More back and forth

Share this article

Edd Thompson considers the impact of the recent judgment from the Court of Appeal in Wakefield College on the concept of ‘business activity’

Key Points

What is the issue?

One of the fundamental pillars of VAT is the concept of ‘business’. Whether an activity is carried out by way of business can have radical implications for the VAT positions of the parties involved.

What does it mean to me?

Recent developments now give some reason to believe that we need to step back again from the business test many thought we had to follow after the Longridge upon the Thames case, and instead carry out a more fact-sensitive and wide-ranging enquiry.

What can I take away?

At the time of writing, HMRC has yet to comment publicly on the Wakefield decision. However, it certainly looks like we are back to some sort of multifactorial approach to determining whether an activity is a business activity, just not one that draws on a structured list of factors as in Lord Fisher.

Getting down to business

One of the fundamental pillars of VAT is the concept of ‘business’. Whether an activity is carried out by way of business can have radical implications for the VAT positions of the parties involved. The only problem is we don’t really know what it means.

Why does it matter?

At the start of any introductory VAT course you’re likely to learn that one of the conditions for a transaction to be within the scope of VAT is that it must be carried out ‘in the course or furtherance of business’. This is why, for example, you don’t need to consider VAT when you casually sell unwanted possessions on eBay as a one-off; you may be providing something to someone and getting money in return, but it doesn’t have the characteristics of a business-type activity.

This can be good news. Non-business activities can’t leave you with a requirement to register and account for VAT. However, they don’t give you the entitlement to register and recover VAT on costs that you get if the activity is by way of a (taxable) business. This trade-off is often at the heart of why the concept of business is so important in VAT.

The net effect of the trade-off will depend on the circumstances. Sometimes it may be desirable for an activity to be a business – think about a situation where there’s lots of VAT on the costs and the customer can recover any VAT charged on its purchase. Sometimes the opposite will be true – imagine there is very little VAT on the costs and the ‘customer’ can’t recover any VAT. But hopefully it should be apparent that the distinction can, and often does, result in radically different VAT costs along the chain of transactions.

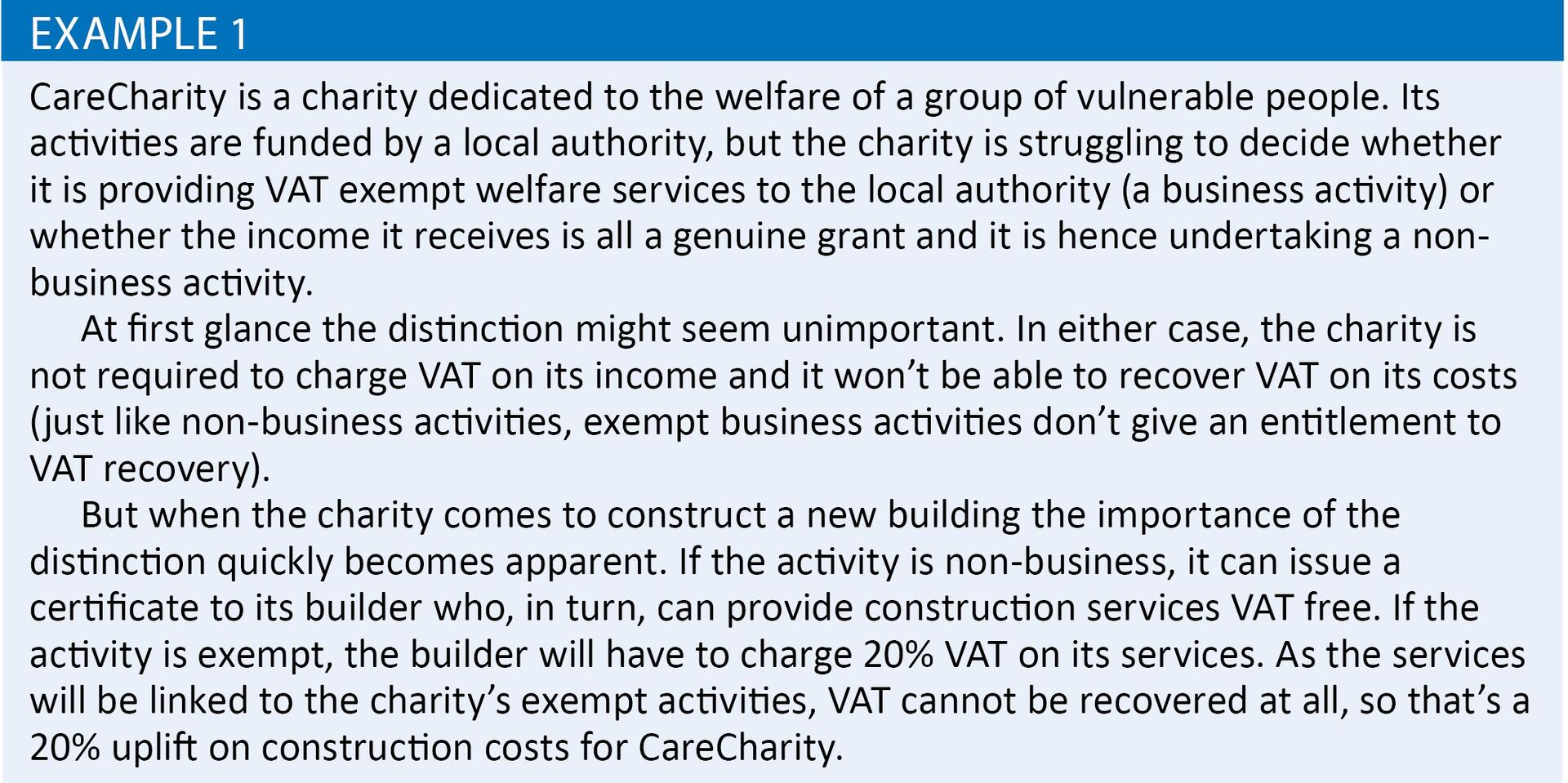

If that wasn’t enough, the concept of business can also have a crucial impact on the VAT reliefs available on purchases. This is vital in the charity sector where a key relief is the zero-rating for construction services, which can allow charities to benefit from VAT free building costs. A condition of the relief is that the building is to be used for the charity’s non-business purposes. The costs at stake can be very material indeed, as example 1 illustrates.

