Plan B for the Light Blues

Share this article

Stephen Woodhouse and Charlotte Fleck consider what is next for EBTs as a result of the Rangers decision

Key Points

What is the issue?

The extent to which tax charges may arise as a result of the funding of an EBT either historically for cash-based planning or in the future for wider plans such as share schemes

What does it mean to me?

It will be important to review any historic, cash-based EBTs where no settlement has been reached under the HMRC opportunity. Of greater importance to most people will be to review how the decision may affect wider plans that involve salary sacrifice or funding of trusts

What can I take away?

Tax law is changing and, in the light of case law developments, is uncertain, particularly if any perceived planning or avoidance is involved. This requires continued scrutiny and care, not only when considering the impact of tax avoidance but when there are potentially unforeseen impacts of court decisions in cases involving avoidance

The case involving Rangers Football Club (AG for Scotland v Murray Group Holdings Ltd (and others) [2015] CSIH 77) provides a rare dash of colour to the often turgid world of tax appeals and challenges.

This relates not only to the pseudonyms applied to witnesses before the First-tier Tribunal to preserve their anonymity. The case is also at the centre of extensive attempts by HMRC spanning more than 20 years to counteract tax planning involving employee benefit trusts (EBTs) and represents an unexpected success for it following lower-tier decisions and findings of fact.

Yet the result has brought uncertainty to the law, making further litigation likely.

Structure

The structure was so complex that the First-tier Tribunal decision ran to 186 pages.

The key elements were:

- Murray Group Holdings Ltd, the parent company of the Murray Group of companies, established an EBT;

- the EBT benefited employees of the group, which included footballers playing for Rangers FC;

- contributions were made to the EBT for various employees, some of whom (executives rather than footballers) had no contractual entitlement. Others (mainly footballers) were contractually entitled to payments; and

- the amounts contributed were appointed into sub-funds for named employees and their families. Those assets were used to provide benefits, typically loans, to those employee and their families.

Planning

The planning centred on the intended effect that assets settled on the terms of discretionary trusts were not subject to income tax or NICs.

On that basis, there would be several employment tax consequences (as well as intended inheritance tax benefits). These were:

- no income tax or NICs on the funding of the trust or allocation to sub-funds;

- income tax and NICs on benefits in kind provided during employment by reference to the specific benefit; and

- no income tax or NICs in tax years after the employment ends.

As such, loans would not have been taxed on being advanced; they would have suffered notional interest tax charges under s 175 of the Income Tax (Earnings and Pensions) Act 2003 (ITEPA 2003) in tax years when the individual was employed within the Murray Group, but not in subsequent years. There would have been no charges if the loans were written off after the employee died.

The intended result offered long-term (lifetime) employment tax and NIC planning.

