Lump sums

Share this article

Kelly Sizer discusses the taxation of state pension lump sums

Key Points

What is the issue?

The new state pension, available to those retiring from 6 April 2016, cannot be deferred in favour of a lump sum. It can only be deferred for an increased regular state pension after the period of deferral.

What does it mean to me?

Those who deferred their ‘old’ state pension, who reached state retirement age prior to 6 April 2016, still have the choice of receiving a lump sum plus their indexed regular pension or an increased regular pension.

What can I take away?

People who have deferred under the ‘old’ rules may now be claiming sums in the tens of thousands of pounds. Misunderstanding the tax rules on taking a lump sum can cost them dearly.

The problem of getting the tax position right when claiming deferred state pension lump sums is one that will eventually be retired to the history books. This is because those entitled to the new state pension, that is those reaching state pension age from 6 April 2016 onwards, no longer have the option to defer in favour of a lump sum – they may only take a higher regular state pension income when they cease to defer.

But for now, the complexity of the quirky manner in which state pension lump sums are taxed remains for those who deferred claiming the ‘old’ state pension. This, as the Low Incomes Tax Reform Group (LITRG) has seen from its (virtual) post bag, has been causing a great deal of angst for affected pensioners.

Large sums

The lump sums available to those who have been deferring claiming their state pension for a few years can be considerable – tens of thousands of pounds in many instances. The lump sum is worked out as the state pension not claimed (including any uprating that the individual would have been entitled to), plus ‘interest’ at 2% over the base rate.

It might occur to readers that the ‘interest’ element of the lump sum might qualify in itself for the savings nil rate and/or starting rate for savings. However, while GOV.UK describes it as interest, I use the same term in inverted commas, as the legislation itself (Pensions Act 2004 Schedule 11) does not describe it as such.

If one considers that the alternative is to take a higher weekly state pension (increased by 1% for every five complete weeks of deferral under the ‘old’ rules, or 10.4% a year), it is much more likely that the 2% plus base rate ‘interest’ increment to the lump sum was not intended to be taxed as such. And indeed, Parliament then laid down special tax rules applicable to the lump sum, which do not provide for the ‘interest’ element to be stripped out and taxed as savings income.

Rate of tax

The rate of tax applicable to state pension lump sums is dependent on the amount of the taxpayer’s other taxable income, and the tax bracket into which they fall. For this purpose, the special rates of tax applicable to savings income (the starting rate for savings and the savings nil rate, or personal savings allowance) and dividend income (or dividend allowance) are ignored.

As explained by Robin Williamson in his article ‘Curiouser and Curiouser’ in August’s Tax Adviser, F(2)A 2005, sections 7–9 provide quite simply that the lump sum is treated as income but is not counted when determining the total income of any person. So if a person’s income apart from the pension lump sum (‘other income’) is totally covered by their personal allowances, the pension lump sum is taxed at a nil rate. If their other income less allowances is below the basic rate limit, the pension lump sum is taxed at the basic rate, at the higher rate if other income is between the basic rate limit and the higher rate limit, and at the additional rate if other income exceeds the higher rate limit.

Note that ‘income’ is determined by reference to Step 3 of the income tax calculation per ITA 2007 s 23. There is therefore no adjustment for Gift Aid or pension contributions as there is, for example, in the calculation of adjusted net income in ITA 2007 s 58.

For Scottish taxpayers, the rate is determined by the Scottish income tax bands.

Marriage allowance – a trap?

The marriage allowance given under ITA 2007 chapter 3A Part 3, seems to create a potential problem in respect of the tax rate applicable to the lump sum. Step 3 of the income tax calculation, from which the lump sum tax rate is determined, is income after deducting allowances to which the person is entitled under ITA 2007 chapter 2 Part 3 (the personal allowance and blind person’s allowance).

The effect of an election for the marriage allowance by the transferring spouse is to reduce their personal allowance by 10%. The conclusion is, therefore, that it is the reduced personal allowance that comes into play in determining the state pension lump sum tax rate, given that there has been no provision amending F(2)A 2005 to disregard any marriage allowance election. Those making such an election to give up 10% of their personal allowance and claiming a state pension lump sum should therefore take great care that it does not mean they trigger a tax charge on the lump sum which could by far outweigh the tax reduction offered by the marriage allowance!

