Keep it in the family: how to run a family office

Share this article

Family offices offer a tailored way for families to manage their assets and affairs, but success depends on careful structuring, funding and expert tax advice.

Key Points

What is the issue?

Family offices are becoming increasingly popular as wealthy families centralise the management of their financial, administrative and strategic affairs through dedicated structures, often with professional advisers at the core.

What does it mean for me?

The tax and regulatory implications of running a family office are complex – covering corporation tax, VAT, transfer pricing and global reporting obligations. Without proper planning, families risk double taxation, loss of VAT recovery, or non-compliance with transparency and regulatory rules.

What can I take away?

Families should seek early, coordinated legal and tax advice when setting up or restructuring a family office to ensure that funding, fees and governance frameworks are both compliant and tax-efficient. A tailored, well-advised approach can secure long-term wealth preservation, reduce administrative burden and maintain control across generations.

A ‘family office’ enables a family to outsource the management of its wealth holding structures, and other administrative or strategic functions, to a trusted group of advisors or individuals. Family offices principally exist to relieve family members of the burden of these responsibilities by centralising them within a carefully selected team.

Family offices can take many forms, depending on the size and complexity of the family, where the family is resident, the nature of the assets being managed and the range of services to be provided. Some family offices are dedicated to service a single family, while others operate as multiple family offices supporting several clients.

The structure can range from a single professional who is directly employed, to a larger family office company employing specialists across a range of disciplines – sometimes forming part of a wider family management and asset holding structure.

The benefits of family offices are numerous and include:

- the ability to consolidate family costs and achieve economies of scale;

- ensure continuity of vision across multiple generations of a family within a lasting framework;

- limit the liability for family members when structured as a company;

- maintain confidentiality and discretion amongst a select group of trusted individuals;

- provide flexibility and freedom outside the constraints and restrictions often imposed by larger institutions; and

- control and direct accountability.

Crucially, there will never be a ‘one-size-fits-all’ model for a family office. Each must be tailored to the family’s unique circumstances, priorities and long-term goals. For tax advisers, fully understanding these factors is essential to designing a bespoke and efficient structure that meets the family’s needs.

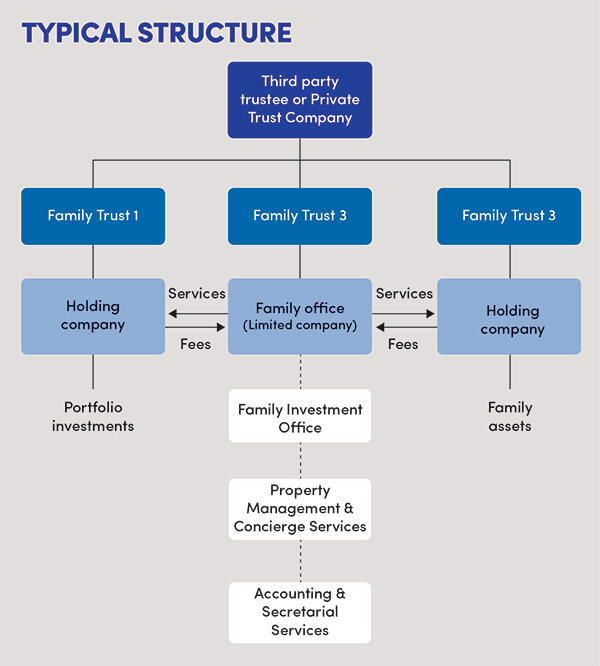

The structure of a family office

The structure of a family office should take into account the family’s specific needs, as well as its unique jurisdictional, tax and regulatory considerations.

A family office is often established as a limited company, with its shares held either by a family trust or directly by family members. However, alternative vehicles – such as partnerships – can also be appropriate, and in more complex cases the family office could sit within a wider network of companies or other vehicles.

The exact form of the vehicle would depend on its intended function, which is specific to each family. For instance, where the purpose is primarily to oversee asset-holding entities and manage the division of the underlying income and capital among family members, a partnership could be more appropriate. By contrast, if the family office employs staff and provides a range of services – such as investment management or concierge functions – a corporate structure is likely to be preferable.

Typically, the family office company or vehicle operates separately from any asset-holding entities, although these would normally form part of the same overall family group.

Directors are often family members, who may also be shareholders, while many families appoint independent professional directors. Using independent professionals can be more expensive, but it alleviates the administrative burden for family members, may help to navigate any family tensions and may be preferable from a confidentiality perspective – as directors’ details may appear on public registers such as Companies House.

Family offices may have a single office, or multiple offices across different jurisdictions. Multiple offices are more common where family members reside in different countries and prefer to be able to deal with a local family office hub. Opening an office abroad can also be helpful for immigration purposes, as some jurisdictions offer visas to individuals setting up family offices or businesses locally. Other reasons may include diversifying the family’s investments geographically, addressing local skills shortages or responding to changing political climates.

Services provided

The range of services provided by a family office can vary widely and tend to evolve with the family’s changing needs. At the most basic, a family office might provide personal assistant-type support to help with daily tasks such as managing communications, drafting emails, organising diaries and arranging travel and accommodation.

