looking to maximise the return on its advertising budget would select a horse box. But the accountant I was advising genuinely thought that 50 /50 would be a fair apportionment. I don’t know whether his argument was successful but I suspect not and that he had to settle for 20%.

For useful case law about input tax and boat expenses, see Lai’s Ltd (TC 3352).