Readers will, however, appreciate that the recipient spouse under a marriage allowance election does not receive an enhanced personal allowance. Instead, they get a tax reduction at step 6 of the ITA 2007 s 23 calculation. It therefore follows that a spouse in receipt of a tax reduction from a marriage allowance election who also claims a state pension lump sum cannot claim that, by virtue of their own personal allowance plus marriage allowance, they have nil taxable income and therefore nil tax liability on the lump sum. That is to say that the marriage allowance has no effect on the calculation of the tax liability on a state pension lump sum for the recipient spouse.

The marriage allowance might therefore create a lose-lose situation if an election had been made and both spouses were then to claim a state pension lump sum!

‘Tax election’

The state pension lump sum is taxable in the year in which the person is entitled to it, i.e. when the lump sum option is chosen on ceasing to defer. This is irrespective of when it is actually paid. If, say, a person stopped deferring and chose a lump sum on 1 April but that lump sum was not in fact paid until early in the new tax year, the tax point nevertheless would be 1 April.

This is unless a ‘tax election’ is made at the same time as choosing the lump sum (at the time of claiming the deferred state pension), or within a month of that day (Reg 21A(3) SI 1987/1968). This election allows the pensioner to opt for the lump sum to be paid early in the next tax year and also to be taxed in that later year.

Timing is critical

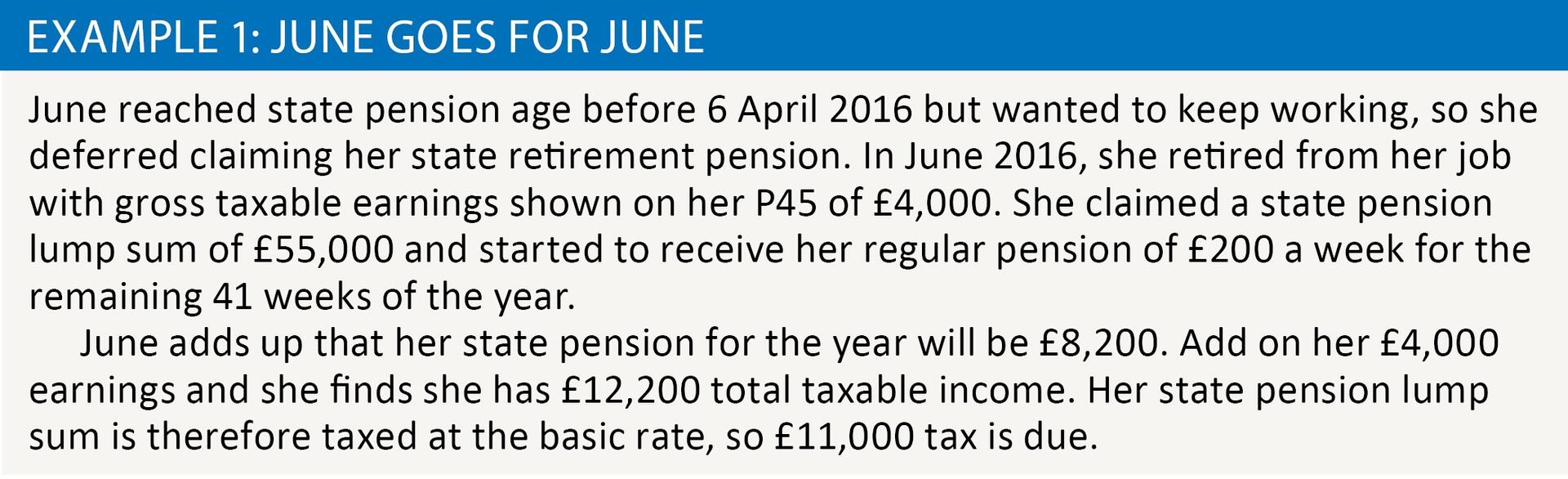

Hopefully prospective pensioners who are well advised by a tax professional would appreciate the importance of carefully timing a claim to a deferred state pension in order to get the best result for tax purposes. The following example, based on an enquiry to the LITRG website, illustrates the dangers of getting it wrong. See example 1.

