This is not a drill!

Share this article

Alan Powell explains the wide-ranging impact of new HMRC controls for alcohol wholesalers and retailers

Key Points

What is the issue?

Under new law, HMRC will have to approve as wholesalers most business-to-business vendors of duty-paid alcohol. Trading wholesale in this context means trading in any quantity of alcohol. Further, many businesses affected by the new scheme would not be classified as ‘traditional’ wholesalers, or even consider their trade to be wholesale. Retailers will have to check that HMRC have approved their suppliers

What does it mean to me?

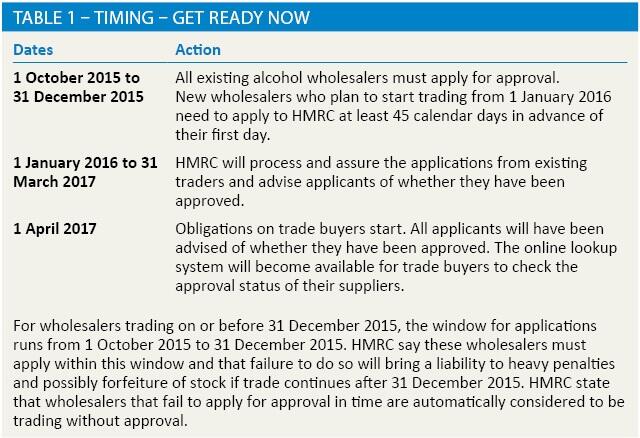

HMRC will start to register existing wholesalers between 1 October and 31 December 2015. ‘Trade buyers’ (including retailers) will only be able to buy legally from approved wholesalers when the scheme takes full effect from 1 April 2017 (see Table 1)

What can I take away?

Businesses selling alcohol should review all their activities to check whether they need to be approved as wholesalers and, if so, apply on time. Retailers should also prepare for the new scheme and their obligations under it. Failure to comply will lead to severe sanctions as HMRC gets tougher in the fight against alcohol duty fraud

Excise duty fraud, particularly in beer and wine, is a significant problem for the Exchequer and legitimate businesses. Latest figures indicate a median tax gap for alcohol of around £1 billion. Many supply chains have been infiltrated by fraudsters who divert duty-unpaid goods into the UK market. HMRC’s measures to counter the fraud so far have had modest success, including the supposed ‘ideal’ electronic excise movement and control system for EU duty-suspended movements – EMCS.

Of the anti-fraud measures that were considered in 2012, the only one being taken up is the proposal from the Federation of Wholesale Distributors (FWD) to register and control wholesalers of duty-paid alcohol. This is going back to the future to an extent because the Commissioners of HM Customs and Excise were required to license wholesalers in liquor under ALDA 1979 s 65, a requirement repealed by FA 1981. Since then, there has been no official control over the wholesaling of alcohol.

A tough and comprehensive regime

The new provisions to control wholesalers are more pervasive than the old licensing requirement and affect traders who might not even think they are wholesalers of alcohol. HMRC have sewn a fine mesh to prevent fraudsters using gaps in the net for illicit activity and estimate that 21,000 businesses will need to be registered or else will break the law when selling alcohol. Moreover, businesses will not legally be able to buy alcohol for commercial purposes from any non-registered trader. The penalties for breaches will be severe. Trade buyers will be able to refer to approved wholesalers’ unique reference numbers (URNs) via an online lookup facility.

During consultation, the alcohol retail industry had expressed concern that such a scheme would require much resource or it would lack credibility and fail, which HMRC have acknowledged. It is reported that HMRC have recruited 200 staff specifically for this exercise and that training is nearly complete.

Alcohol Wholesaler Registration Scheme

The Alcohol Wholesaler Registration Scheme (AWRS) is for goods traded at or after the duty point, that is duty-paid goods only. It should not be confused with existing control of goods under duty suspension, so-called ‘wet bonded’ goods. Even if a person is approved by HMRC for other excise activities, they will still need to be approved under AWRS if selling duty-paid alcohol wholesale – meaning any quantity of alcohol. The scheme does not apply to private individuals buying alcohol from retailers for their own use.

Legal framework

FA 2015 s 54 amends ALDA and introduces new provisions in s 6A. Meanwhile, secondary law, The Wholesaling of Controlled Liquor Regulations 2015, was laid before parliament in July.

The AWRS sets out a new regulatory system for ‘wholesaling of controlled liquor’ and ‘controlled activities’. In this context, wholesale means any quantity of liquor – that is, not subject to de minimus limits as in the old whole licensing rules.

A ‘controlled activity’ means:

- selling ‘controlled liquor’ wholesale;

- offering or exposing controlled liquor for wholesale sale; or

- arranging in the course of a trade or business for controlled liquor to be sold wholesale.

For the purposes of AWRS, the words ‘offering or exposing for sale’ have this meaning:

- Offering: when a wholesaler makes a specific proposal to enter into an agreement to sell controlled liquor to another trader. For example, the wholesaler approaches a potential buyer and makes an offer to supply controlled liquor under specific terms.

- Exposing: when alcohol is displayed for the purpose of inducing people to enter into a contract to buy it in circumstances in which the sale would be wholesale. It covers ‘invitations to treat’, for example – displaying controlled liquor on premises for the purpose of inviting offers to purchase it.

It would not be necessary for anyone to buy the alcohol for it to be considered as being offered or exposed for sale.

Controlled liquor is sold wholesale if:

- the seller is carrying on a trade or business and the sale is made in the course of that business;

- the sale is to a buyer carrying on a trade or business, for sale or supply in the course of that business; and

- the sale is not an incidental sale, a group sale or an excluded sale.

Incidental sales

AWRS is not designed to capture retailers who trade with the intention of making sales solely to the public. An ‘incidental sale’ – one that is made wholesale but not made knowingly or intentionally by the retailer – is excluded.

Application for approval

Businesses will be required to apply for approval to trade as duty-paid wholesalers and will need to pass a ‘fit and proper’ test imposed by HMRC as a condition of approval. Applications are to be made online using the ‘your tax account service’ accessed through the Government Gateway. It will be an offence to trade without approval.

If approved, the wholesaler will be allocated a URN. From 1 April 2017, they must provide this to their customers and include it on all wholesale alcohol sales invoices.

HMRC will maintain a register of approved wholesalers.

Obligations imposed on trade buyers

This is where the scheme bites deeper. HMRC’s draft public notice states that a ‘trade buyer’ is ‘someone who purchases alcohol from a wholesaler to either sell on to trade, or to sell to private individuals, ie a retailer’. There is no definition of ‘trade buyer’ within the relevant law – I checked this with HMRC at a meeting with policy officials in July.

From 1 April 2017, it will be an offence for trade buyers to buy duty-paid alcohol from unapproved wholesalers. They will need to carry out sufficient due diligence, including evidence of having requested a wholesaler’s URN and checked its authenticity.

If trade buyers are found to have purchased from an unapproved wholesaler, they could face prosecution, be liable to a penalty and their alcohol stock may be seized. If the trade buyer also holds a retail licence, HMRC may also apply to the licensing authority for it to consider sanctions to the trader’s retail licence to sell alcohol.

HMRC’s online lookup system will allow trade buyers to view the details of their alcohol suppliers to ensure they are approved for AWRS.

Contesting a rejection of an application

Any decision by HMRC to not approve an applicant under the AWRS, or to apply conditions to an approval, or revoke an approval, or apply penalties will be subject to a request for review of that decision or appeal to the First-tier Tribunal.