Money on trees

Share this article

Richard Davidson examines the benefits of investing in UK woodland

Key Points

What is the issue?

UK commercial forestry is emerging as a mainstream alternative asset class.

What does it mean to me?

Investing in forestry can provide superior risk adjusted returns, tax free income from timber sales and is not liable for CGT on the increase in value of the standing timber, and there is no inheritance tax after two years of ownership.

What can I take away?

In a low or zero interest rate environment, forestry provides investors with an investment in a sustainable real asset with strong ESG credentials. Forecast returns of 10.0% per annum that are uncorrelated with equities and bonds.

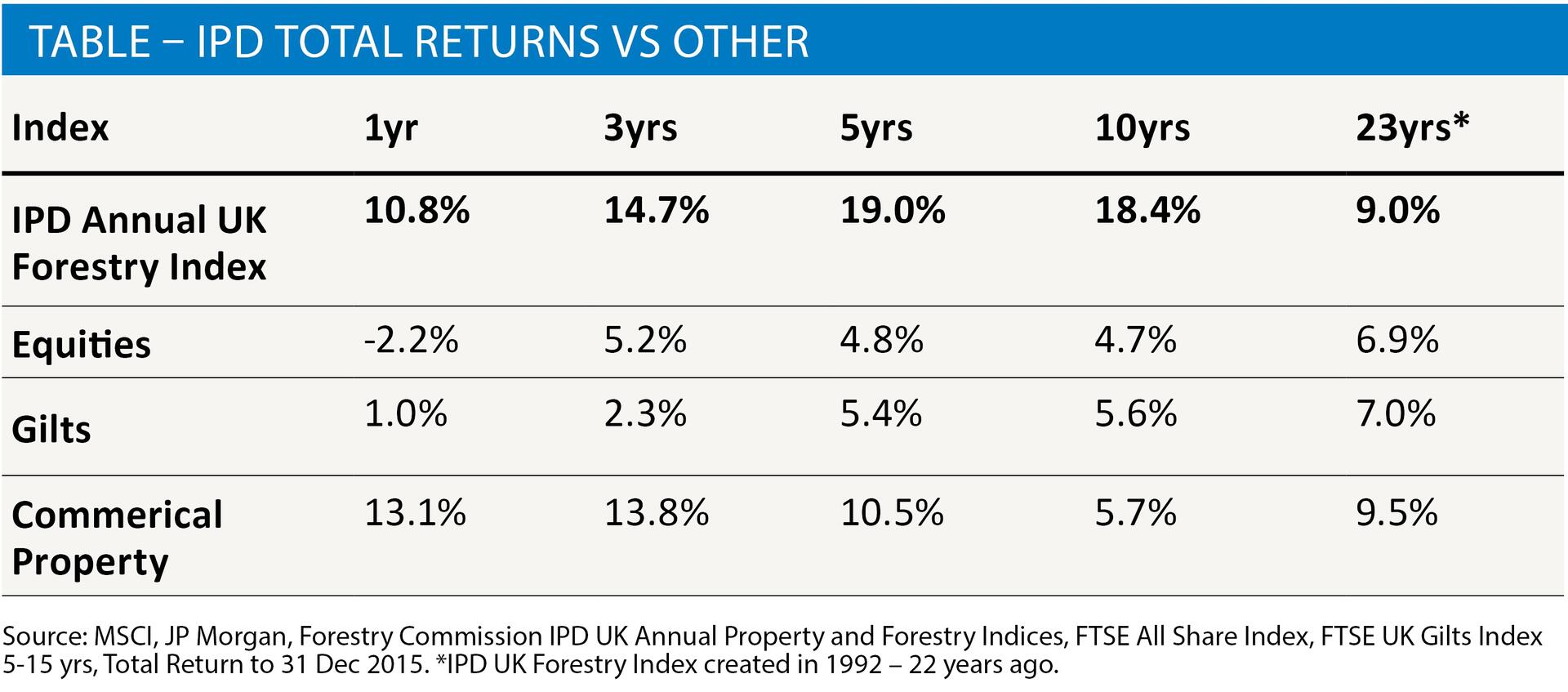

The investment returns for those who have invested in UK woodland have been handsome for some time now. Once considered a niche investment market, UK forestry has emerged from the shadows into the mainstream investment landscape as commercial forestry’s unique return characteristics have caught the attention of fund managers attempting to generate superior risk adjusted performance. Over the last ten years to 31st December 2015, UK commercial forestry, as measured by the IPD Forestry Index (a sample of 133 commercial forests in Britain), has been one of the most fruitful asset classes, generating annualised returns of 18.4%, with no years of negative returns. See table 1. It has outperformed all other traditional and alternative asset classes. Furthermore, these returns have been achieved with an annual standard deviation of less than 10%. Unsurprisingly, this kind of performance has piqued the interest of both institutional and private investors. See figure 1.