Spotlight 5

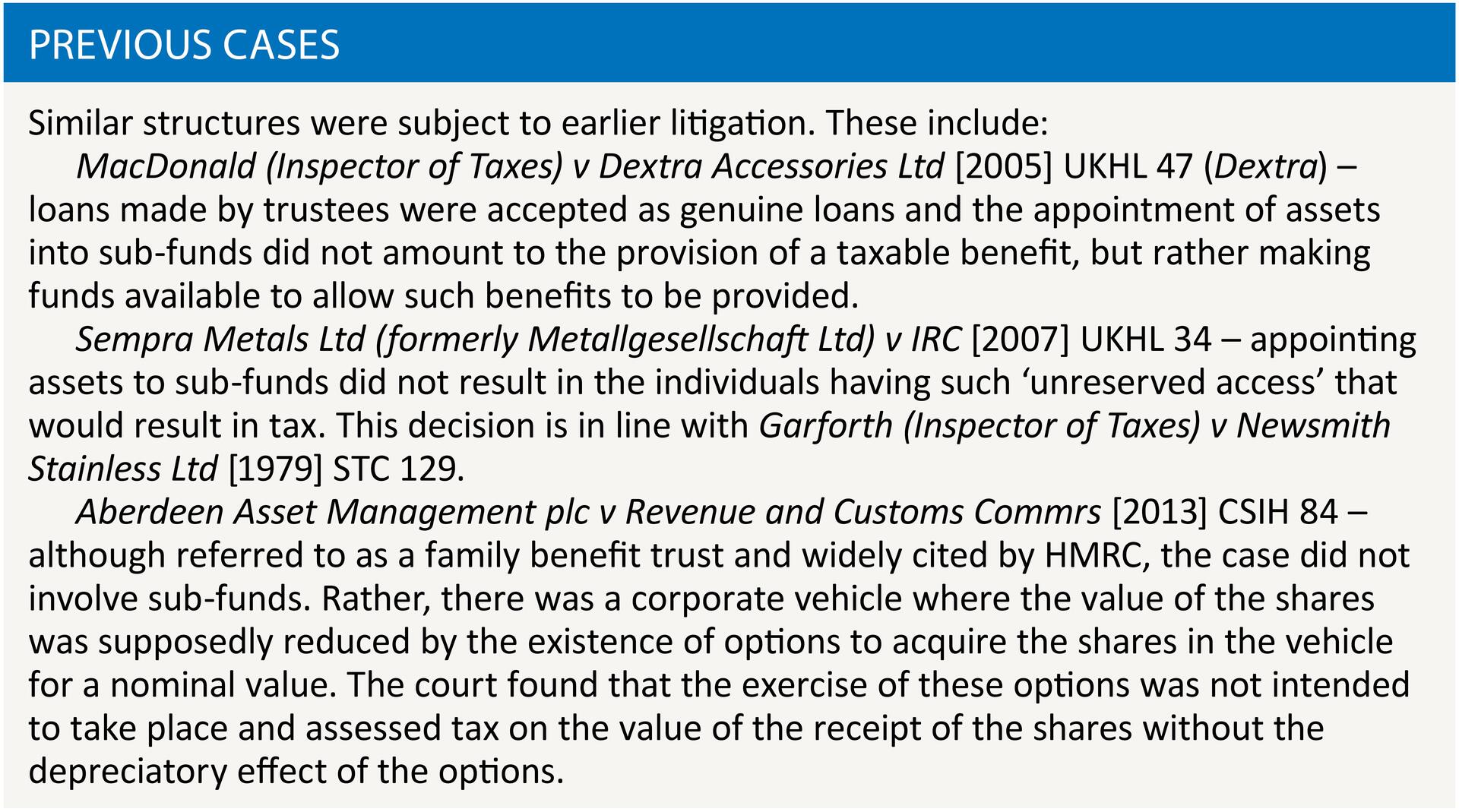

The HMRC view of cash-based EBTs similar in nature to the facts of the Rangers case is set out in Spotlight 5. It states: ‘HMRC’s view is that, at the time the funds are allocated to the employee or his/her beneficiaries, those funds become earnings on which PAYE and National Insurance contributions are due and should be accounted for by the employer’.

The rationale for this view was based on the decision in Garforth. This found that earnings had arisen on the basis that the individual concerned had ‘unreserved access’ to the funds and HMRC considered that this was also the case with EBTs when funds were allocated to beneficiaries.

EBT settlement opportunity

This view led to the offer by HMRC to settle PAYE and NIC liabilities under the EBT settlement opportunity (EBTSO) based on the taxpayer accepting the view of the law set out in Spotlight 5. This offer expired on 31 July 2015.

Rangers case

Facts

The essence of the findings related to the structure discussed above. The underlying facts were favourable to HMRC, with evidence suggesting de facto control of trust assets by beneficiaries. Many advisers expected HMRC to win the case at First Instance but, based on the findings of fact advanced, the tribunals decided in favour of the taxpayer, severely denting the basis for the Spotlight 5 claims for taxability on allocation of assets.

Court of Session decision

In the Court of Session, a different approach was advanced by HMRC and endorsed by the court. This applied the ‘redirection principle’. The court considered cases such as Hadlee v IRC [1993] AC 524, Brumby (Inspector of Taxes) v Milner [1976] 1 WLR 29 and Smyth (Surveyor of Taxes) v Stretton (1904) 5 TC 36. These show that, if an employee directs remuneration to be paid to a third party (for example, to discharge a debt), it amounts to earnings of the individual taxable when received by the third party in the same way as if received by the individual themself.

This analysis was applied not only to the contractual amounts payable to the footballers, but also the non-contractual amounts payable to the executives in the wider Murray Group.

In reasoning bearing some resemblance to the logic applied in R & C Commrs v PA Holdings Ltd [2011] EWCA Civ 1414, the court adopted an approach based on analysing the commercial reality of the payments. It concluded that the payments into the trust were from the employment of the individuals concerned and should be viewed as taxable earnings, subject to PAYE and NICs, at the point when received by the trustees.

Impact of decision

This decision, if reached by the First-tier Tribunal, would not have been surprising in relation to the contractual amounts. One point of difference between this case and other similar structures was the payment of contractually committed amounts to the EBT.