If June had consulted a tax adviser at the time, no doubt she would have been told to make a ‘tax election’ to the DWP so that, while drawing her regular state pension income, she could have waited for the lump sum to be paid in April 2017. Her indexed weekly state pension, being her only income, would then have fallen within her 2017/18 personal allowance of £11,500 and she would not have been subject to income tax on the lump sum. Without that advice, June made an extremely expensive mistake.

Unfortunately, there does not appear to be any provision for a late ‘tax election’ to be made. Reg 21A of The Social Security (Claims and Payments) Regulations 1987 (SI 1987/1968) is clear that you only have a month to make the ‘tax election’. It would therefore seem that LITRG’s enquirer’s only recourse would have been judicial review if she could prove a failing in the process – but that is beyond the reach of most ordinary taxpayers and strict time limits apply.

In the absence of being able to file a late election, it might be that the taxpayer could consider making a complaint. This might involve one or both of the Department for Work and Pensions (DWP) and HM Revenue & Customs (HMRC), given the unusual relationship here of the two departments – i.e. the ‘tax election’ in fact has to be submitted to the DWP rather than HMRC as one would expect. Perhaps, for example, the individual did not receive details of being able to make a ‘tax election’ and could complain that they paid too much tax as a result? Alternatively, they might be able to prove that they were given incorrect or misleading information from either department before they took the lump sum.