For families with more complex needs, a ‘full service’ family office can provide a comprehensive suite of services, including:

- concierge services, covering all aspects of personal and household logistics;

- non-personal asset management, such as overseeing investment portfolios and monitoring performance;

- oversight of family companies or trusts, ensuring compliance and alignment with family goals;

- family and corporate governance, including setting policies, succession planning frameworks and decision-making processes;

- wealth and succession planning, ensuring long-term preservation and transfer of wealth between generations;

- management of trophy assets, including high-value collections such as art, wine, jewellery, yachts, jets and cars;

- accounting and financial reporting, covering both family and business assets;

- financial administration, such as paying bills, managing liquidity and placing surplus funds on deposit; and

- philanthropy and charitable giving, including oversight of family foundations, trusts and donations.

Funding and management fee

A substantial injection of funds is usually required at the outset to help establish the family office. This funding is often provided as a capital contribution or, less commonly, a shareholder loan. Since most family office entities are not designed to be profit making, capital contributions tend to be the more practical approach.

Once up and running, the aim is for the family office to become self-funding by charging management fees for the services it provides. These fees may be charged either directly to family members or to their trusts and asset-holding vehicles, depending on the nature of the services rendered.

It will often be more tax-efficient to charge the management fee to asset-holding entities within the family structure rather than to individual family members. This approach can avoid VAT leakage (where those entities are VAT-registered) and allows expenses to be set off for tax purposes. However, if a family member is regularly dipping into the family office for personal services, that individual should be charged separately, rather than wrapping those costs up in fees charged to the wider family wealth structure.

If management fees are not charged for services provided, the value of those services can be regarded – at least in the UK – as a taxable benefit in kind. This could be the case, for instance, if family members sit on the board of a corporate family office, act as shadow directors or are beneficiaries of a shareholder trust.

In the UK, income tax on a benefit in kind can be charged at rates of up to 45%, so this is best avoided. To avoid such tax exposure, the management fee must at least cover the value of any third-party services procured by the family office and, arguably, include a margin to cover the cost of staff employed directly by the family office.

Other tax and compliance considerations

Family offices that operate as corporate entities are normally structured so as not to make a profit. This ensures that corporation tax – or its equivalent in the jurisdiction of incorporation – does not become payable. This is usually not problematic, as the management fee can be kept at an appropriate level. This is another reason for the family office and the family’s investment-holding entities being kept separate.

VAT

VAT treatment presents particular challenges for family offices due to the difficulty in defining their activities and determining whether these constitute taxable supplies. Where services are provided solely to family members without charge, HMRC may view these as non-business activities falling outside the scope of VAT. This would mean that the family office would not need to register for VAT but would also be unable to recover input VAT on its costs.

Conversely, if the family office charges fees to family members or related entities for services, these may constitute taxable supplies, potentially requiring VAT registration once the threshold is exceeded. VAT registration would enable recovery of input VAT on associated expenses.

Many investment management services are VAT-exempt, but this can be disadvantageous if it restricts recovery of input VAT on professional fees, office expenses and operating costs. The VAT position becomes more complex where the family office serves multiple family branches or unrelated parties. Advisers can assist by analysing the nature of services provided, determining the optimal structure from a VAT perspective, and ensuring that any VAT registration and reporting obligations are properly managed.

Transfer pricing

Transfer pricing issues arise when a family office and the investment entities it supports are under common control – for example, within an overarching trust structure. HMRC requires that all transactions between connected parties reflect arm’s length pricing. Where a family office charges management or advisory fees – or allocates costs – to family-controlled investment companies, these arrangements must be demonstrably consistent with what independent parties would agree in comparable circumstances.

Undercharging or providing services without appropriate remuneration can trigger transfer pricing adjustments and tax liabilities, whilst overcharging may be challenged as lacking commercial substance. Although some smaller family offices may fall within the SME exemption, this is less likely for international or multi-jurisdictional structures. Cross-border arrangements are particularly complex, as they fall within the scope of both UK transfer pricing rules and OECD guidelines. Coordinated advice and careful documentation are required to satisfy tax authorities in multiple jurisdictions.

Global reporting and transparency

In addition to the tax reporting obligations of family members, it is likely that entities within a family’s wealth structure will be subject to global information exchange regimes, such as the Common Reporting Standard (CRS), US FATCA and various beneficial ownership registers. Family members must understand what information is reportable and who it must be disclosed to. Maintaining full and accurate records is essential.

A centralised family office can make this much easier by managing the reporting obligations and record keeping in multiple jurisdictions, as well as being responsible for the privacy and tax profiles of family members.

Regulatory considerations

Family offices face an increasingly complex regulatory landscape. Whilst smaller family offices may fall outside the scope of Financial Conduct Authority (FCA) regulation if they limit activities to managing the family’s own wealth, boundaries can blur when services are extended to multiple family branches or accept external capital. Other key issues include AML compliance, data protection obligations under UK GDPR, and potential registration requirements if investment management services are provided. This is a complex area where expert advice is vital.

Role of tax advisors

Given the complex and evolving legislative and regulatory frameworks, experienced tax and legal advisers play a crucial role in supporting family offices. Their expertise is essential across multiple areas, whether advising on the establishment and funding of family offices, establishing appropriate governance structures, implementing robust compliance frameworks, reviewing regulatory obligations or advising on personal tax considerations for family members.

An effective family office will successfully combine support from external professionals with internal family decision making. Larger family offices may benefit from having trusted ‘in-house’ advisers to provide initial legal or tax advice. Some smaller family offices may have trusted professional advisers who provide more of a quasi-family office function where their internal resources are not as substantial.

In all cases, it is important to find the right balance: retaining sufficient in-house oversight and control over matters of key importance to the family while delegating specialist work to external experts who can provide independent, technical and up-to-date advice.

© Getty images