Image

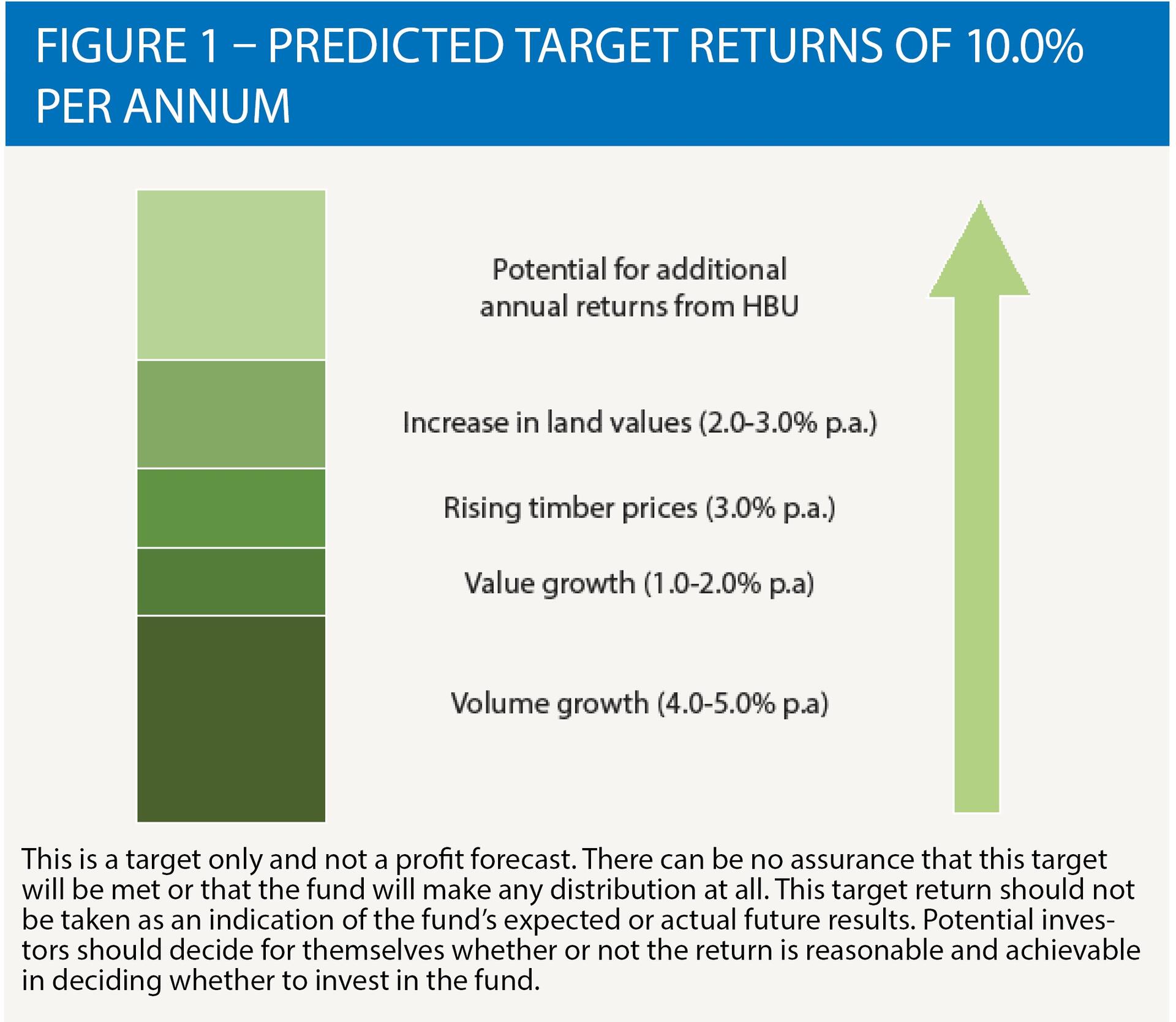

Target returns of 10.0% per annum

Although returns achieved from UK commercial forestry over the last decade are unlikely to be repeated over the next ten years, we expect long term annual nominal returns of circa 10.0% based on predictable volume and value growth of the trees and anticipated modest appreciation in timber prices and land values. This positive outlook is shared by GMO who forecast that timber will outperform international large cap equities by 3.2% per annum in real terms over the next seven years. Forestry also provides the added benefits of being lowly correlated to stocks and bonds, positively linked to inflation and produces an annual cash flow yield of 2.0% – 4.0% from harvesting timber. This compares favourably with the current 10-year gilt yield (0.8%) and the FTSE All-share dividend yield (2.9%).

Forestry has benefited from the growth in popularity of multi asset investments, which has seen pension funds, endowments and private clients reduce their asset allocation to more conventional equities and bonds in favour of alternative investments such as property, private equity, hedge funds and infrastructure. Amid the ongoing low-interest rate environment and volatile markets, it is no surprise that an increasing number of private individuals and institutional investors are attracted by the stable returns UK forestry offers. It is a trend that is following the US where commercial forestry, or timber as it is more commonly known, is a significantly larger and more mature market. The top 30 US Timber Investment Management Organisations (TIMOs) oversee approximately US$ 57bn of timber assets.

Performance of the asset class has been driven by a combination of factors including: the biological growth of the trees, the rising timber price, the increase in land values and the Higher and Better Usage (HBU) of land as an alternative energy source. As a medium to long term investment, forestry is generally low risk as it is underpinned by unique return drivers that are its strength: Trees grow regardless of what GDP or the stock or bond markets are doing, and the volume of the timber that is standing in the forest available for sale will increase every year. On a UK commercial softwood 35–40 year cycle this equates to a 4.0–5.0% annual volume growth rate. Not only is that more volume but the percentage of the tree in the more valuable large diameter cuts increases too as the tree expands. The rise of alternative energy projects have also contributed to returns, with solar panels, hydro-electric schemes and wind turbines all providing an alternative use for land.