Extending this to circumstances in which it was found as a fact that there was no earlier contractual right, so that the payments, by implication, were made to the trustees by the company on a discretionary basis, is a departure from previous case law and practice. This, linked with the court reaching this conclusion after arguments that had not been advanced at the earlier hearings, presents potentially unintended consequences in areas of established practice and benign planning.

Existing EBTs

The decision should not affect existing EBTs if settlement has been reached under EBTSO. In other cases, however, HMRC has scope to apply the decision to argue for tax to arise at the point of funding of the trust rather than allocation of assets. In many cases, this would lead to the same result (where the allocation occurs shortly after funding), but would be inconsistent with the basis of the settlement offer and the HMRC approach both in Spotlight 5 and tax cases (starting with Dextra) spanning more than ten years.

Receipts basis

The court struggled to reconcile its decision with the receipts basis of tax applied to earnings by s 18 of the Income Tax (Earnings and Pensions) Act 2003 and interpreted in cases including the Court of Appeal in R & C Commrs v UBS AG [2014] EWCA Civ 452. That was distinguished only by reference to a questionable distinction between cash and share (or other asset) based awards, leading to the potential for different tax results for each.

Income tax/NIC congruence

The court had a similar difficulty in Forde and McHugh Ltd v R & C Commrs [2014] UKSC 14. This concerned the NIC treatment of contributions to another form of employee trust, an unapproved pension scheme. In this case, the Supreme Court held that NICs were payable only on what the employee received.

The reconciliation adopted by the court was to seek to limit the decision in Forde and McHugh to NIC liabilities, leading to the prospect of tax arising at a different time and on a different amount from NICs. Although the definition of ‘earnings’ for NICs (s 3 of the Social Security Contributions and Benefits Act 1992) is not identical to ‘remuneration’ as defined for ITEPA 2003 purposes (s 62, ITEPA 2003), it is difficult to discern any relevant distinction in the language or case law interpretations of the two terms.

Deferred compensation

The redirection principle as applied in the Rangers case creates the scope for tax to arise under deferred compensation schemes. This applies if awards have been made subject to performance conditions and are therefore subject to contingency but specific payments have been made to a third-party trustee to fund the eventual payments should vesting occur.

Although the court did not seek to overturn the long established principles underlying deferred compensation plans in Edwards v Roberts (1934) 19 TC 618 and specifically confirmed its continued applicability, it is difficult to reconcile the court’s analysis with that case.

Salary sacrifice

Salary or bonus sacrifice arrangements, particularly into registered pension schemes, are well established. HMRC gives detailed consideration in its guidance manual EIM42750. This treatment is predicated on ensuring that payments are not for contractual amounts, but merely allow for expressions of wishes by the employee, without which the salary sacrifice would not be effective. Instead, the funding would be regarded as employee contributions giving rise to additional NIC costs. HMRC has been asked to clarify the impact of the Rangers decision on salary sacrifice arrangements, but stated that it did not intend to make any substantive statement until any appeal proceedings have been resolved.

Disguised remuneration

The disguised remuneration (DR) legislation is designed to apply tax and NIC charges on an earmarking event, imposing tax on the allocation of assets consistently with the position set out in Spotlight 5. The extensive exclusions provide protection for various plans by reference to this charging structure.

If the reasoning in the Rangers case is applied widely, it could lead to charges arising on the funding of the trust or other third-party arrangement without the need for an earmarking. This would undermine not only the operation of the DR rules, but also the exclusions to protect share option plans and other forms of ‘safe’ plan design.

Reliability of findings of fact

Although not directly germane to the tax implications of the case, the willingness of the Court of Session to admit arguments that altered the decision and that were not raised in the First-tier or Upper Tribunal is concerning. The redirection principle had not been considered by either tribunal; had not been advanced previously by HMRC; and did not feature in the rationale for Spotlight 5 or the many cases settled under EBTSO.

What happens now?

It appears that an appeal against the decision will be heard at the Supreme Court. If this happens, there will be continued uncertainty on the correct way of taxing EBTs with individual fund allocations before the application of the DR legislation. Following that legislation, such allocations and ‘earmarking’ would give rise to clear charges to tax collected through PAYE and NICs.

The uncertainty remains, however, for historic EBTs that have not settled under the settlement opportunity and in the other areas of difficulty highlighted in this article. For most taxpayers, it is the latter that will cause most concern, with clear scope for innocent planning to be adversely affected and with uncertainty and risk resulting, accompanied by a need for careful planning of the plans potentially affected.