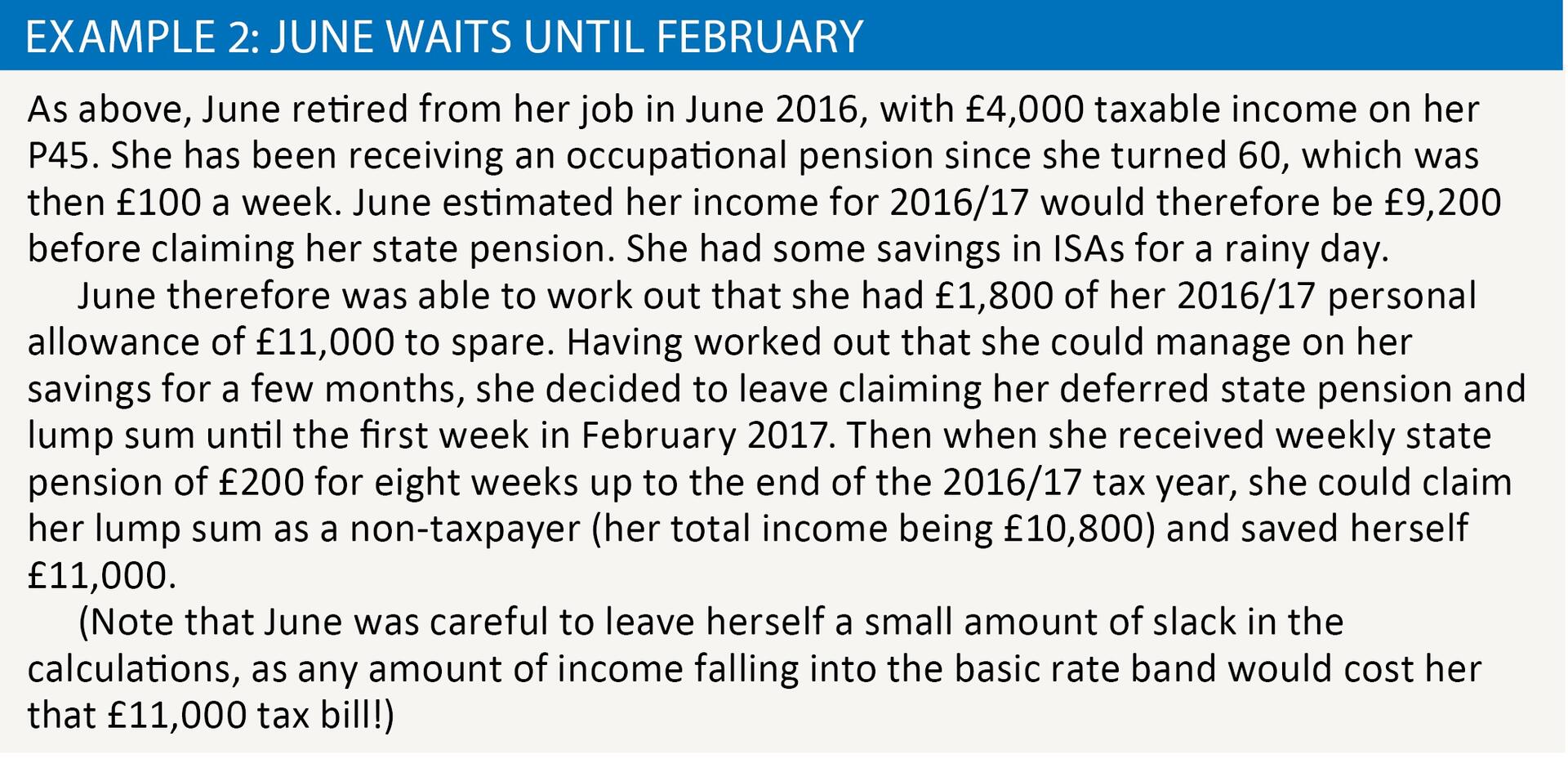

Tax election aside, however, let’s consider what else our enquirer may have done. Let’s say that June in our example above had another small pension which, together with her state pension, would give her total weekly income of £300.

In that situation, the tax election would have been no good to June, as her 2017/18 income with the two regular pensions together would amount to over £15,000 and she would still be taxable on the lump sum at the basic rate. But a bit of careful planning in the year of taking the lump sum might still have saved her an £11,000 tax bill. See example 2.

A word of warning

Readers will be aware of the need to avoid straying into giving advice that is regulated by the Financial Conduct Authority. Their website confirms that advising on the state pension itself is not regulated. However in the second example above of June waiting to take her state pension until later in the tax year and meanwhile drawing on savings, we can easily see how non-regulated advice might cross paths with regulated – especially if, for example, June’s ISA savings were held in investments other than cash.

Considering the tax position on, and timing of a claim to, deferred state pensions might also closely interact with planning under pensions freedoms (available for defined contribution pension savings since 6 April 2015). One can easily see how, for example, someone might:

- stop working on 5 April 2018 with earnings of say £40,000 in the 2017/18 tax year;

- then claim a deferred state pension lump sum of £60,000 in the 2018/19 tax year (at a time when the weekly state pension received will keep them within their personal allowance);

- and then in 2019/20, supplement their state pension income by starting to draw down on pension savings.

A person in the above situation might also access a tax-free lump sum from a pension in the 2018/19 tax year, as that obviously would not be included in the calculation of the tax rate on the state pension lump sum. But they would not wish to start drawing down any taxable element of the pot.

Any such planning would therefore need to be done in conjunction with an authorised and regulated adviser.

And finally

This article started off by saying that you cannot get a lump sum payment by deferring a claim to the new state pension (those reaching state pension age from 6 April 2016) – you can only get a higher regular pension. While that is true, you could end up with a lump sum from claiming the new state pension if you backdate your claim.

You can backdate a claim to the new state pension for up to 12 months. A backdated payment does not earn interest and is simply a payment of the amount you would have received, going back to the date of the claim. It does not qualify for any ‘special’ tax rules as with the old deferred state pension lump sums described above. Under Part 9, Chapter 5 ITEPA 2003, it therefore follows that the pension income is the amount accruing, irrespective of when it is paid.

A prospective claimant of the new state pension cannot therefore delay a claim to it, obtain a lump sum under the backdating rules and then expect that lump sum to be taxed in a later year. Though of course they may defer a claim to the pension and any higher weekly amount due when eventually claimed would be taxable in the year of claim onwards.

Guidance from the CIOT/ATT Professional Standards Team

As mentioned in the article, members will need to proceed with caution when offering advice to clients on this particular area, so as not to accidentally stray into the realms of providing unauthorised financial advice as it is a criminal offence to give investment advice if you are not authorised to do so by the FCA. Further details can be found on the FCA website.

Furthermore, in line with the guidance set out in our Professional Rules and Practice Guidelines, members must not undertake professional work which they are not competent to perform. As with all services provided members should ensure that the work to be undertaken is fully and accurately covered by both their engagement letter and Professional Indemnity Insurance.