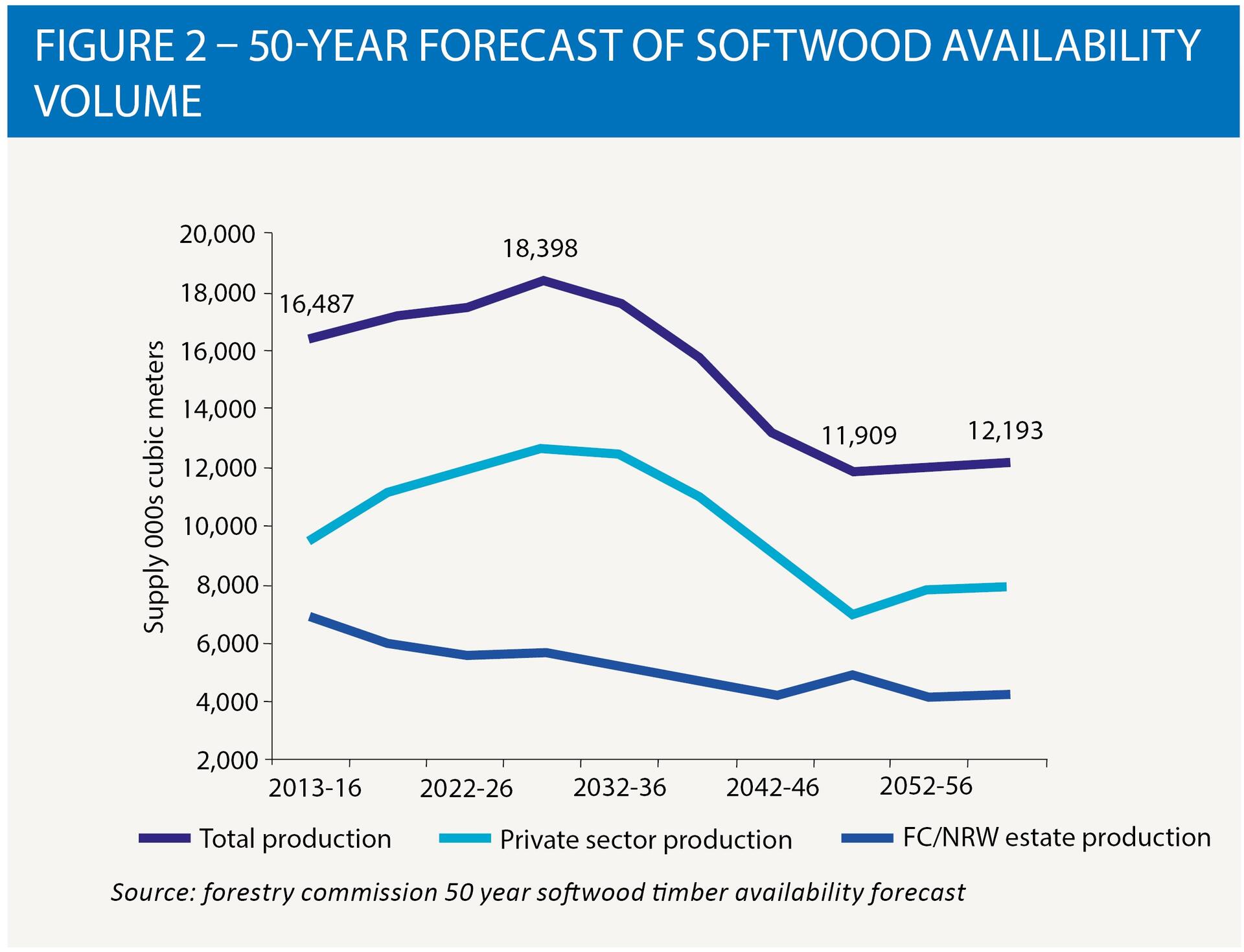

Looking beyond the next decade, the supply demand dynamic for UK timber is also strong. See figure 2. The UK still imports over 60% of the timber that the country uses, fluctuating with FX rates. We also expect the fallout from the UK’s decision to leave the EU to benefit UK timber as the pound weakens, leaving domestically produced timber more attractive to UK sawmills and timber yards. A shortfall in tree planting in the UK during the early 1990’s will create a shortage of timber supply from 2030 onwards. This coincides with the growing timber component within housing, the need for carbon neutral building materials and demand for biomass.

Forestry Commission timber availability forecast

UK forestry returns are further enhanced by the compelling tax benefits for UK investors. Once a commercial forest, or share in one, has been owned for two years it qualifies for 100% Business Property Relief, and as such is not subject to inheritance tax. Furthermore, the increase in value of timber is not affected by capital gains tax and income derived from the revenue generated by cutting down and selling the trees is free from income tax. The tax benefits surrounding UK commercial forestry are summarised as follows:

- Tax free income: Proceeds from UK timber sales are tax-free whether the asset is held personally or by a company

- Tax free capital gains: Increase in value of standing timber is exempt from capital gains tax (excluding increase in underlying land values)

- Capital gains roll-over: Proceeds from the sale of capital assets can be reinvested in UK commercial forestry land to defer the capital gains

- No Inheritance tax: Qualifies for Business Property Relief after two years of ownership