It’s clearly fundamental to be able to determine whether an activity is a business or not. Consequently, the significant confusion over the meaning of business is a worrying state of affairs.

The ‘traditional’ approach

Back in the day – by which I mean before 2016 – there’s a good chance that if you were learning about the concept of business you would have focused on the ‘business test’ set out in the case of Lord Fisher [1981] STC 238. Although I won’t revisit the facts of the case, suffice to say that it essentially set out a list of six hugely influential factors that needed to be considered when establishing if an activity qualifies as a business for VAT.

No single one of the ‘business test’ factors in Lord Fisher was determinative of whether an activity was a business. Instead you needed to look at the circumstances of an activity as a whole, using the factors outlined by the Court as a guide to arrive at a reasoned view as to its status.

Many other relevant cases continued to arise on the subject of business activities, but they broadly continued to be influenced by a similar multifactorial approach.

A major shift

Then in 2016 came the Court of Appeal’s judgment in Longridge on the Thames [2016] EWCA Civ 930. Longridge was a charity that ran outdoor activities such as rowing, sailing and kayaking, primarily for young people. It charged for the activities but the charge was low and it was flexed to the ability of people to pay. Because of this model, Longridge didn’t believe it was in business for VAT.

Just like CareCharity in example 1, Longridge was constructing a new building. It believed that its building costs should benefit from the VAT relief for non-business buildings and so be VAT free. HMRC disagreed, instead arguing that by charging for the activities Longridge had a business activity.

The Court of Appeal looked to Europe for guidance because the UK’s concept of business had to be interpreted in line with the concept of ‘economic activity’ in European VAT law. Drawing on European cases, it decided that the test was in many ways simpler than the Lord Fisher business test might suggest.

Broadly, if a payment could be linked directly to something provided in return and it took place on a continuous basis then it was a business activity. Longridge was therefore in business and could not benefit from the VAT relief on its building costs. Notably, the fact that it wasn’t trying to make a profit appeared to be largely irrelevant.

Many in the VAT community saw this as a real shift away from the decisions in many previous UK cases. It looked like the multifactorial approach to evaluating business activities might be dead and that a whole lot more activities than we thought might really be business activities.

A step back?

Recent developments now give some reason to believe that we need to step back again from the simpler test many thought Longridge meant we had to follow. In May of this year the Court of Appeal looked at the topic again in Wakefield College [2018] EWCA Civ 952.

Wakefield college was a further education college which offered courses to students. The students had to pay, but fees were heavily subsidised. The college felt that this was a non-business activity but HMRC disagreed and saw it as an exempt business activity. Once again, the dispute kicked off because of a building that the college thought it should be able to build VAT-free.

The college lost its appeal but the way the Court thought about the issues was different to Longridge. Whilst the Court agreed that a payment needed to be directly linked to something provided in return to be in the scope of VAT, the link on its own wasn’t enough to establish a business activity. On top of this you need to look whether the activity was done ‘for remuneration’.

In this context, ‘for remuneration’ had its own VAT meaning which required a ‘wide-ranging’ and ‘fact-sensitive’ enquiry. In the Court’s view, there was ‘no checklist of factors to work through’. In other words, you couldn’t appeal to a generic set of factors (of the sort found in Lord Fisher) to determine if an activity was a business, you had to look at each case on its merits.

Looking at the specific facts of Wakefield’s case, the Court thought the following facts pointed towards a business activity:

- the provision of education courses was the sole activity of the college

- providing courses to subsidised students was a significant part of what the college did

- the fee income paid by subsided students was significant

- the fee income paid by subsidised students made a significant contribution to the cost of providing the courses

- the level of fees varied depending on the cost of the course (even if it did not cover the cost in full)

- fees were not fixed by reference to means

- the viability of further education in general was underpinned by a mixture of grant aid and fees

However, what the Court called ‘subjective’ factors, such as whether the college was aiming to make a profit were not relevant to its decision.

It is worth noting that the Wakefield decision was heavily influenced by a European case called Borsele (C-520/14) which examined whether a Dutch local authority providing school transport in return for a small parental contribution had a business activity. The European Court (CJEU) in Borsele appeared to advocate the kind of two-stage test used in Wakefield and arrived at the conclusion that the transport wasn’t provided for remuneration.

Where are we now?

At the time of writing, HMRC has yet to comment publicly on the Wakefield decision. However, it certainly looks like we are back to some sort of multifactorial approach to determining whether an activity is a business activity, just not one that draws on a structured list of factors as in Lord Fisher.

We may understandably be left more than a little confused by all the back and forth. The court decisions give tax advisers something to work with but it seems there are still multiple shades of grey when advising whether an activity is a business. Moreover, the suggestion in Wakefield that we need to make ‘wide ranging’ and ‘fact sensitive’ enquiries seems, regrettably, to invite disagreement and uncertainty.

Of course, there is no easy answer to the dilemma, but I can’t help but feel sorry for those charities wondering if they need to register for VAT or perhaps whether they can get their building costs free of VAT, often having to settle for the answer that it’s a bit of (educated) guesswork.