The historic returns, environmental, social and governance (ESG) credentials and tax incentives have not gone unnoticed by some significant institutional investors. Pension funds and endowments especially have been reaping the rewards. For example, two years ago Essex County Council invested £60 million of its pension fund into global forestry. Forestry investments offer numerous benefits to society:

- Carbon sequestration – Forests of Sitka spruce absorb 161 tonnes of Carbon per hectare

- Improving air quality – Trees absorb, transport and decompose many air pollutants

- Providing outdoor recreation – 417 million recreational visits were made to forests in England in 2014 (Forestry Commission)

- Supporting biodiversity – Forests provide sheltered habitats for wildlife, often supporting endangered species

- Regulating water supply & quality – Forests nurture the soils that are key to water retention, filtering & quality

- Produces renewable and energy efficient construction materials – As forests are harvested, the trees are replanted to begin the next forest cycle. Timber also has a much smaller carbon footprint than other materials such as steel and iron

Based on recent performance and future expectations the market for investment in UK forestry looks rosy. This will be driven by an increasing demand for timber amid a predicted fall in supply. At the same time timber is a carbon neutral product and will therefore have increasing share of construction demand. Ultimately UK forestry provides investors with a stable, sustainable real asset that grows in volume terms; as well as generating an annual cash flow yield of up to 4.0% it offers prospects of real capital growth, inflation protection and significant tax benefits.